Extreme market reactions ahead

Vimal Gor

Pendal Group

This time last year, at Livewire Live we flagged a likely resurgence of volatility and highlighted some of the factors that we believed would drive this. In this exclusive report for Livewire, I review the thesis and explain why we expect much more extreme reactions going forward.

The most significant force was the global withdrawal of unprecedented central bank stimulus and the draining of liquidity from the financial system. One year on, we have witnessed:

- One of the largest spikes in volatility since the GFC,

- A 10% peak-to-trough sell-off for the S&P 500,

- Routs in high yield credit and,

- A dramatic downturn within emerging markets.

As central bankers continue to march down the path of policy normalisation, alongside the heightened spectre of political disruption, we believe volatility is likely to persist in the near term.

Despite some of the sizeable market swings experienced in 2018 thus far, policymakers have shown little sign of shying away from monetary tightening. The Federal Reserve has already delivered two rate hikes this year and is widely expected to deliver at least one more before year end, while a further three are priced in for 2019.

Its peers are following suit with the Bank of England and Bank of Canada having ratcheted up rates further this year and the ECB forecast to do the same in 2019.

"The Federal Reserve has already delivered two rate hikes this year and is widely expected to deliver at least one more before year end , while a further three are priced in for 2019"

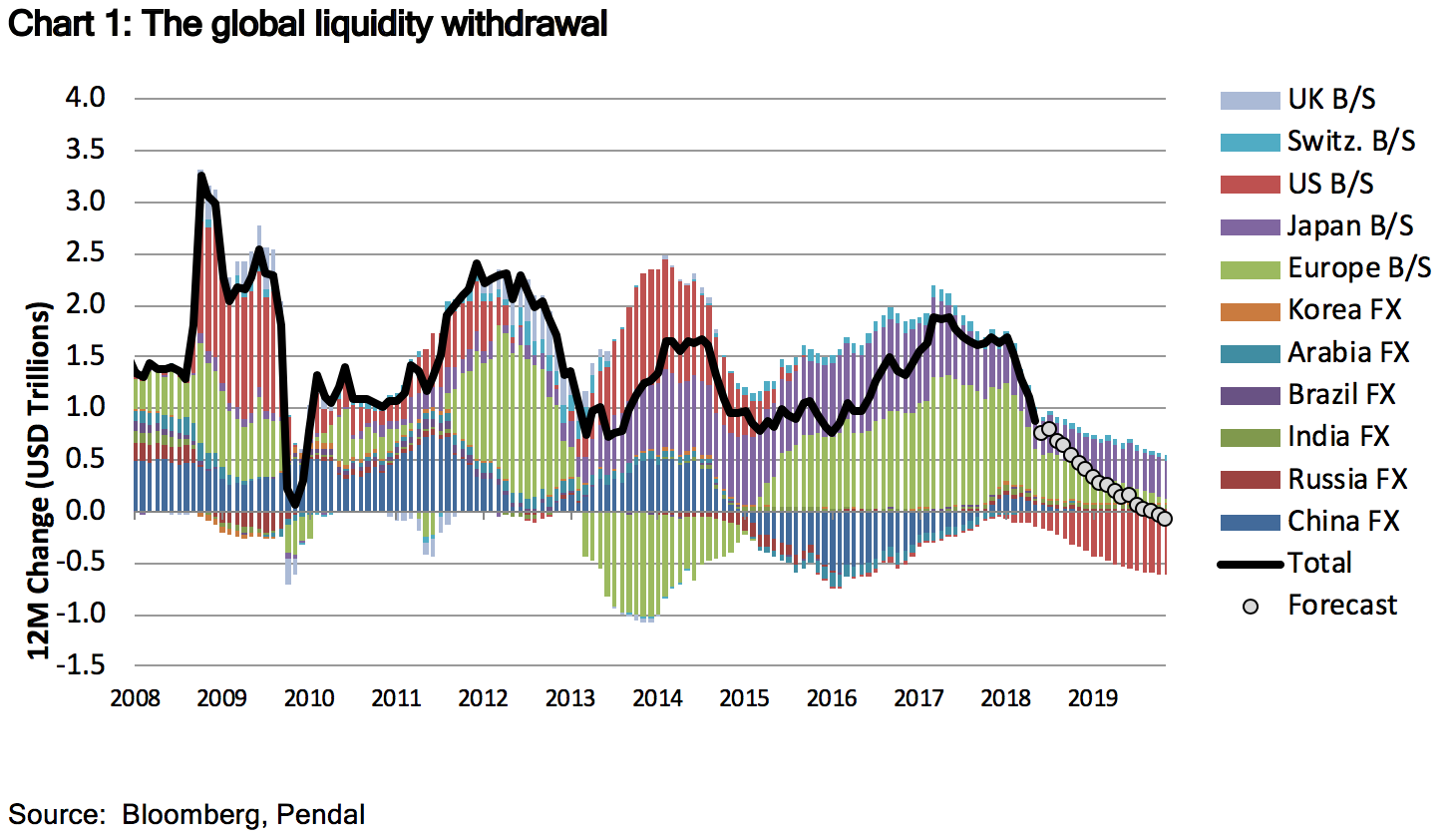

Compounding this global policy tightening is the reduction of central bank balance sheets. The Fed continues to sell down large blocks of its securities each month, while the ECB will halt its purchases of corporate and government bonds this quarter. Together, the annual change in global central bank balance sheets is now forecast to shrink next year, as illustrated in the chart below.

The winners and losers

When we started to identify the risks posed by this thematic, we flagged several areas that we believed would be most vulnerable, namely those that had benefited most from the swell of liquidity in prior years and those that had lured investors with the potential for higher returns in an era of low yields.

This included high yield credit, pockets of emerging markets, as well as regions particularly susceptible to political disruption.

On the reverse side, we believed as investors unwound their higher risk positions, safe-havens like the US Dollar would benefit.

Of course, timing such a reversal in risk sentiment and change in market regime from a long period of calm seas to one of crashing waves can prove difficult. For example, the slide of the US Dollar into the end of 2017 was surprising for us and many other market participants, as was the continued strong performance of high yield credit. The latter required us to adopt some innovative positioning. Rather than taking a single position that would benefit when credit sold-off, we adopted relative value trades that could still perform well in a market sell-off, but at a lower cost.

When we saw the S&P’s 10% correction and 308% VIX spike in February this year, we knew the volatility regime change we had been expecting was underway.

Several subsequent episodes of volatility helped reinforce this view and benefited our positioning. One such episode was the well-publicised Italian political turmoil. This reflected a theme we had identified around heightened political risk, particularly in Italy ahead of its general election. We positioned our portfolios accordingly and they subsequently benefited significantly from the large spike in the country’s yields.

Where to from here?

Looking forward, we believe Italy’s experience reflects a growing trend across broader Europe away from the prevailing centrist political views, to the extremes. This is likely to feed further fiscal policy uncertainty in the near term and trigger additional bouts of market volatility. The ECB removing stimulus is also effectively pulling the rug out from overvalued asset prices in the region, leaving European credit particularly exposed.

"The ECB removing stimulus is also effectively pulling the rug out from overvalued asset prices in the region, leaving European credit particularly exposed"

Emerging markets (EM) have been another area of significant volatility and political disruption, with specific pockets more at-risk than others. During the years of low yields, many market participants were tempted into developing economies in their search for higher returns. Now as global stimulus is being withdrawn these positions are being unwound, causing rapid capital outflows and dramatic downturns in their currency and bond markets. Turkey has been a prime case study this year with the Turkish Lira having plunged 42% to the end of August. It is just one example among a growing list of suffering EMs that includes South Africa, Brazil and Argentina.

"If we consider that the “taper tantrum” headache of 2013 was driven by the mere slowing of asset purchases, then their reversal should be a very long and painful hangover"

Their experience is just one symptom of the global liquidity drain and has, in turn, revealed a number of pain points across markets. If we consider that the “taper tantrum” headache of 2013 was driven by the mere slowing of asset purchases, then their reversal should be a very long and painful hangover. With less liquidity and the implicit support under overvalued asset prices being removed, we are likely to see much more extreme reactions going forward.

This represents both a risk and an opportunity for investors. It is a risk for investors that are reliant on areas like high yield credit and certain emerging market debt. At the same time, it is an opportunity for investors that are positioned to benefit from the underperformance of those asset classes and have a long volatility bias.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

2 topics

Vimal Gor

Head of Income & Fixed Interest

Pendal Group

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Expertise

Vimal Gor

Head of Income & Fixed Interest

Pendal Group

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Expertise

Comments

Comments

Sign In or Join Free to comment