Robust Commodity Outlook

Gavin Wendt

MineLife

Given recent headlines and speculation with respect to commodity prices, I thought it worthwhile to outline my views on the near-term picture. Overall, I remain very optimistic with respect to prices and demand. In particular, recent positive Chinese commodity demand data and outcomes from the recent Chinese Communist Party Congress, will provide markets with direction and confidence.

Iron ore remains enigmatic. There’s been ongoing volatility in price, but it’s fair to say that its overall price performance has exceeded all expectations over recent years. The latest price retreat is just the latest phase in this cycle of volatility.

Iron ore use in the world’s biggest consumer, China, remains robust despite authorities’ closure of independent, lower-quality steel producers. Demand at the premium end of the steel industry has increased, as the Chinese steel industry continue to evolve.

The latest data for September reflects this. China's imports of iron ore jumped 10.6% year-on-year to a record 102.8 million tonnes – a surge from 88 million tonnes imported during August. Iron ore imports for the nine months to September are up 7.1% 817 million tonnes and well on track to end the year well above 1 billion tonnes.

The same thing is happening in the coal sector.

In fact China’s coal imports during September rose to their highest level since December 2014, as Beijing’s safety and environmental crackdown curbed output at domestic miners. Coal imports jumped nearly 11% to 27.08 million tonnes last month, compared to the same period a year ago. They were also well up on the 25.27 million tonnes imported in August.

Imports for the first nine months of the year were up 13.7% to 204.85 million tonnes, reflecting strong appetite for the fuel despite the country’s effort to cut coal consumption and put it on track to beat the record 255 million tonnes imported in 2016.

What about other key commodities?

China imported 9 million barrels of crude oil a day during September – which is up 1 million barrels from the 8 million for August this year and September 2016, and above the 8.5 million barrels a day average for January to September.

China’s imports of copper and copper products climbed by 26.5% year-on-year during September, whilst shipments of unwrought copper - which includes anode, refined, and semi-finished copper products - reached 430,000 tonnes last month. This is equal to the figure for March and up 10% from August's 390,000 tonnes.

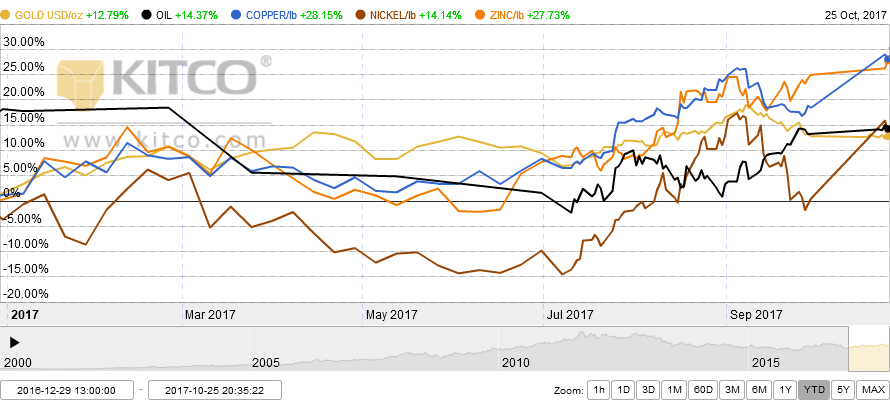

It's been a solid period for most commodities – with copper, nickel, gold, zinc and oil all performing solidly. This is reflected in their H2 2017 performances in the graphic below.

What’s also interesting is that other more obscure metals - like vanadium, tungsten and various rare earths like neodymium - have joined the price party. The common denominator amongst these metals is that they are predominantly produced in China and they have all been hit hard by Beijing’s recent environmental crackdown. Chinese premier Li Keqiang pledged at the annual National People’s Congress in March to make “our skies blue again”.

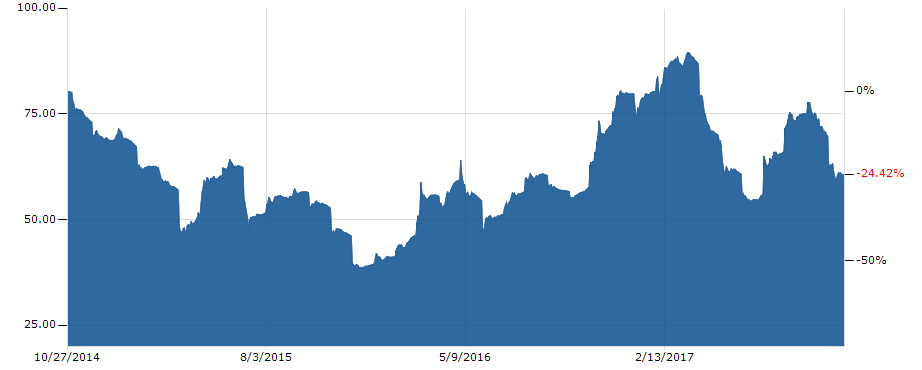

The graphic below is also interesting because it shows the performance of the ASX Small Ordinaries Resources Index over the course of the past 12 months. It’s a heart-warming picture indeed.

Given the inherent volatility in world affairs – think Trump, North Korea etc - this chart does come as somewhat of a surprise. Nevertheless, what it does reflect are a combination of factors – most importantly the seeming resilience of Chinese commodity demand, as well as a greater appetite for risk on behalf of investors.

At the same time there are obvious supply constraints, as the world’s miners have learnt from past lessons and maintained quite a deal of balance sheet restraint in terms of spending on new projects/acquisitions. This is a far cry from the disastrous forays by RIO and BHP over the past decade into ill-timed/ill-conceived expansions - such as shale oil & gas, aluminium, potash and coal – where many tens of billions of dollars of shareholders’ funds were wiped away.

Driving interest at the present time are speculative developments in the Pilbara region of WA (conglomerate gold), the strong A$ gold price that continues to drive domestic producers, growing appreciation of the demand opportunities for a whole host of commodities related to the burgeoning electric vehicle industry and strong commodity prices right across the board.

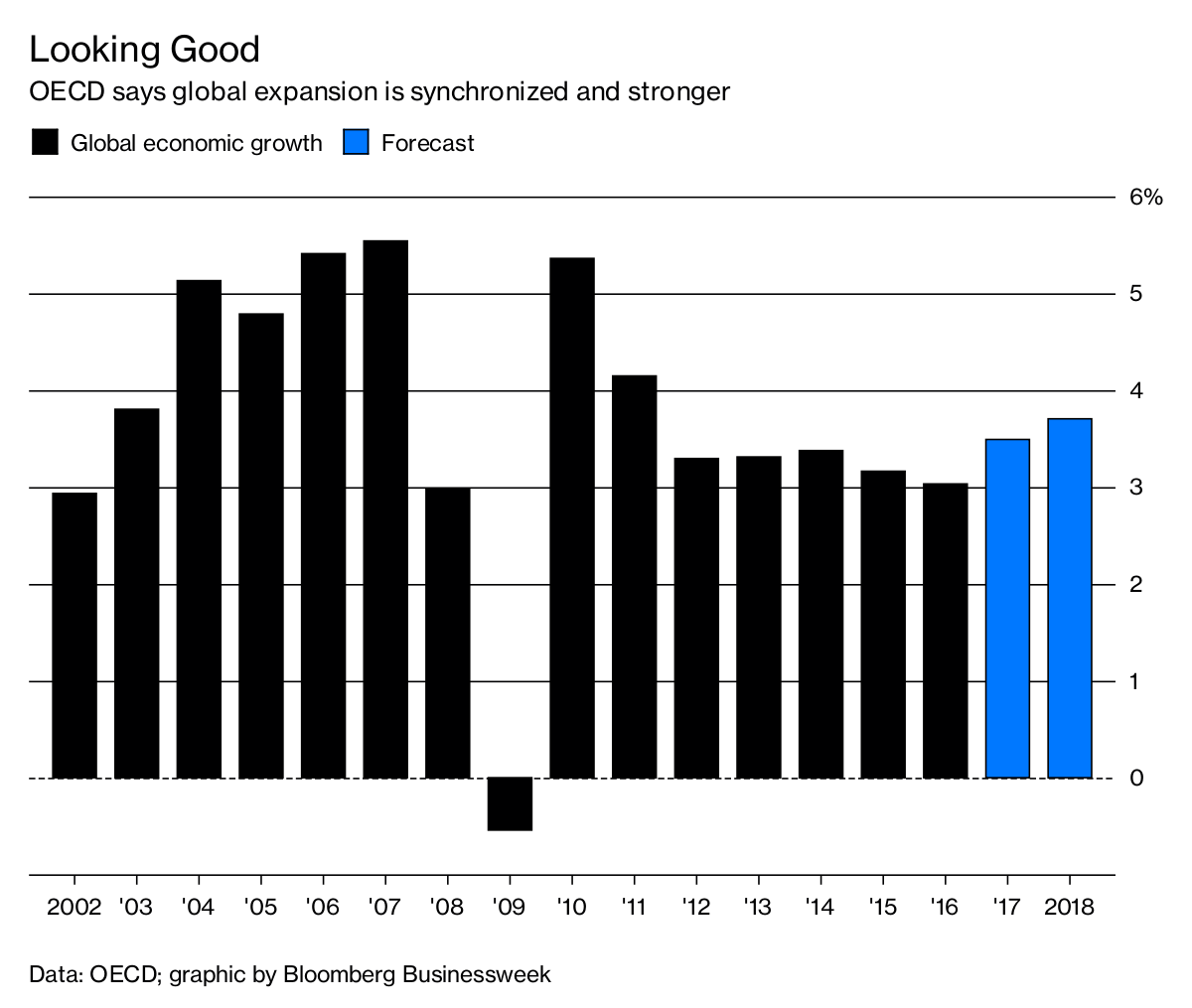

From a broader perspective, the global economy is getting stronger and is forecast to grow at the fastest pace since 2011 this year, according to the OECD. Expansion will accelerate next year, with the biggest economies all contributing, the OECD says in its Interim Economic Outlook.

In the background we have China’s 'One Belt, One Road' initiative. The plan is to build a vast network of new trade routes across the globe, incorporating multiple high-speed rail networks to penetrate Europe, massive ports across Asia and Africa and a series of free-trade zones.

China is going to spend up to a trillion dollars on infrastructure projects and hopes to bind more than 65 countries and two-thirds of the world's population to its economy. It’s a massive global development undertaking that will require enormous commodity usage.

Finally, if President Trump can finally get some traction on the policy front, we might see some realisation of his proposed infrastructure renewal spending plans, which would deliver the boost to commodity demand that was anticipated in the wake of his election a year ago.

To conclude, ‘volatility’ is more than ever the buzzword of modern times – whether that is in an economic or political context. And it’s certainly applicable to commodity markets too. Nevertheless, I believe world economic growth is on a steady footing and there are various factors that will help support commodity prices and maintain momentum within the sector.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

9 topics

2 stocks mentioned

Gavin Wendt

Founding Director

MineLife

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

Expertise

Gavin Wendt

Founding Director

MineLife

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

Expertise

Comments

Comments

Sign In or Join Free to comment