Fed to go negative?

Chris Rands

Yarra Capital Management

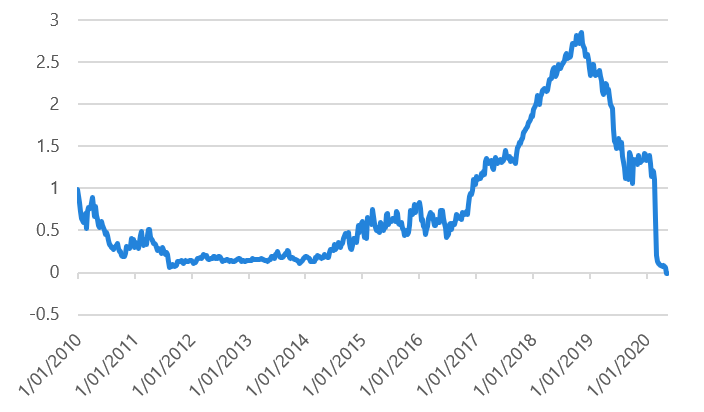

Before I dive into this, it’s important to understand why people are starting to think about the idea. The Fed Funds 12 contract (FF12), which is the market’s expectation for cash in 12 months’ time, just went negative. You can see this in Chart 1, where the expectation for cash in 12 months’ time fell to -1.5bps. This is the first time it’s fallen below zero.

Chart 1: Expected cash rate – 12 months’ time

Source: Bloomberg

Two things are worth pointing out here:

- While this is mildly negative at best, at no time over the past 10 years (during the GFC, Euro-crisis, etc.) did the market push this rate negative. The prior low in 2011 was around 6bps.

- If you don’t believe that the cash rate can go negative, then step right up, as I have a trade for you. Sell Fed Funds futures at a negative rate and when the market figures out that the Fed won’t do it, it will trade back to positive again. That is what makes this so topical. If the market didn’t believe it was possible, they would be selling this like crazy.

It’s worth noting that I’m not just saying this now because the market started pricing it. Here was a comment to Bloomberg two months ago when this mess was kicking off:

“The more I think about it, the more it makes sense to me that the U.S. cash rate will fall below zero some time very, very soon,” said Chris Rands, portfolio manager at Nikko Asset Management Ltd. in Sydney. “I wouldn’t be surprised if the U.S. tries negative rates, especially with the tailspin in oil now adding to the virus fears.” — Bloomberg, 9 March 2020

Three things cannot be hidden

So, why would the US go negative? There are three key reasons:

- The US government finances are a mess and will not be getting better any time soon.

- Everyone else is doing it.

- Central banks’ employment and inflation mandates are miles away.

1. The US government finances are a mess

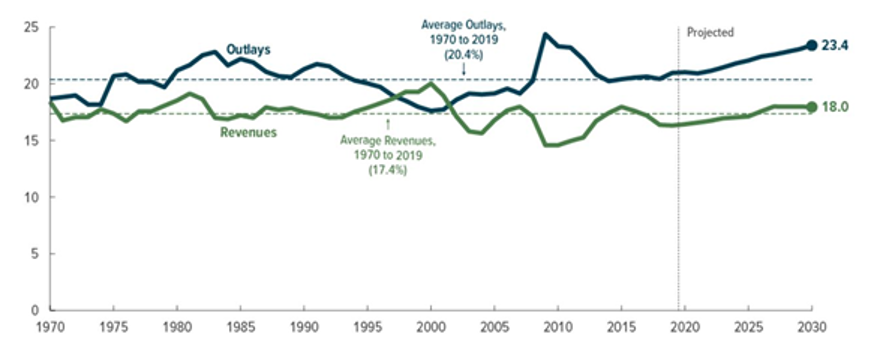

I recently did a presentation that focused on government finances, and the takeaway from that was it’s extremely hard to see how the US government is going to finance their huge deficits without holding rates down for a long time.

This was the chart I used in the presentation that showed the breakdown of the US government’s spending and revenues (which create the deficit) before COVID-19 hit. The green line shows expected US government receipts as a percentage of GDP, while the blue line expenditures as a percentage of GDP.

Chart 2: US spending and revenues pre COVID-19

Source: Congressional Budget Office

Because outlays are 25% larger than revenues it implied a 5% deficit going forward before COVID-19, a number which will spike higher now. This 5% of GDP is the equivalent of the US coming up with $1tn per year (yes trillion with a T). So, how could the US make this balance? Simple maths tells us:

- Cut spending by 5% of GDP—which would imply a 25% cut to total spending.

- Increase taxes by 5% of GDP—which would imply a 30% increase in taxes.

Given the way the US seems to think cutting taxes is the way to balance the budget, let’s just say for the foreseeable future tax increases are not happening (note: Trump’s tax cuts from two years ago have exacerbated this fiscal situation). Instead, let’s shift our focus on the spending side.

The Congressional Budget Office (CBO) tells us that 75%+ of US Federal Government spending goes to:

- Social security: USD 1 trillion, which includes an average benefit of USD 1,503 to 45 million retired workers.

-

Health care: USD 1.1 trillion, of which almost three-fifths went to Medicare to provide coverage for 61 million Americans aged 65+ or who have a disability. The majority of the rest went to 82 million low-income children, parents, elderly and those with disabilities.

-

Defence: USD 700 billion.

So, when you look at their budget and where it’s headed, it is difficult to see how it will balance. This is what we have been forecasting for a long time and is part of the reason why I usually expect rates to be lower than others, as the slow-motion deterioration of government finances has been visible for some-time.

In 2018, I wrote about the effects of an aging population:

“Like growth, demographics can have profound implications for government debt depending on how policy makers tackle its effects. There are two key mechanisms at play. Firstly, as a greater percentage of the population enters retirement it requires greater welfare spending from the government. Secondly, as the working age population declines it means that the number of people available to be taxed to fund those benefits decreases...

Given governments are reluctant to cut pensions and raise taxes for political reasons, the natural release valve is for the government to increase government debt to cover its shortfalls. This is what has been observed in Japan over the past 20 years.”

Now the point of this is to say that if you can’t balance the budget, then the best way to fund it is with the smallest interest bill possible. This requires interest rates to be as low as they can go.

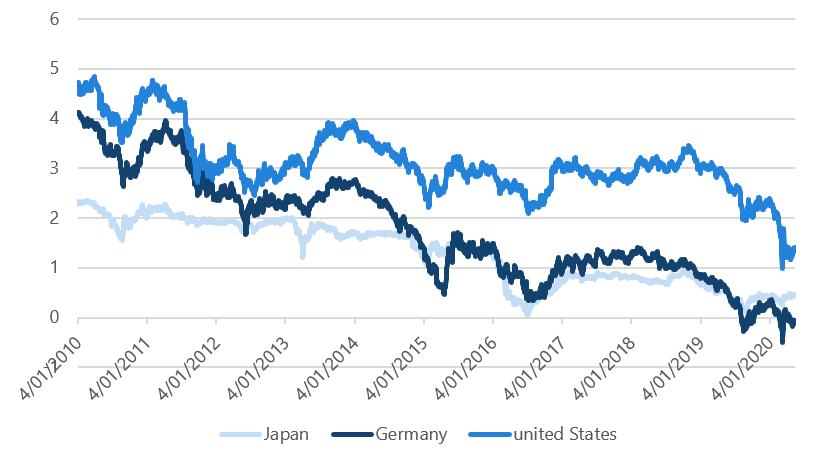

Here is the 30-year bond yields of Germany, Japan and the US. Germany is -6bps, Japan +44bps, while the US sits at +130bps. Time to get serious to fund this mess?

Chart 3: 30-year government yields

Source: Bloomberg

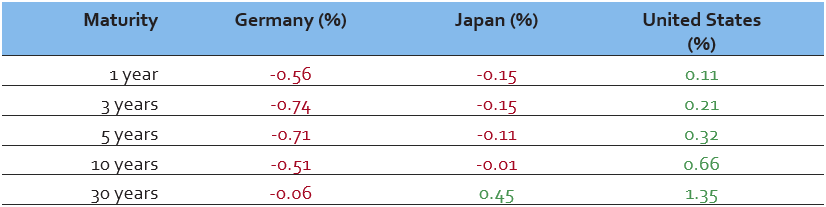

Here is the rate structure of the three economies. The entire rate structures of Germany and Japan are basically negative—the market is paying them to spend!

Table 1: Rate structures

Source: Bloomberg

What is the best way to keep funding a deficit that is clearly not sustainable? Take the cash rate negative and you won’t have to pay a cent…

Now, in ‘normal times’ this would not work as those bond vigilantes will sell your bonds until you become bankrupt. But when you couple it with central banks buying trillions of dollars of assets, it allows the government spending to continue.

(Note: I do think sovereigns will eventually be caught out playing this game—I just don’t think we are there yet. Italy could be a different story, but that will be for another time).

In my opinion, the choice for the US government once we emerge from this crisis will be: cut spending, increase taxes or cut rates. Unfortunately, the path of least resistance over the past 10 years has been to cut rates.

2. Everyone is doing it

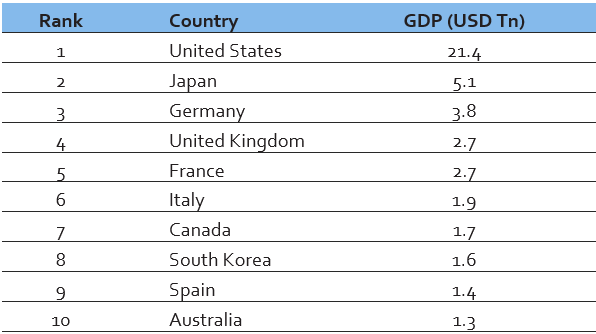

The second reason I believe rates will go negative is because the US Government debt load is going to be hitting levels that saw other countries going negative. Here are the world’s 10 largest developed economies by GDP. (Notable emerging market economy exclusions are China, India and Russia. They have a different investor base).

Table 2: Worlds’ 10 largest developed economies by GDP

Source: International Monetary Fund, Wikipedia

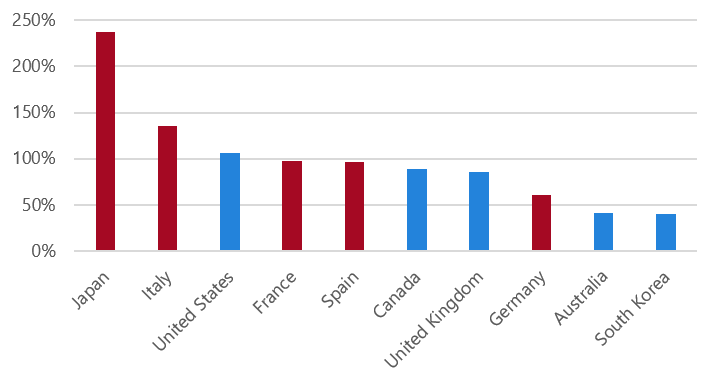

And the rankings of those countries by government debt to GDP (as at 2018). The countries in red are those with negative rates.

Chart 4: Government debt to GDP

Source: International Monetary Fund, Nikko AM

Chart 4 shows that all countries with government debt to GDP of around 100% or more (with the exception of Germany, which is caught up with the European experiment) have put in place negative rates. This implies that once your government debt gets too high you have to take drastic measures.

Welcome to the new normal. Where central banks are in control and deficits don’t matter.

3. Central bank and inflation mandates

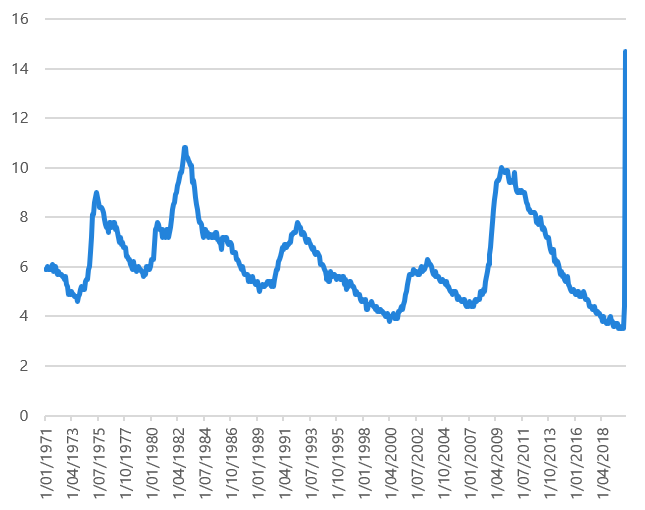

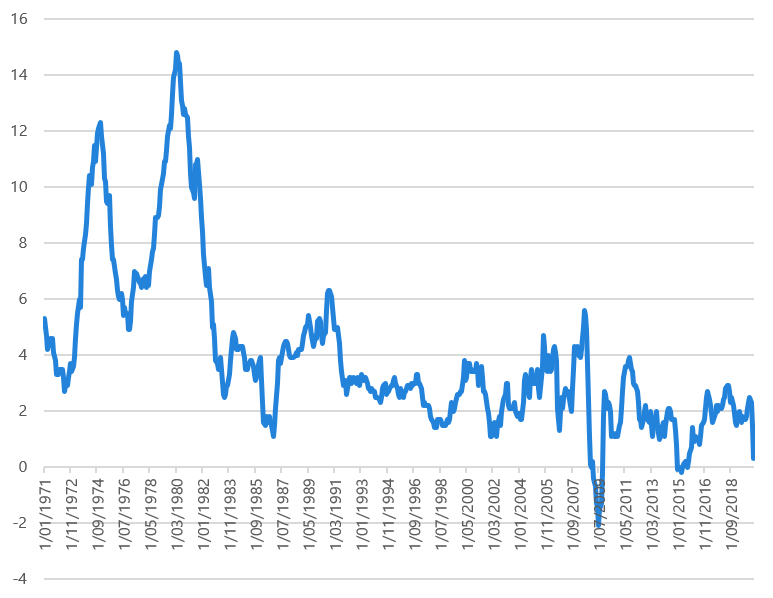

The last point to make is that inflation is likely going to be weak for some time and hence offers no roadblock to central banks taking drastic action. Let’s take a quick look at the dual mandate of the central bank: full employment and 2% inflation.

Here is the US economy at the moment:

Chart 5: US unemployment rate

Source: Bloomberg

Chart 6: US inflation rate

Source: Bloomberg

With 14% unemployment and 0% inflation, there is nothing holding the US back from drastic action. Looking forward, if we think about how this could improve into the future, the unemployment chart shows this takes a long time to correct itself.

Let’s be positive for a moment and assume that the actual unemployment rate lands at 8% once the economy reopens. Over the past four decades, unemployment has usually taken more than two years to go from 8% to 6%: 1983 to 1987, 1991 to 1993, and 2012 to 2014. So, even in a rose-coloured glasses scenario, 6% unemployment (not even full-employment) is likely not occurring until at least 2023. Given the US economy wasn’t consistently generating 2% inflation with an unemployment rate of just over 3%, reaching full employment is going to be a long time away.

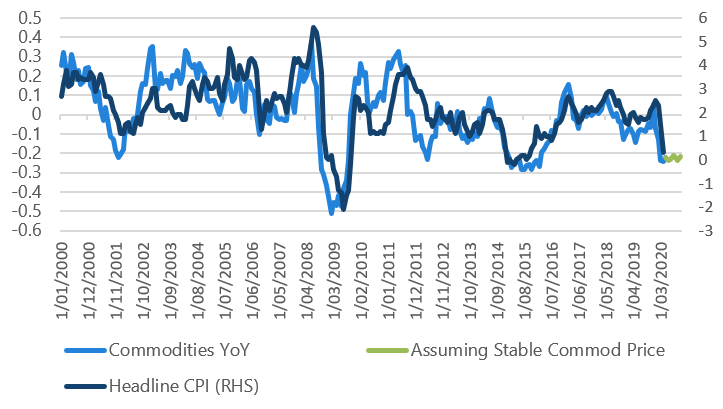

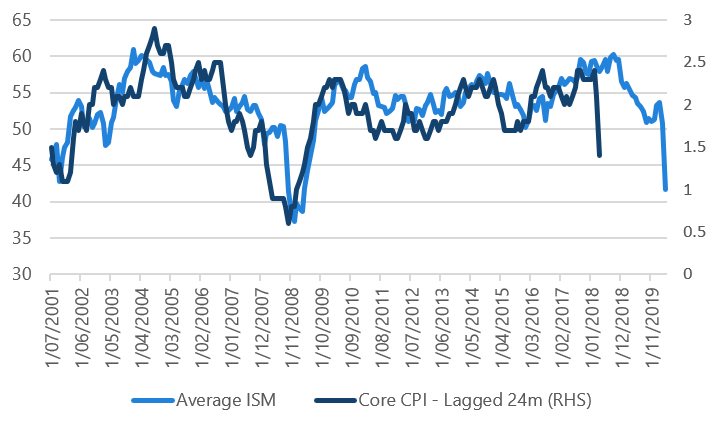

On the inflation front my indicators are looking particularly sour. Here are the two indicators (Charts 7 & 8) that I like to use for headline and core CP:

Weak commodity prices had pointed to the 0% headline figure that we just saw—so watch for a rebound in commodities if you want headline inflation higher. For core CPI, the business cycle had already been slowing when we came into this crisis. So, weakening inflation forces were already in place before the COVID-19 induced recession occurred. It is very hard to see what will drive inflation higher over the near term.

Chart 7: US headline inflation and commodities

Source: Bloomberg, Nikko AM

Chart 8: US core CPI and business cycle

Source: Bloomberg, Nikko AM

This would suggest there is very little in the way of economic outlook that will stand in the way of the Fed doing something drastic. In fact, it’s probably encouraging it.

Bringing it all together

When I put all this together—huge deficits to fund, debt levels well above 100% of GDP, and the Fed now years away from their dual mandate, I can’t help but ask myself “Why wouldn’t the Fed take rates negative?”

Now this is still going to feel crazy, but I will again share some research from the IMF which talked about this idea last year (good timing for them).

Enabling Deep Negative Rates to Fight Recessions: A Guide

The zero level of rates is not a law of nature, it is a policy choice:

“However, the zero lower bound is not a law of nature; it is a policy choice. The central message of this paper is that with readily available tools a central bank can enable deep negative rates whenever needed—thus maintaining the power of monetary policy in the future to end recessions within a short time.”

——Enabling Deep Negative Rates to Fight Recessions: A Guide, IMF, April 2019

To combat a recession, typically rates need to fall 500 to 600 basis points:

“500 – 600 basis points cuts in policy rates have been typical during recessions in advanced countries, but at present policy rates in most advanced countries remain too close to zero to make cuts of that size possible without using negative rates.”

——Enabling Deep Negative Rates to Fight Recessions: A Guide, IMF, April 2019

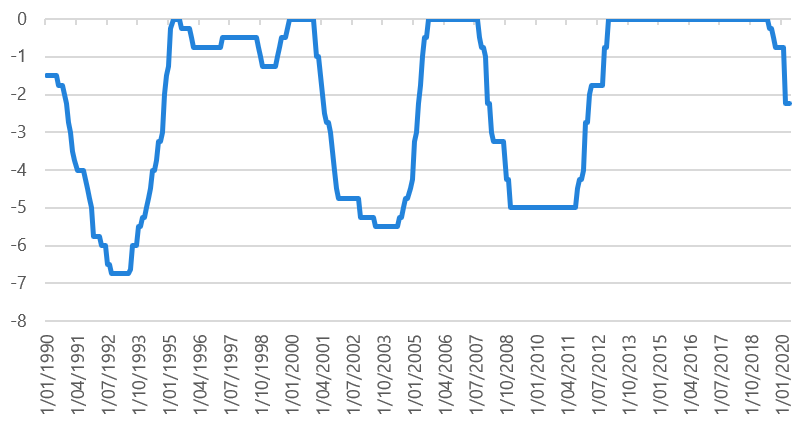

So far, US cash rates have fallen a little over 2% from their peak. You can see from Chart 9 below that this is a little under half the usual crisis move. (In this chart I take the current cash rate vs the peak cash rate over the prior four years. This gives a good sense of the total reduction that is usually achieved).

Chart 9: Change in cash rate vs 4-year high

Source: Bloomberg, Nikko AM

From this perspective I think that the Fed should already be considering this option, as it’s hard to determine how else the government intends to finance itself, and a race to the bottom in interest rates globally could tip their hand.

But with that in mind, let’s look at the most common criticisms that I would expect to see on the other side of the argument:

- A. “It’s not natural to have negative rates." This is true and I agree with it. From a long term perspective, it’s probably not a good policy as debt loads will just get higher. However across the world central banks have bought almost USD 20 trillion of assets, the ECB/BOJ have negative rates, the BOJ buys credit as well as equities, and the Fed is now buying junk bonds, credit, mortgage-backed and government securities. The time for referring to natural/normal is long gone and if that’s the only argument, it won’t hold up.

- B. “The Fed doesn’t want to go negative.” This is probably closer to the truth. But my personal view is it doesn’t matter what they ‘want’ or ‘believe’. The government has a huge funding task and they are going to be issuing USD 4 trillion of debt this year, while the Fed is going to be about as far away from their policy objectives as they can be.

I personally don’t think central banks have ‘wanted’ to do any of this, but the time for crazy policies is coming.

- C. They can just keep buying assets (QE) instead. This is another good argument and will undoubtedly help the government fund their deficits. But you can see from the rate structure across Japan and Europe that taking cash rate negatives pushes everything lower. The US 10-year bond has been stuck at 0.6% and cash has only fallen 200 points. If they want it even lower, they are going to have to do more. Additionally, if other countries start taking rates lower, the US dollar could keep going higher—reducing the ability for the economy to bounce back from its recession.

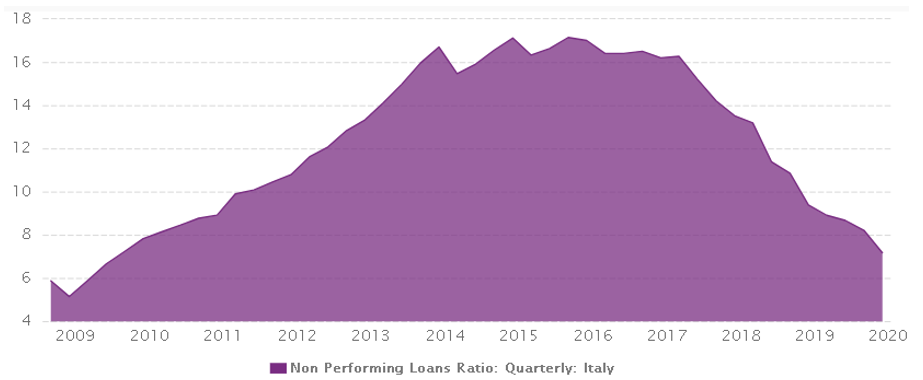

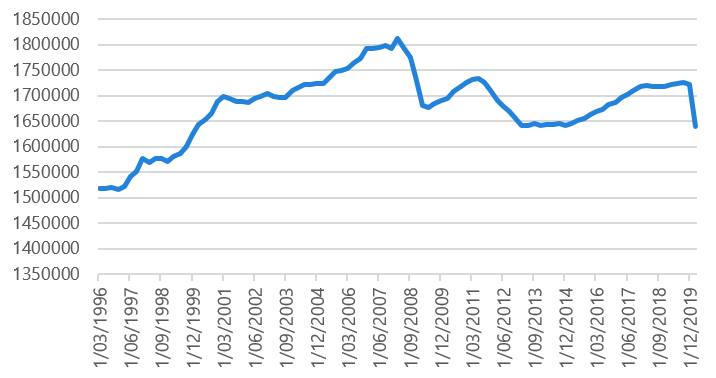

- D. The banking system does not perform well under negative rates. This is again a valid argument, but I think it overlooks the counterfactual. Yes negative rates hurt net interest margins (NIM) and seem to impair the banking sector, but it has also thrown a huge lifeline to some struggling economies. Let’s take a quick look at the Italian banking system below.

In the Italian banking system, non-performing loans peaked at 16% in 2014, having been on a non-stop rise as the Eurozone went from crisis to crisis. Coincidently however, these impaired loans started to improve at the same time that the EU commenced their negative rate program and QE.

Chart 10: Italy’s non-performing loans ratio from Jun 2008 to Dec 2019

Source: CEIC Data

For a country with 130%+ debt to GDP, no ability to spend because of their already large deficit, zero productivity growth and GDP growth of 0% (yes you read that right, the Italian economy in 2019 was the same size as it was in 2004) this seems like a remarkable feat. An absolute ‘Hail Mary’ of a pass from the ECB.

It looks to me that while negative rates have hurt some banks, it has redeemed others; creating more of a trade-off than a question of good/bad.

Chart 11: Italy’s GDP

Source: Bloomberg

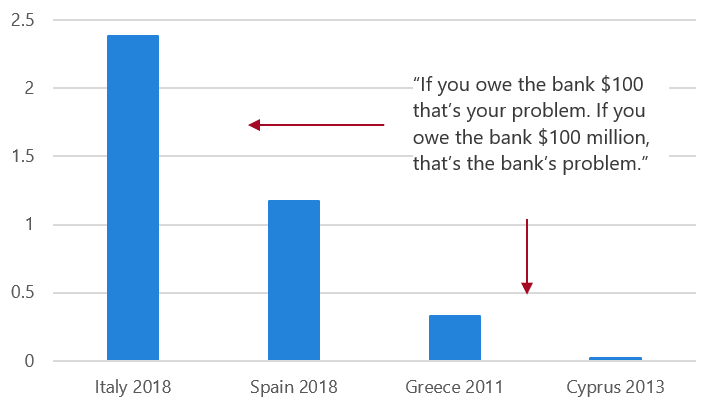

I used Chart 12 in a recent presentation, which shows the size of different government bond markets. Here we can see that the 2018 Italian bond market was monumentally larger than Greece’s was. Italian government bonds are around USD 2.5tn dollars compared with the Greek market where government bonds were ~USD 300bn in 2010. Even at almost 1/10th the size of Italy, it almost blew up the banking system.

It does remind us that one thing that hurts more than NIM compression is your sovereign defaulting.

Chart 12: Estimated size of government bond market (USD trillions)

Source: International Monetary Fund – Global Debt Database

To me, this argument suggests we are focussing on what occurred (negative rates didn’t generate inflation) and therefore saying that it didn’t work. No doubt this will rub some people the wrong way, but it’s the counterfactual that I am more interested in: we can’t observe what would have happened if they didn’t do it.

Conclusion

This view could turn out to be very wrong. The Fed might signal tomorrow that they really don’t want to do it and nothing they have said yet would confirm it. It is one of the more crazy central banking ideas. But even knowing that, I just keep landing back at the same spot: everything is pointing towards them trying it.

Stay one step ahead of the crowd

Our investment philosophy is based on identifying pricing anomalies. Inherent in this philosophy is the belief that markets are often incorrect in forecasting short-and medium-term influences and conditions. Keep up to date on where we believe the market has got it wrong by hitting the 'follow' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris is responsible for portfolio management, including portfolio construction and trading for various Australian fixed income portfolios including the Nikko AM Australian Bond Fund at Yarra Capital Management (Nikko AM was acquired by Yarra Capital Management in April 2021). Chris has over 9 years of experience in the fixed income market. He is also co-host of the popular Australian podcast series The Rate Debate.

........

This material was prepared and issued by Nikko Asset Management Australia Limited ABN 34 002 542 038, AFSL 229664 (Nikko AM Australia) who is the responsible entity and issuer of units in the Nikko AM Australian Bond Fund ARSN 098 736 255 (Fund). Nikko AM Australia is part of the Nikko AM Group. The information contained in this material is of a general nature only and does not constitute personal advice. It does not take into account the objectives, financial situation or needs of any individual. For this reason, you should, before acting on this material, consider the appropriateness of the material, having regard to your objectives, financial situation and needs. Investors should consult a financial adviser as well as the information contained in the Fund’s current Product Disclosure Statement (PDS) and the ‘Additional Information to the PDS’ which are available at www.nikkoam.com.au/pds before deciding to invest in the Fund. Applications will only be accepted if made on a current application form. An investment in the Fund is not a bank deposit and distributions and the return of capital are not guaranteed. Whilst we believe the information contained in this material to be correct as at the date of presentation, no warranty of accuracy or reliability is given and no responsibility is accepted for errors or omissions. Figures, charts, opinions and other data, including statistics, in this material are current as at the date of publication, unless stated otherwise. The graphs and figures contained in this material include either past or backdated data, and make no promise of future investment returns. Past performance is not an indicator of future performance. Any economic or market forecasts are not guaranteed. Any references to particular securities or sectors are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities or sectors and no warranty or guarantee is provided that the positions will remain within the portfolio of the Fund.

1 topic

Chris Rands

Co-Portfolio Manager, Fixed Income

Yarra Capital Management

Chris is responsible for portfolio management, including portfolio construction and trading for various Australian fixed income portfolios including the Nikko AM Australian Bond Fund at Yarra Capital Management (Nikko AM was acquired by Yarra...

Expertise

Chris Rands

Co-Portfolio Manager, Fixed Income

Yarra Capital Management

Chris is responsible for portfolio management, including portfolio construction and trading for various Australian fixed income portfolios including the Nikko AM Australian Bond Fund at Yarra Capital Management (Nikko AM was acquired by Yarra...

Expertise

Comments

Comments

Sign In or Join Free to comment