Falling house prices: hype and reality

Michael Doble

APN Property Group

If house prices are falling as rapidly as some headlines impute, can we expect this to impact AREIT investors? Let’s begin by looking at the facts, rather than the headlines. Housing demand and supply ebbs and flows. Because of the lower barriers to entry there’s often volatility in residential housing.

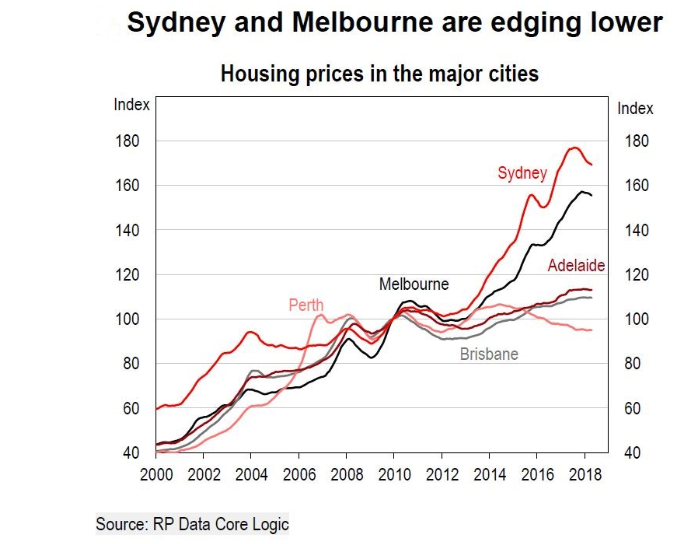

We’ve experienced a five year bull run in residential housing which has seen average Sydney house prices rise more than 75% to the middle of 2017. Melbourne was not far behind, growing more than 55% over the same period. It’s not surprising that after a sustained period of extremely strong housing growth, we’re now starting to see a price correction.This is part of a normal cycle.

In recent years, the high level of demand was not fully met by supply pushing price growth beyond long term averages. Housing price falls are the result of the market retreating to equilibrium. Unfortunately, the fall attracts a great deal of hype (which journalists love) that obscures this reality.

CoreLogic dwelling prices were flat month-on-month in March this year and have been flat-to-falling since mid last year. The year-on-year drop, however, was a mere 1.2%. It’s almost absurd that we are talking about a major housing correction. The basis of such surveys are also imperfect, not like-for-like comparisons of the same assets bought in one period then sold in another. They are a guide, albeit an imprecise one.

Residential values are best assessed over a three year period. On this basis we could witness capital declines of 10% and still have healthy long term capital appreciation over the period. Taking market moves from month-to-month (or even quarter-to-quarter) and then extrapolating them into an annualised figure, as many have been doing lately, might create an eye-catching headline but not much else.

We prefer to look at the long term drivers of residential property, starting with population growth. Last year, base population growth (births minus deaths plus immigration) amounted to around 388,000 people. But it is the temporary resident category – mainly international students – that is a big driver of residential demand in inner city Melbourne and Sydney.

UBS analysis of ABS data of recent migrants finds standard population growth understates the reality of booming ‘people growth’.

Temporary visas doubled from 285,000 in 2007 to a record 663,000 in 2016. More than half of these visas were held by students. In 2017, students on temporary visas reached a record high of around 400,000. They all need somewhere to live, which is why standard population measures understate the true demand for residential property.

Then there are the more traditional measures. Unemployment remains at an historic low of around 5.4% and wages growth, whilst modest at 2.1% a year, is at least keeping pace with inflation. Consumer confidence is steady and above levels seen for most of the past four years. These are not the conditions under which house prices usually crash.

Interest rates are more of a concern, especially with bank funding costs increasing, but they remain at reasonably low levels. Minutes from the Reserve Bank’s July meeting observed that “…while changes in advertised housing lending rates had not been in a particular direction overall, lending rates for new and outstanding variable housing loans had drifted downwards over much of the prior year.” House prices “had fallen moderately” in the major cities to date. Moderate is not dramatic.

And whilst household debt is at record highs, the servicing of it has improved in recent years. In fact, according to ABS and RBA data analysed by MacroBusiness, “while our gross debt has soared, what it costs us in interest (as a percentage of household disposable income) is about as low as it has been in 14 years.”

There is nothing structural, significant or material about the heat coming out of the housing market.

On the supply side, again there’s more hype than reality. Despite much talk about over-supply in certain sectors, especially low quality inner city apartments, according to the HIA, residential building commencements fell 8% in 2017.

Based on total population growth and predictions of demand based on average household sizes supply is broadly matching demand. In our view, the price weakness in residential property markets is part and parcel of a normal cycle, a product of the huge price growth of the past few years. Investors in the commercial properties have much less to worry about than media headlines suggest.

To the final question; what if the house price falls gather pace and the “wealth effect” kicks in?

Economists describe the wealth effect like this: When the value of our homes increase, it makes us feelricher, even if there’s not an extra cent in our pockets. We spend a bit more as a result. There’s a lot of evidence to support it (see this National Bureau of Economic Research paper by Case, Quigley and Shiller). The effect of housing wealth, especially compared with other assets, on consumption is particularly strong.

What’s less conclusive is whether it operates in reverse; when house prices are falling, do people reduce their spending?

Economists are divided on this issue. The NBER paper cited above first found that “households increase their spending when house prices rise” but that there was “no significant decrease in consumption when house prices fall”. It was, however, later updated after an extension of the data set, claiming there was a decrease in household spending.

Christopher Flavelle, meanwhile, cites in Slate a number of economists that don’t believe in the wealth effect at all. Anecdotal evidence from Australia’s recent house price boom might support this; there was no huge surge in retail spending as house prices rocketed, so why should a pull back lead to spending falls?

Right now, the argument is moot. There’s nothing in the current data that suggests current modest falls in house prices will accelerate. For AREIT investors, the issue is getting far more attention than it deserves. Best ignore it and move on.

Want to learn more?

here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is highly regarded in the real estate funds industry, with 31 years experience. He's held various senior roles specialising in real estate valuation, consultancy and funds management

2 topics

Michael Doble

Chief Investment Officer, Real Estate Securities

APN Property Group

Michael is highly regarded in the real estate funds industry, with 31 years experience. He's held various senior roles specialising in real estate valuation, consultancy and funds management

Michael Doble

Chief Investment Officer, Real Estate Securities

APN Property Group

Michael is highly regarded in the real estate funds industry, with 31 years experience. He's held various senior roles specialising in real estate valuation, consultancy and funds management

Comments

Comments

Sign In or Join Free to comment