Gold – The Fed, Trump and Holidaymakers

Gavin Wendt

MineLife

Gold’s best friends at present are the US Federal Reserve and Donald Trump. The US dollar is weakening as the opposition of two more Republican senators to the US healthcare bill this week meant the measure is effectively dead in its current form.

The broader dollar index has touched a more than 10-month low, on reduced confidence in the President's agenda and comments by Janet Yellen that suggest a more dovish approach to US interest rates than the broader market had been factoring in. Rates will rise, but at a much slower pace than markets had been expecting.

Figure 1: US Dollar Index

The US dollar is a victim in all of this, as investors that had been factoring in multiple rate rises will likely only see one more during 2017. Evidence shows that the currency has been falling steadily throughout 2017 – down around 7% so far.

Multiple distractions on various fronts, but in particular national security, have meant that Donald Trump’s policy agenda has been thrown off course and significantly delayed. In fact the Trump rally appears to be stalling badly, as false promises come to fruition and he struggles to execute policies in the face of powerful vested interests in corporate America and Wall Street. And how much of what Trump promised is actually deliverable? The world is changing rapidly, posing risks to any sort of conventional economic recovery.

As a McKinsey study highlighted recently, ‘Even if we rebuild factories here and you build plants here, they’re just not going to employ thousands of people - that just doesn’t happen,” said report co-author and McKinsey Global Institute Director James Manyika. “Find a factory anywhere in the world built in the last 5 years - not many people work there.”

In fact the Trump rally appears to be stalling badly, as false promises come to fruition and he struggles to execute policies in the face of powerful vested interests in corporate America and Wall Street. And how much of what Trump promised is actually deliverable? The world is changing rapidly, posing risks to any sort of conventional economic recovery.

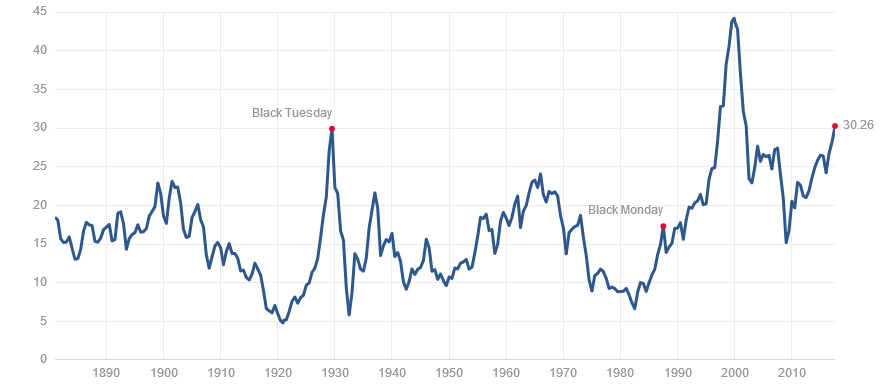

Figure 2: Robert Shiller’s CAPE Index

Robert Shiller, Nobel Laureate economist, told CNBC last week that investors should be cautious about investing in US stocks in such ‘an unusual market.’ The CAPE index that he devised thirty years ago is at ‘unusual highs’ which is concerning. The Yale professor advised, ‘One should have a little of everything if one hasn’t diversified this would be a good time to do that.’

Trump delays and scandal has weakened the US currency and benefited gold. Despite this, record-high equity prices and bond prices with higher U.S. bond yields appear to have kept a lid on gold and silver prices, which would normally have seen greater gains in an environment of such uncertainty.

Let’s not forget too that rising interest rates per se aren’t necessarily negative for gold – the key is the real interest rate – that is, the current nominal rate less the rate of inflation. The Fed's perception of inflation is rooted in data and calculations, but for most ordinary US citizens the anecdotal evidence is that things are getting more expensive. Not only that, but their dollar is being stretched compared to its purchasing power over past years.

The Fed's stated 2% inflation target is therefore a mirage, as the cost of living has been moving higher at a faster pace than the Fed seems to believe in its analysis. Interest rates around the world fell to their lowest levels in history post the GFC, and even though the Fed has been tightening credit since December 2015, they remain at a very low level of 1.25%.

The takeaway from all of this is that the real interest rate in the US is effectively negative – as the real rate of inflation is greater than the current nominal interest rate. So even if we factor in multiple interest rate rises, the real interest rate will remain negative.

What’s significant about this in the context of the gold price is that over the past five decades at least, when interest rates have been below the level of inflation, gold has outperformed.

In my view this likely presents a turning point in gold’ fortunes, given the volume of recent selling by traders in ETFs and other instruments related to the yellow metal based on the belief in a more hawkish Fed approach to monetary policy.

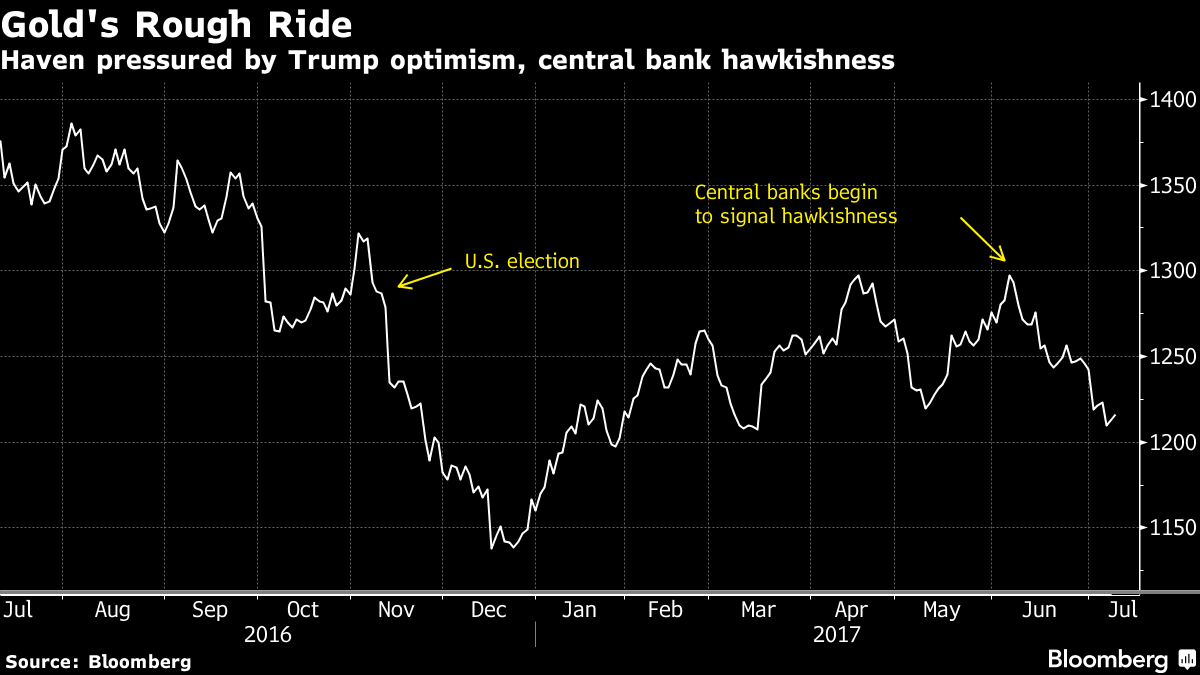

Figure 3: 12-month Gold Price Performance

Further underlining the timing of the current investment opportunity is the seasonality of the yellow metal’s recent relative price weakness. The typical selling leading into the Fed’s most recent rate hike contributed, but what many like to call the “summer doldrums” are very much in play.

Gold has typically suffered a seasonal lull during the northern hemisphere summer, as investment demand tends to wane as investors concentrate on holiday distractions. There’s also a lack of any major income-cycle or cultural drivers of investment demand.

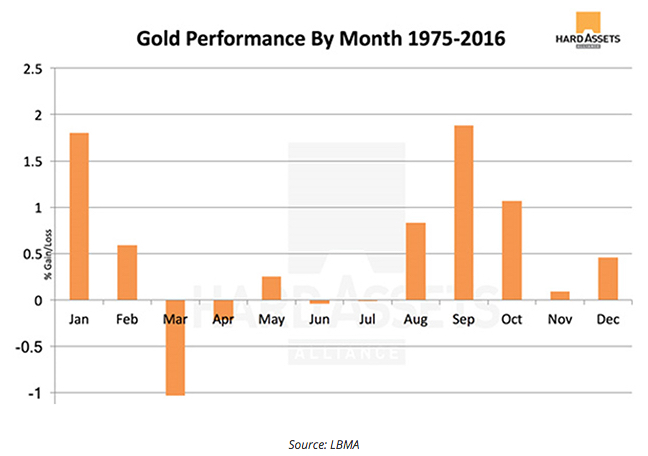

Figure 4: Seasonal Gold Performance

However for the past three US interest rate hikes, gold had a good up leg for three months each time, with the corresponding weakness with dollar index. The odds are reasonably good that gold will have a similar bounce over the coming months.

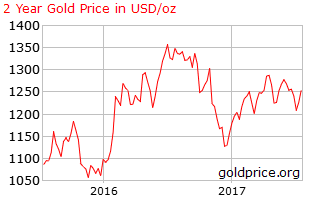

In fact, gold and silver have been the quiet achievers in the metals sector so far during 2017. This will come as a surprise to many, given the generally negative tone permeating commentary around the precious metals sector. Gold and silver were amongst the best performing assets during H1 2017 - with gains of 8% and 4% respectively. Interestingly too, gold has risen in value in terms of virtually all major currencies with the exception the euro, where it fell by 1.2% during the first half.

Figure 5: Two-Year Gold Price Chart

The world’s biggest gold-buying market, India, has certainly seized upon the opportunity that has presented itself so far in 2017. Gold is once again pouring into India following the catering of physical demand last year to a seven-year low.

Physical demand for gold has surged in India since January, following a plan by the Indian government last November to "demonetize" the equivalent of US$220 billion in large Indian bank notes, which had a disastrous effect on the gold trade and other sectors of the Indian economy that are reliant on cash transactions.

Quoting data from GFMS Thomson Reuters, India imported 521 tonnes of gold between January and June, compared to 510 tonnes for the entirety of 2016. Value-wise, the H1 2017 figure for gold imports was $22.2 billion versus $23 billion for 2016. If those numbers hold up, the annual total could surpass 900 tonnes, or $40 billion, which would be the strongest year since 2012.

Summary

Gold has been somewhat battered over the recent past; however there remains little reason to panic for medium to long-term investors. There is presently a buying opportunity with several triggers for upside. Real interest rates are likely to remain negative in the years to come, even despite recent hikes. Accordingly, we maintain confidence in our base-case gold price target range for the yellow metal during 2017 of between $1200 and $1300/oz.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

6 topics

Gavin Wendt

Founding Director

MineLife

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

Expertise

Gavin Wendt

Founding Director

MineLife

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

Expertise

Comments

Comments

Sign In or Join Free to comment