3 immediate implications of tighter lending standards

In our latest 50-page report for funds and institutional investors, Chemical Change, we’ve conducted a detailed consideration of shifts in mortgage lending standards, and the likely outcomes from these changes. Highlighted below are three immediate implications.

1) Crimped borrowing capacity for portfolio investors

The regulator might justifiably be bemused by commentary of the ‘recent’ tightening of lending standard given that tightening commenced in earnest in 2014 and has been in evidence incrementally ever since. Perhaps media coverage heightened due to the Royal Commission and reports of declining dwelling prices, following several years of gains.

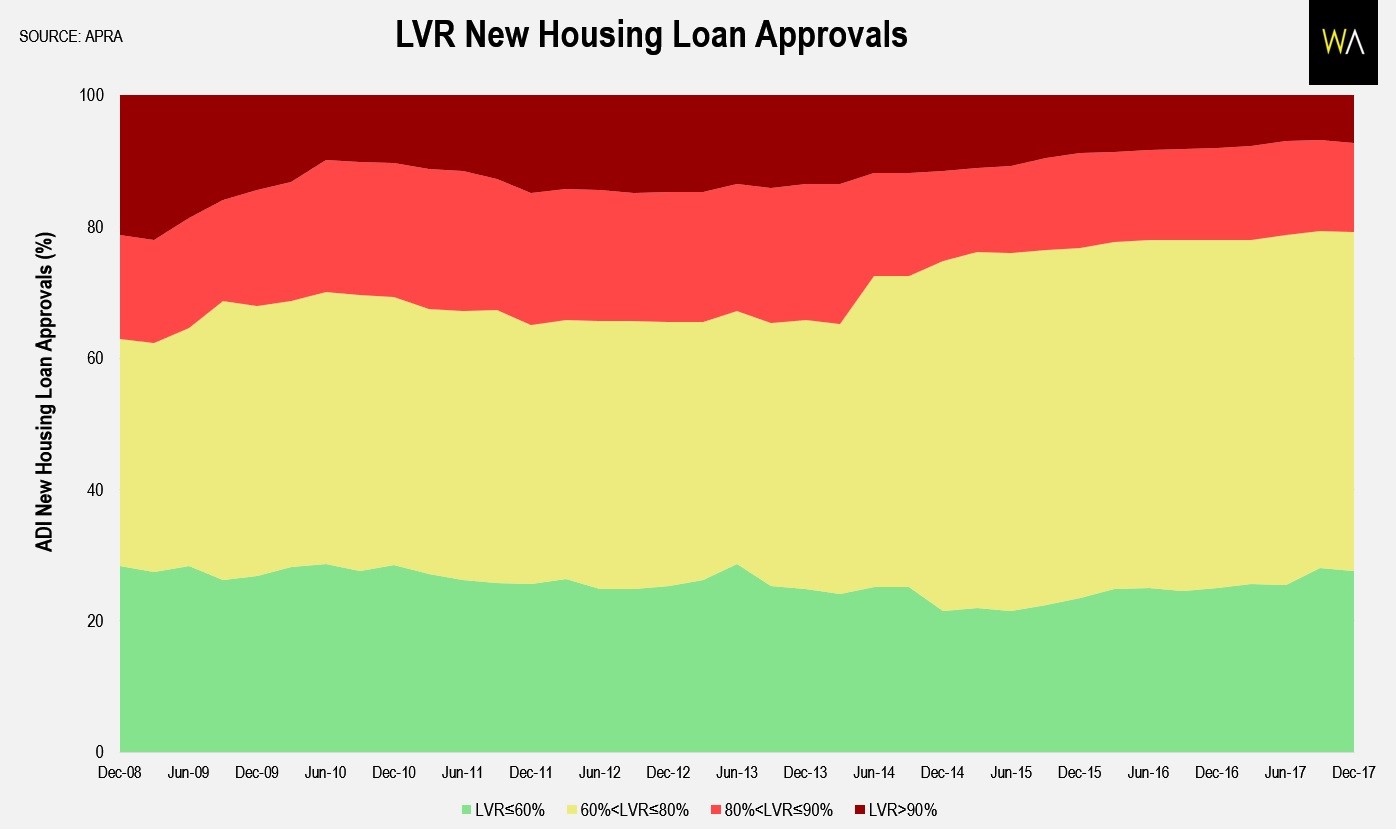

Highly leveraged loans have gradually been dialled back

A breakdown of loan-to-value ratios (LVRs) reported by APRA relating to ADIs denotes how highly leveraged loans have gradually been dialled back, while mortgages have been assessed at conservative rates of 7 per cent for several years, reducing the risk in the market.

While borrowing capacity has only been trimmed marginally for most homebuyers, there’s been a considerable impact on many portfolio investors. This is pruning lending volumes at the margin and has helped to remove much of the speculative heat from the housing markets of the two main capital cities.

There will be greater scrutiny of actual household expenses by category to contend with, while mortgage processing times for ADI lenders could potentially be drawn out as brokers get to grips with an increased administrative burden.

2) Reducing stock of interest-only loans

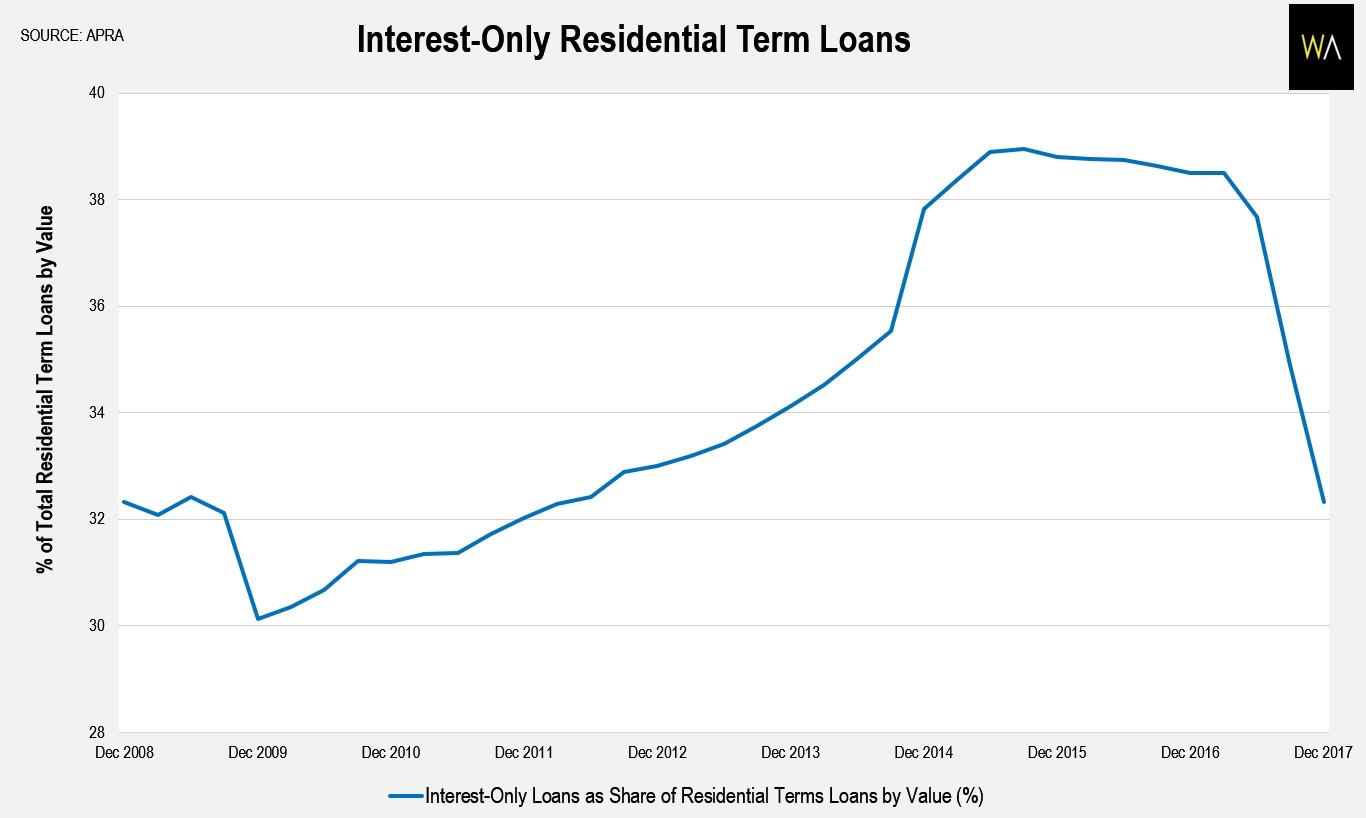

We highlighted last year in our P&I Cliff report for funds and institutions the possibility of a problematic reset eventuating from tighter lending standards (albeit this was not the base case).

Regulatory moves have been swift and effective in reducing the flow of new interest only (‘IO’) mortgages, with market share cut dramatically from more than 45 per cent of housing loans to households at the Q2 2015 peak to about a third of that level by the end of 2017.

Furthermore, the introduction of an interest rate differential between investor and owner-occupier loans incentivised borrowers to switch voluntarily to paying back principal sooner than scheduled.

It’s worth remembering that although short-term funding costs have increased recently, some lenders have profited from the higher mortgage rates on IO loans, so there may be scope for margins to compress.

The stock of IO loans has quickly declined from nearly 40 per cent to closer to 30 per cent of total outstanding mortgage credit, with IO loans outstanding dropping by about $75 billion over the past year.

The repayment of principal is thus taking place sooner than expected in many cases. While some adverse impacts may be evident on consumer discretionary expenditure, the risks of a ‘trigger’ event appear to remain well contained.

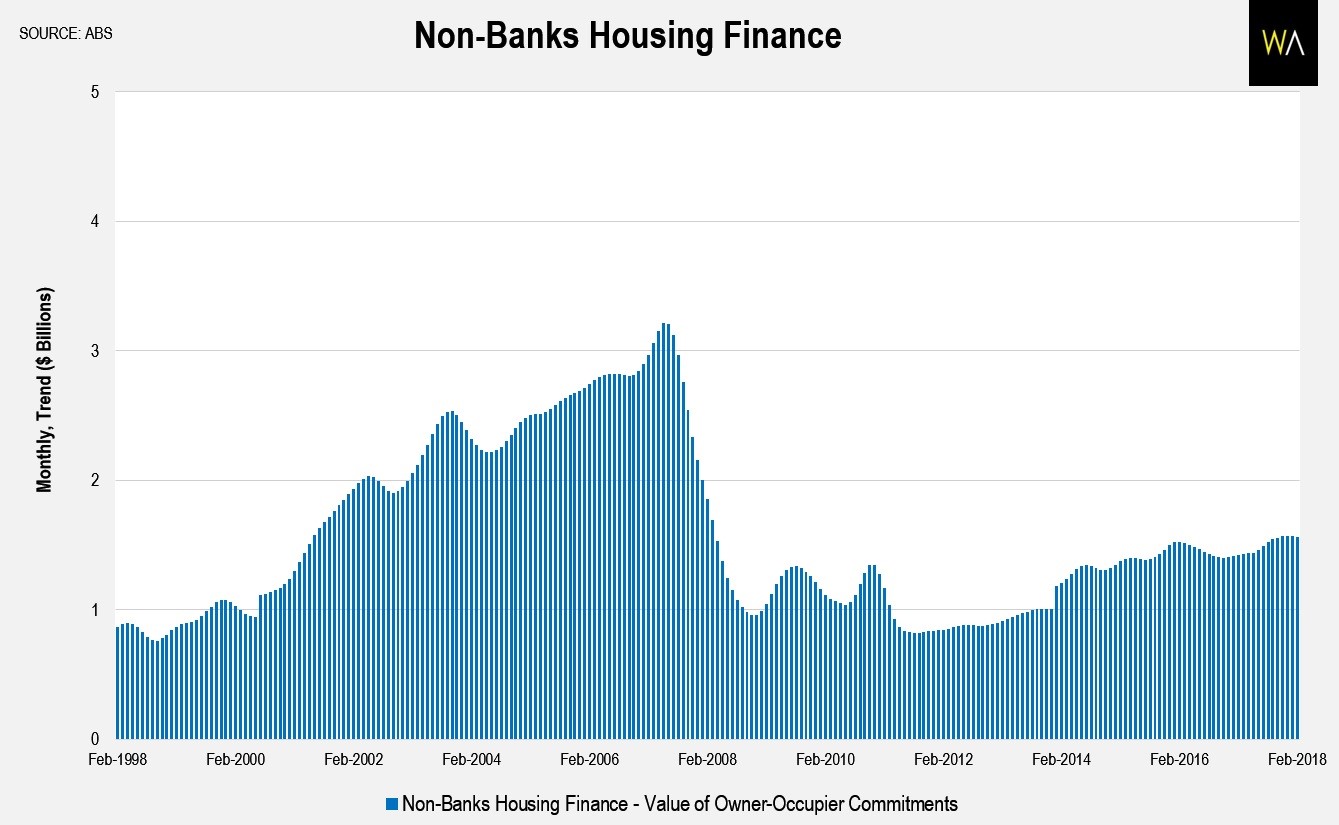

3) Non-banks step into the breach

With a historically high volume of apartment projects still under construction, settlement default risks have increased somewhat from low levels, with some developers recording a moderate increase in instances of non-settlement.

Some commentary has alluded to a recent shift towards subprime lending, but that is unsupported by facts or our experience on the ground, with lending standards having incrementally moved in the other direction.

The default risks are arguably most elevated in inner-city Brisbane where newly completed units are frequently failing to value up at settlement, while the resale market for new apartments is thinner.

Sydney has by far the greatest number of dwelling units still under construction, but in absolute terms population growth in both Sydney and Melbourne has remained at or close to all-time highs, and the underlying demand for housing remains strong.

Our liaison with mortgage brokers highlighted a recent jump in activity at a couple of the non-bank lenders, which is helping to absorb some of the risks related to any lack of access to credit.

Although non-bank lenders have traditionally been associated with a higher systemic risk, in most cases lending standards are considerably higher than in cycles past, as well explained by Christopher Joye in the Australian Financial Review last week. Hopefully Joye’s crisp article will draw the attention it deserves, having taken a machete to reams of misinformed analysis on Australian lending practices.

Although non-banks are not governed by the same regulatory measures as the mainstream lenders, ASIC’s granting of a licence to continue operating remains conditional upon satisfactory processes. Meanwhile low-doc loans, a staple of the lending market through previous cycles, now comprise only a small share of new mortgage flows.

Secondary implications

Tighter macroprudential measures were required because a small cohort of borrowers had become efficient at extracting equity and growing investment property portfolios at a rapid pace.

The Australian housing market at the national level has cooled, though the recently reported declines in prices need to be viewed in the context of half a decade of price gains in the two most populous cities.

Private dwelling investment reversed from record highs into a steady decline through 2017 and may slow from a peak of ~$25 billion per quarter towards ~$20 billion. However, the risks from a sharp slowdown have been offset by a timely boost to the non-residential sector, with the value of commercial approvals surging to an all-time high $46 billion over the year to Q1 2018.

Our ongoing liaison with mortgage brokers has corroborated some previously discussed weaknesses in lending practices.

Our ongoing liaison with mortgage brokers has corroborated some previously discussed weaknesses in lending practices. For example, the additional liabilities of some borrowers were not always being captured in a complete and accurate manner, a loophole that has now been tightened up.

Robust internal controls relating to the writing of mortgages to Chinese borrowers several years ago were also found to be wanting at some institutions. Yet brokers report that these loans have significantly outperformed in terms of arrears rates, perhaps due to a cultural disposition towards honouring debts.

Some commentary has alluded to a recent shift towards subprime lending, but that is unsupported by facts or our experience on the ground, with lending standards having incrementally moved in the other direction. We’re seeing a tightening in standards, but credit is still flowing, and transactions are still settling, in lower volumes.

Certain risks remain at large, including whether a prospective change in government will ultimately result in a landscape change for the way in which investment property is taxed, particularly with regards to net rental losses and capital gains, bringing how well this week’s healthier Federal Budget is received into sharp focus.

The full 50-page "Chemical Change" report for funds and institutional investors includes our detailed assessment of the impact on banks and lending flows, housing market risks, and implications by sector.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Co-founder of AllenWargent Property Buyers - "the better way to buy property".

Veteran property market analyst & investor.

3 topics

4 stocks mentioned

Co-founder of AllenWargent Property Buyers - "the better way to buy property". Veteran property market analyst & investor.

Co-founder of AllenWargent Property Buyers - "the better way to buy property". Veteran property market analyst & investor.

Comments

Comments

Sign In or Join Free to comment