Bathwater babies and value opportunities

“Buying cheap stocks is great, but buying good companies cheaply is even better” - Joel Greenblatt

Value investing has so much intuitive appeal. Who doesn’t like a bargain? However, in recent years much has been written about the death of value investing. Value investing is sometimes mistaken for a style that just buys cheap stocks. However, this superficial method says nothing about business quality. The problem with just buying cheap stocks is that they can remain cheap for good reasons.

Valuations and quality attributes of a company are joined at the hip and is best expressed in the following equation:

Price to book multiple = (return on equity - growth rate) / (discount rate - growth rate)

In the equation, price to book (PB) multiple is a proxy for valuation and return on equity (ROE) is a proxy for quality. Hence, if a company’s quality is lower it means a company’s valuation should also be lower and vice versa (if all else is equal). It’s not surprising that the collective wisdom of the market roughly captures this relationship. This market efficiency is highlighted by the correlation between ROE and PB multiple for the Australian banking sector through time and across stocks.

Time-series of Commonwealth Bank’s PB multiple and ROE

Source: FactSet

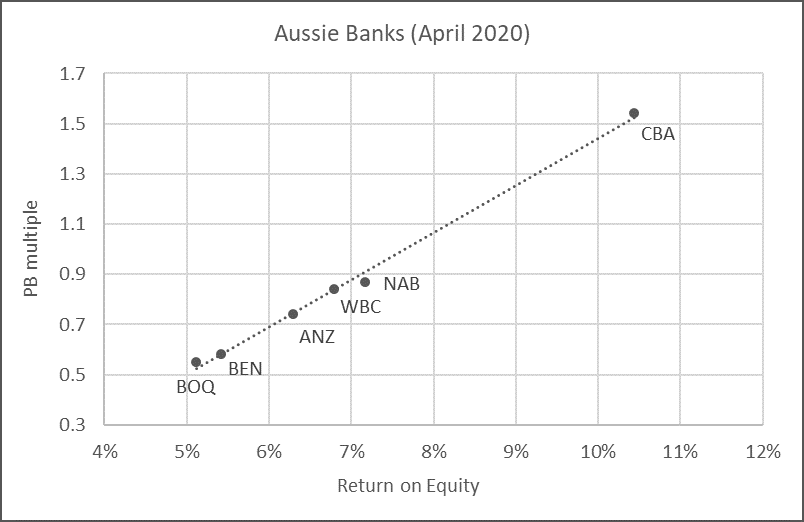

Cross-section of Aussie bank’s PB multiple and ROE

Source: FactSet

If the cheapest bank has the lowest ROE and the most expensive bank has the highest ROE, do you think they are mispriced (undervalued or overvalued)? Or is the market simply efficient in pricing the quality of the business?

‘True’ value investing is not about buying cheap stocks for cheap sake but is about identifying mispriced securities when valuation and quality are disconnected. In other words, buy good companies at a cheap price. For example, a defining moment in Warren Buffett’s career was when he bought American Express (a ‘compounding machine’ as he would later call it) after its share price collapsed from the Salad Oil Scandal in the early 1960s.

Joseph Piotroski (2000) later popularised the idea of buying good quality companies when valuations are cheap. His research paper attempted to sort out company valuations disconnected from their fundamentals. His findings highlight that higher quality companies within the value basket delivered 7.5% p.a. higher returns than the entire value basket alone. Piotroski’s research helped lay the foundation for the quantitative world in creating factor exposures for the quality attributes of companies.

Finding valuations that are disconnected from fundamentals is rare because markets are roughly efficient over time. But it becomes easier during market corrections because indiscriminate selling creates more opportunities. At Vertium, we call these opportunities “bathwater babies”, where the market has thrown out the baby with the bathwater. Post the COVID crash, our research highlights two stocks (Lendlease and Cochlear) where their current valuations are substantially dislocated from their business quality.

Lendlease (LLC)

LLC’s core business is property development, hence it’s no surprise that its valuation multiple falls when economic growth slows. During these periods, it makes no sense to value a business on earnings multiple because short-term profits evaporate.

Fortunately, there are multiple ways to adjust valuation multiples when earnings are temporarily depressed. One could use the earnings generated before the slowdown. For example, the historic 10-year average earnings could be used similar to the method adopted by the Shiller CAPE ratio. Alternatively, we like to use the PB multiple. If the long-term ROE of the business has not changed and the PB multiple is temporarily depressed, then a disconnect between valuation and quality is potentially identified.

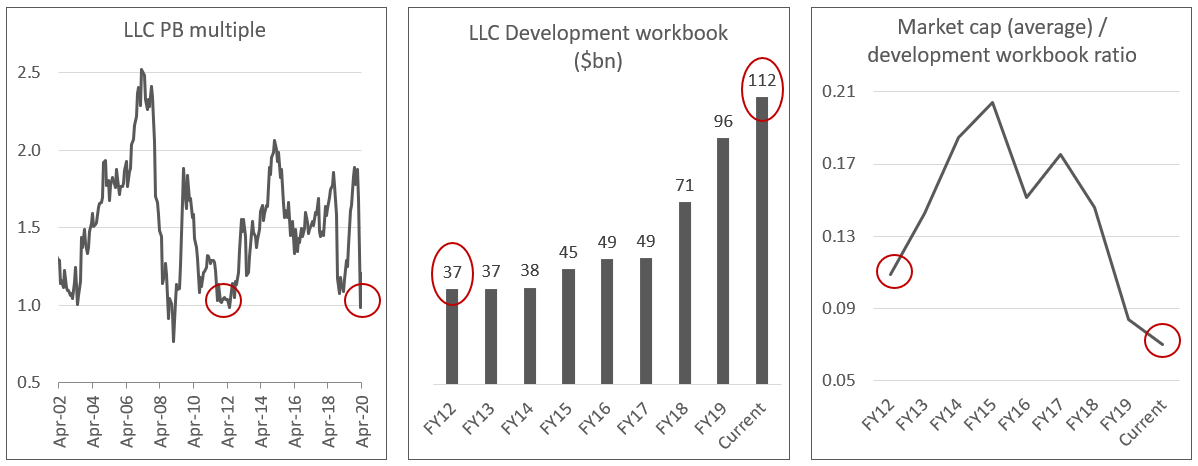

LLC can currently be bought close to its book value. At current prices LLC represents a classic value stock where the market is not willing to pay for much goodwill or future growth of the business. However, LLC offers more than just being cheap, there is a large disconnect between its current valuation and its fundamentals. LLC’s PB multiple is temporarily depressed but the business is likely to be stronger in the future given its large development workbook (a proxy for its future earnings and ROE).

The disconnect between valuation and quality is even more apparent when examining the ratio of LLC’s market cap to its development workbook over time. This ratio is currently the lowest in history highlighting that LLC is cheaper now (compared to future profits) than during the Euro crisis in 2012.

Source: FactSet, Lendlease, Vertium

Cochlear (COH)

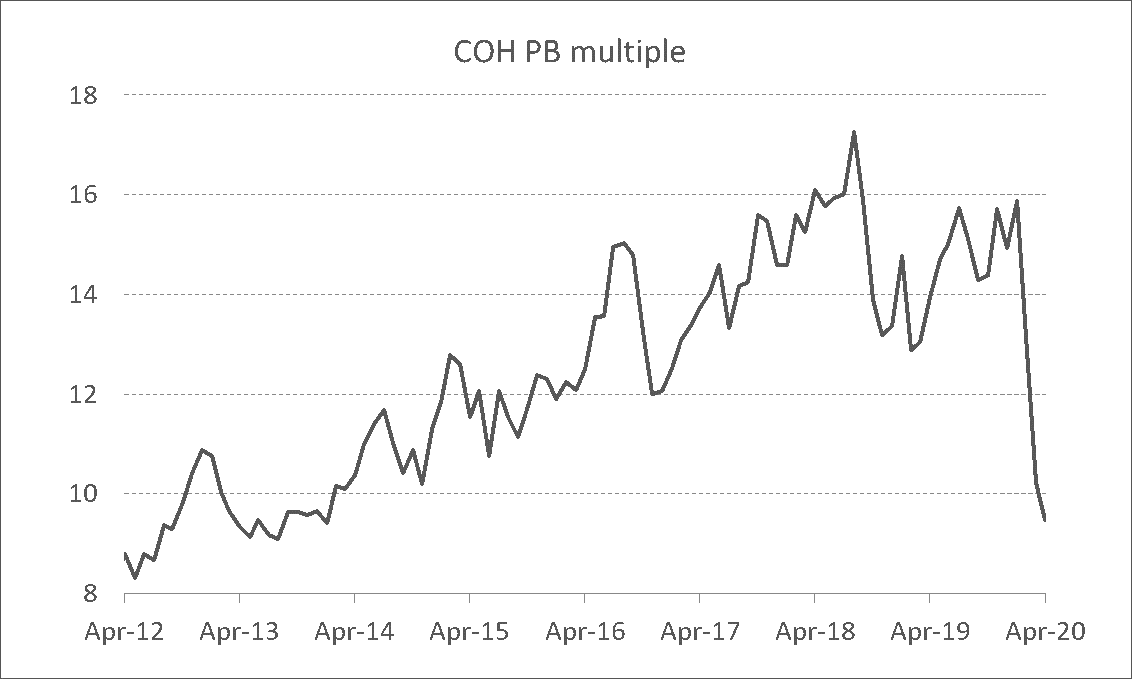

COH would not be the first stock you think about when investing for value. Its leading global position allows the company to earn an extraordinarily high ROE (5-year average of 44%). Most investors would call it a compounding machine given its long track record of delivering earnings growth. Given its pedigree the stock has seldom exhibited a cheap headline valuation multiple. Many believe that traditional price to book multiple is obsolete for growth companies such as COH because intellectual property does not show up on a balance sheet in the same way as tangible assets.

However, when earnings are temporarily depressed the old chestnut, PB multiple, becomes extremely useful. Given the COVID crisis, the lack of elective surgeries has resulted in a very large earnings hole for COH. Its share price has de-rated to such an extent that its current PB multiple is as cheap as it was in 2012, the year that its business was affected by a product recall.

Source: FactSet

COH’s business bounced back from that temporary setback in 2012, but the key question now is whether it can recover from the COVID crisis. In other words, will its depressed valuation reconnect with its long-term profit generation capability? If its long-term ROE is not impaired, then earnings should mean revert. Hence, over time COH’s PE multiple should compress and its PB multiple should expand with an improving ROE.

Our research indicates that COH should recover well post the COVID crisis. There is evidence that Cochlear surgeries have mean reverted to pre-COVID levels where lockdowns were lifted, such as in China. If the reason for the earnings collapse is due to no elective surgeries, then by the same logic earnings should recover when elective surgeries resume. Furthermore, in the near term there’s scope for COH’s earnings to recover strongly given that Advance Bionics (a key competitor) issued a product recall just before the COVID pandemic lockdowns. In the long term, COH’s runway of growth will be enhanced if management can successfully commercialise a totally implantable cochlear implant from their R&D program.

Summary

Rather than systematically buying value (regardless of quality), ‘true’ value investing involves looking for disconnects between valuations and quality. While value investors will naturally have a tough time in a bull market, there are many market dislocations on offer due to the COVID crisis. Both Lendlease and Cochlear have been thrown out with the bathwater and over time their current depressed valuations will eventually reconnect with their strong business fundamentals.

In our view, Greenblatt’s quote at the start of this article is only partially correct. We suggest that this quote should be changed to:

“Buying cheap stocks is SOMETIMES great, but buying good companies cheaply is ALWAYS great.

Reference:

Piotroski, J., Value Investing: The Use of Historical Financial Statement Information to Separate Winners from Losers, Journal of Accounting Research, 2000, Volume 38, pp. 1-41

Get investment ideas from industry insiders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

2 topics

8 stocks mentioned

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Comments

Comments

Sign In or Join Free to comment