Equity train could stay on the rails for now

Marcus Tuck

Mason Stevens

The market is expecting US growth to rebound from its temporary hiatus in the March quarter, and for China's growth to slow only modestly this year. If both of those things happen the equity train can stay on the rails for a while longer, with growth being neither too hot nor too cold.

Financial markets prefer to see economic growth and inflation in the "Goldilocks" zone - not too hot and not too cold. Extremes at either end, either high inflation or deflation, are destructive for equity markets. Equity investors want economic growth to be strong enough to sustain profit growth but not so strong that it provokes central banks into raising interest rate aggressively to prevent a breakout of inflation.

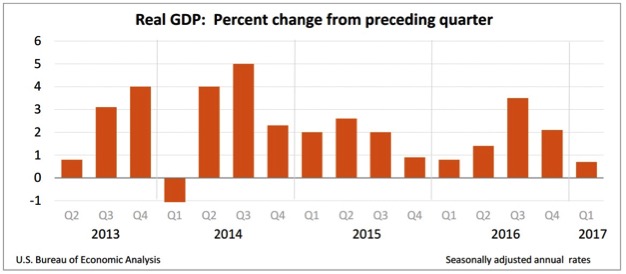

The latest GDP result for the US, released on Friday, showed a weaker-than-expected slowing in the March quarter. In fact, it was the slowest growth in 3 years. US GDP increased at an annualized rate of just 0.7%, down from growth of 2.1% and 3.5% in the preceding two quarters (see chart below). The consensus forecast was for 1.0% growth in the March quarter.

If growth stays that weak it would be concerning but the slowdown appears tied to temporary effects that are likely to reverse in coming months. The steep drop-off stemmed from the smallest increase in consumer spending since the end of 2009. Consumer spending rose just 0.3%, a steep drop from the 3.5% growth recorded in the December quarter last year.

The pullback in consumer spending seems unlikely to last. Americans spent less on gasoline and home-heating fuel after a spell of unseasonably warm weather in February-the second-hottest on record. Warm weather also hurt sales at retailers such as clothing stores trying to move the last of their cool-weather inventory, and a bout of stormy weather kept consumers away in March. There were also fewer sales at car dealers.

Household finances are in fact in the best shape in years due to employment growth, gradually rising wages and strong stock market gains. An index that tracks labour costs posted the biggest gain in a decade. The US Employment Cost Index rose 0.8% in the March quarter, an indication of tighter labour market conditions.

Millions of Americans also received their tax refunds later than usual in 2017, a delay that probably shifted some spending from the first quarter into the second quarter. The better financial positions of households is evident in steadily rising home sales. In the first quarter, investment in home building climbed 13.7%, making the construction industry a significant engine of US growth. All of these things make it likely that US consumer spending will rebound in the second quarter.

Another sudden tailwind for the economy, after a prolonged absence, is business spending. Companies are investing more in structures such as drilling rigs and office buildings. Fixed business investment increased 10.4% and accounted for the bulk of US growth in the first quarter, a marked contrast to the prior two years when it was often going backwards. The gain was driven by a 450% increase in investment by energy producers intent on pumping out more oil and natural gas. If Congress succeeds in eventually passing business and personal tax cuts it should boost business investment and consumption further out.

Companies barely increased the production of goods in the March quarter though, making inventories the other big drag on growth in the quarter. Inventories rose by just US$10.3 billion in the first quarter, after a roughly US$50 billion increase at the end of 2016. As a result, inventories subtracted 0.93 percentage points from GDP growth. However, final sales of domestic product rose 1.6% compared to 1.1% in the December quarter, providing some comfort that underlying economic momentum is not deteriorating.

Government spending at the local, state and federal levels fell 1.7% in the March quarter, the largest drop in 4 years. Defense spending contracted by 4.0%, which is likely to be reversed. Net exports had only a small positive impact on growth in the quarter, with exports up 5.8% and imports up 4.1%.

Meanwhile, inflation advanced at a 2.4% annual pace in the first quarter, based on the Personal Consumption Expenditure (PCE) deflator, the Federal Reserve's preferred inflation gauge. It easily topped the central bank's 2% target for the first time in several years. However, the Core PCE deflator that strips out the volatile food and energy categories was little changed at 2%, underscoring the big effect that oil prices have on US inflation. Oil prices have retreated after the run-up late last year, suggesting moderation in price pressures. But if labour costs continue to rise that could become another source of worry for the Fed.

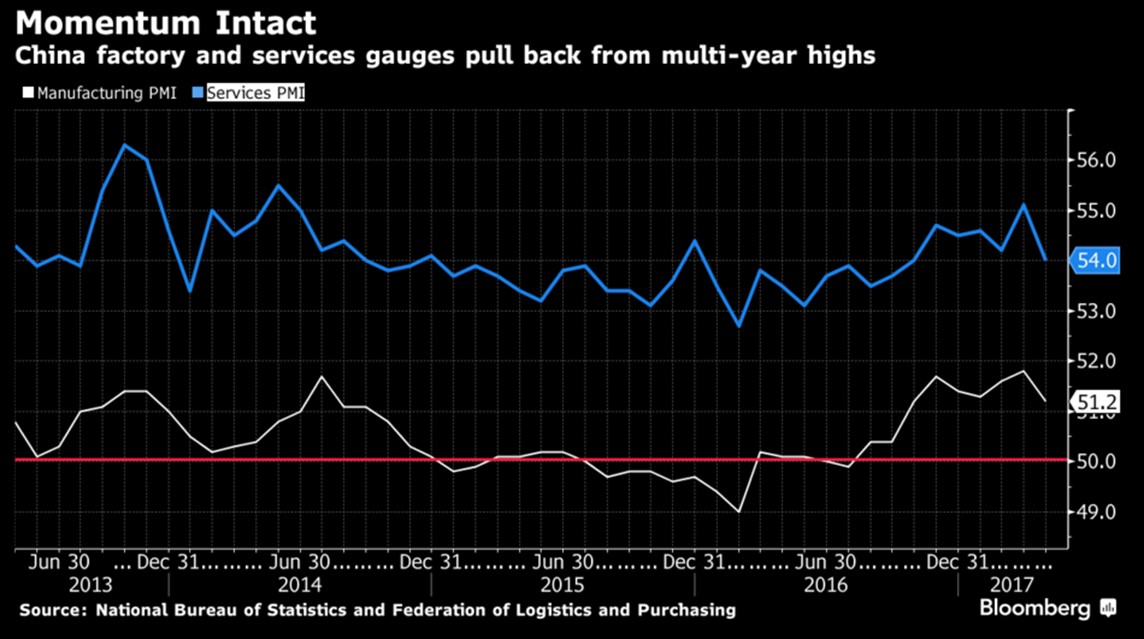

The latest economic data for the world's second-biggest economy, China, were also on the softer side. China's official factory gauge declined as commodity prices fell. The Manufacturing Purchasing Managers Index (PMI) fell to 51.2 in April from an almost 5-year high of 51.8 in March, and was below the consensus forecast of 51.7. The Services PMI decreased to a 6-month low of 54.0 from 55.1. Both gauges still point to growth though, as readings over 50 indicate expansion (see chart below).

China's GDP growth is likely to slow after unexpectedly picking up to 6.9% in the first quarter, the first back-to-back acceleration in two years. Factory and services activity remain at relatively robust levels, but the April data showed weakening across employment, output, new orders and export orders. In general, China is undergoing modest monetary tightening and strengthening of regulations. China's full-year GDP growth is expected to slow to 6.6% from 6.7% last year, according to the latest Bloomberg survey.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

4 topics

Marcus Tuck

Head of Equities

Mason Stevens

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

Expertise

Marcus Tuck

Head of Equities

Mason Stevens

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

Expertise

Comments

Comments

Sign In or Join Free to comment