There is no substitute for guts, vigilance and hard work: Marcus Padley

For Marcus Padley and his investors, it’s been a remarkably good six months during a year in which markets are straddling the boundaries of health, economic and geopolitical crises in the midst of the worst pandemic since the Spanish Flu.

Padley’s ~$60 million Marcus Today Growth SMA is up 9.32% year-to-date against a market down 12.9%, and since the start of the “Corona Crash” has outperformed the index by 23.16%.

But it wasn’t simply a stroke of luck. Having been burned in the past, Padley and his team have fostered their own unique approach to investment. Buy & hold ‘Buffettisms' have been cast out in lieu of pragmatic objectivity, informed timing and the guts to go 100% cash, which they have done three times in the last year. Cash, he says, is an underutilised asset which he labels as the "only defensive stock".

Come COVID-19 the Marcus Today team was match fit; picking with precision the moment to exit, enter and now exit the market. The fund is currently in 100% cash yet again.

"Making these sort of timing calls requires a lot of hard work and hyper-vigilance. There is no easy way to manage someone else's money. Its work. It's what we're paid for. Activity, not inactivity."

In his usual no-mincing-words style, Padley shares with me his strategy and outlines the steps you too can take to become a better investor today. He also discusses why his SMA is once again in cash, and as a bonus, recounts tales from London that may reshape the way you think about life and business.

MARCUS PADLEY, MARCUS TODAY

Can you explain the Marcus Today investing philosophy and whether you invest in your own strategy?

Yes, I invest in my own strategy. Emma and I have ‘skin in the game' as they say. Our SMSF is in the fund and any spare cash we get we roll in there as well. I see it as managing my family’s investments and the other investors are just along for the ride!

At the core, our everyday processes are very similar no doubt to what a lot of other fund managers and investors are doing. We use ‘every tool’ which means anything that works, both fundamental and technical. What is unique about our investment philosophy is that we have a mandate which allows us to go to 100% cash and we use it. Simple as that. We have cashed out three times in the last year, when we have detected precipitous moments.

We developed the philosophy quite naturally, because we decided to treat the money as we would our own (some of it is our own after all). All investors want to be protected from market corrections, but the reality is that most financial advisers, whilst they might be brilliant at structural advice, tax, superannuation legislation, etc., are not fund managers, and for some of them the investment process is an inactive afterthought executed through an unsophisticated percentage mix of asset classes effected through managed funds. The net result is that the investor's money is managed in the "long-term", which is another way of saying, it isn't really managed at all.

We offer an aggressive equity fund.

As Bobby Axelrod says we are in the moving business, not the storage business. We are actively managing our investors' money, doing what they want us to do, doing what we would do for ourselves, which is, simply, attempting to avoid the corrections and participate in the uptrends. We call it "Step performance". Step up, step out, step up, step out. It's a nirvana, but it has worked tremendously well in the recent volatility.

On top of that, when we are invested, we are similarly aggressive in our stock picking and timing. We are not buying the Moron Portfolio. We are active. Using decades of experience, and thousands of dollars worth of software, information and tools.

I have written an article on Livewire about some of the basic principles of what we do (20 ways to beat the herd). It involves hyper-vigilance, decisiveness and a willingness to go "all-out" when it gets dangerous. A long way from the traditional excuse for investment, which is to do some fundamental research, buy a stock and hold it forever.

We're doing something more imaginative. Investing with us comes with an insurance policy not available anywhere else. You know we'll get you out. That’s why big funds are so disappointing and are shunned by many individuals who end up ‘taking control’ (which they don’t really want to) and doing it themselves. Because they don’t trust big funds to actively manage their money, and in particular, to at least attempt to avoid GFC and Corona Crash style events.

Can you list 2 to 3 that are your biggest pet peeves and why?

Good question. Yes. Let's start with this:

1. You Can't Time the Market - Someone did an academic study some years ago, decades ago, saying that you can't time the market. It is all the finance industry needed, an excuse to do nothing. They have been quoting it ever since. If you can't time the market then after a financial adviser has sold you a product there is nothing else to do, they can move on to selling the next client. Not being able to time the market absolves a financial product seller from having to manage a client's investments. Perfect. The problem, of course, is this: if you can't time the market, then what value are you adding? Why is the client paying for your ongoing services? You have to time the market, you can time the market, and anyone who tells you they can't is to be avoided.

2. The use of any Warren Buffett quotes - I once got an email from an editor, he had just moved over to finance from the gardening section of a national newspaper. He told me (a veteran of 17 years writing articles in the business section) that I needed to use more keywords because "there is an Internet you know". Coming from a print media company that was being destroyed by carsales.com and realestate.com, I had to hold back my laughter. But he was right, and it had taken a young gardener to join the finance section to try and drag all his writers into the new world. I Googled the seventy-five top keywords in finance and proceeded to weave every single one of them into that week's 750-word article, which was about the sad need to use keywords and how it was going to destroy good writing. The final line was "This is probably the most boring article I've ever written, but it will almost certainly generate the most clicks". It was the only article the newspaper refused to print. Clearly they love digging up the truth, just as long as it doesn't expose them and their clickery trickery.

So what are the top keywords in finance? I’ll tell you the top ten. They are Warren, Buffett, Buffett, Warren, Warren, Buffett, Buffett, Warren, Buffett, and Warren. If you want clicks, put them in your article ten times, if you want sales of your lame financial product, put them in advertising ten times, if you want to project the subtle impression that you are smart and that Warren Buffett endorses your book, put them in your book ten thousand times.

The bottom line is that quoting Warren Buffett is done for marketing purposes, and if you for an instant believe that someone using Warren Buffett quotes is more impressive for it, more fool you. Let's face it, if anyone could invest the Warren Buffett way some fund manager would be doing it, we'd all be invested, and we would all be billionaires. It can't be done. And if anyone has anything wise to say about investment, say it, don't repeat something someone much smarter than you said, again and again. It's mindless, we've all read them, you're not clever.

You have the ability to go to 100% cash. Without giving away your secrets, can you show 2 to 3 of the inputs that help you make such a decision?

- Consensus opinion. The whole team has to agree.

- Charts. We are not driven by technical analysis, but most of the timing comes from watching the herd and charts are a brilliant way to do that. It is all about spotting and reacting to the big pivot points. You can't do that on fundamental analysis. You will never time stocks or the market using fundamentals. If all the Kings and Queens, presidents, prime ministers, dictators, bankers, central bankers, brokers, financial advisers, currency traders, bond markets and even the taxi drivers couldn't spot the GFC, then no one can. But you could have spotted it on a chart.

- Volatility. A sharp rise in volatility in a stock or the stock market is a sign that the trend is liable to change. Very low volatility suggests overconfidence. A sharp increase from very low levels of volatility often mark significant pivot points.

You obviously made some cracking calls during the COVID crash; going to 70% cash on February 20, and then "all in" on March 24, and more recently, all out again on June 12. Can you walk us through the thinking behind those big calls?

The setup for success this time around came from failures in the past. In particular, during the correction in 2018 when the market fell 15%. Our fund fell 23%. I spoke to a few other fund managers about the October to Christmas 2018 period, and I can tell you, although some funds management groups look like faceless professional institutions, behind them all are individuals who live and die by their performance, and in this period they took some serious mental punishment. So did I. There were three lessons from 2018 that formed the basis of what we have done so successfully this year.

- The power of cash - Initially in the 2018 correction we did fantastically, going to 67% cash within a couple of days of the top. All the ingredients were there for a sharp sell-off. Prior to that, we had been doing a lot of index hugging relying on stock selection for outperformance, which hadn't really worked. We outperformed in cash, significantly. We had been fighting for tenths of a percent of outperformance in a rampant bull market, and it was hard to come by. Suddenly we were outperforming by multiple percent in a day. We had not seen that before. We learned the power of cash. You have no risk. You have buying power. It was the first lesson.

- Cash is the only defensive stock - After our initial cash out we got sucked back into the market on the first bounce and wore the next two significant down legs. We had bought back into quality stocks, ALL, TWE, CSL, COH, RMD to name some. They massively underperformed. And that was the second lesson. If the market is on the move, it will take everything with it, and a quality stock will not protect you, in fact, it will hurt you more. Quality stocks tend to trade on higher PEs, and they hollow out more quickly in a sell-off. There is no defence in a falling market. Cash is king.

- There is no substitute for vigilance and hard work - The third lesson was that rather than bury our heads in the sand and ignore the market over Christmas, hoping for the best, hoping it would all just go away, we remained hyper-vigilant. I was supposed to be relaxing with the family, on the beach, going for runs, windsurfing. Instead, I was on Skype every morning discussing the market. I kept writing the newsletter and managing the fund and thanks to that holiday-ruining extra effort, that hyper-vigilance, when we saw the same signs we had seen at the top, at the bottom, we got fully invested again. It was almost perfect timing. Making these sort of timing calls requires a lot of hard work and hyper-vigilance. There is no easy way to manage someone else's money. Its work. Its what we're paid for. Activity, not inactivity.

I note that your SMA does not invest in bonds or global equities. Do you believe these asset classes have a role in portfolios?

Of course they do. But we are offering a focused Australian equities fund, not a diversified portfolio including multiple asset classes. We'll leave that to the financial planners. We are specialising, in one asset class. Hopefully, there are enough investors wanting us to manage the Australian equities component of a bigger portfolio to make that specialisation profitable for us. We have considered starting an international equities fund, but for now, we have decided that we are going to focus all our attention on our current funds.

We owe it to our investors and truth be known, whilst there are clearly much better growth options outside of Australia, we don't yet have the resources to support an international research capability. We would be pretending, and attracting money because of our brand reputation rather than our international funds management capability. We would be stepping outside our sphere of competence. When we get to a billion in Aussie equities will think about it. Until then, we'll stick to our knitting.

One of the strongest views you have expressed is that "growth beats income". What would you say to a typical Australian investor who chases dividends and franking credits?

A dollar is a dollar whether it comes from dividends, a cash refund from the tax office, or a capital gain, and whilst I wouldn't want to burst the bubble of the traditional yield reliant retiree, chasing income stocks has not only cost money because of the pitiful bank sector performance, it has always cost you money because it corrals you into low growth mature companies with few growth options and nothing better to do than return money to shareholders. And more expensive than all that has been the opportunity cost (lost) of not holding quality growth companies with high returns on equity just because they had low yields. I have done some numbers.

Over 20 years the total return (includes dividends) from the CBA is 659%. The NAB 137%. The ANZ 369%. Westpac 351%. Telstra 55.2%. The Total return from the All Ordinaries has been 330%. If you picked big stocks on ROE (return on equity) instead of yield then the total return from CSL is up 3443%. Aristocrat Leisure 738%. Macquarie 1084%. RedMed 2340%. ASX 1093%. Ramsay Health Care 11589%. A2 Milk up 3488% (in just 5 years). And these are just stocks in the Top 50.

The conclusion is that you'll get a superior total return from companies with a high ROE and low yield, than you will from mature companies with few growth options, low returns on equity, high payout ratios and high yields. It's obvious, reinvesting profits at high rates of return will build an asset and a share price.

Cash cows that pay all their profits to shareholders will not grow. Don’t tell anyone, but 20% compounding growth and no yield beats a 9% yield and no growth. Always has and always will.

In the United States they will tell you that bonds are for income and equities are for growth. The American equity market culture is to reinvest for growth all the time, which is why Microsoft and Berkshire Hathaway resisted paying dividends for decades. In the US paying a dividend is seen as failure, the sign of a company lacking ideas and ambition. That culture is why the US market yields 2.5% whilst Australia yields 4.5% plus franking or around 5.89% on average.

Because Australian CEOs pander to the siren-like obsession of their Australian shareholders who want income and, an absolute red herring, a fully franked yields. Those cash refund cheques are a drug. But they are blinding millions of Australians to the growth in share prices available from low yielding companies. With term deposits paying around 1% it just doesn't make sense for companies to give money back to a shareholder, not when the company's return on equity is 20%. Far better they keep it and reinvest it at 20%. A high yield is a warning, not a beacon.

The bottom line is that if you are bothering to take the risk in equities you would be far better to focus on total return rather than dividend yield. Yields, franking and the cash refund, in particular, are distracting retirees from the best stocks in the market. You would be better to filter for high ROE and low yield than a high payout ratio and a high yield. Of course, you will have to sell shares to buy groceries, but if you can get your head around that little conundrum you'll be eating avocado smash for breakfast in your nursing home and going to bed dunking chocolate digestives not plain.

You list a lot of great tables with stock ideas in your wires. What are 2 to 3 of your unconventional strategies to generate such stock ideas?

- Technical scans - It's not unconventional but we do, as many vigilant investors do, scan the whole market, which is over 2000 stocks, for technical signals every day. It's a great way to pick up on stocks changing trend.

- Using inside information - No not illegal inside information, but information that is all around us. For instance, we are in the finance industry. We have a very good handle on which companies are succeeding and failing in our industry. We run an SMA on the Praemium platform. A few years ago their customer service was woeful and we worked out that it was because they were growing so rapidly. It's now a lot better by the way. But armed with that insight we bought HUB24, Praemium and Netwealth. The SMA industry was booming. In another example, I made a small fortune out of Mortgage Choice in 2012, when I spotted a friend of mine with a Mortgage Choice franchise on Facebook. He had bought an expensive Mercedes and gone on holiday to New York with all his children. I had a look. Numbers were good and the price was beginning to trend up. I bought it at 150c. It ran over 300c and I sold it when it had its first big correction. We all have our own inside information. Ask yourself, who do you know that is doing well (or badly), what industry are they in, is there a listed stock that would work as a proxy for that theme?

- TV advertising – I keep a lookout for companies that start advertising on TV. We would love to advertise on TV but we wouldn't do it unless we had cash to burn. If you're advertising on TV, especially in this day and age, it means you have a lot of money and are succeeding. Many years ago I picked up on Webjet this way. You probably know the ads. Making money in stocks is about probability not certainty. Your odds are a lot better when you know a company is swimming with the tide. I traded Webjet for years, knowing it was a bottom left to top right stock. Nothing quite like having the odds on your side.

What are 3 to 4 of your favourite stock screens?

- Return on equity. Think of it as how much the company makes a year out of a dollar. If return on equity is 30% then every time you hand them a dollar, they'll make 30% for you. It is so much more important than measures like yield. The best companies have a high return on equity and a yield of zero. If they can make 30% a year I don't want them giving it back to me so I can put it in bonds. Keep it.

- Performance. If you want a list of the best investments for next year, look at the best performers this year. Stocks don’t go down because they are cheap, they go down for a reason. Stocks don’t go up because they are expensive, they go up because people like them. The market is a natural filter for rubbish stocks. You don’t buy stocks just because they fell a lot and you don’t sell them because they double, or you’ll never hold a ten-bagger.

- PE and yield. But not how you think. Sort stocks by the highest PE and the lowest yield. The rockets under the rocks are right in front of you. It’s the opposite of what you expect and have been taught to believe.

- On a technical screen, RSI and MACD. You could choose 100 indicators but these two sit permanently on our charts because they are a couple of the simplest and the best. We don't follow them slavishly but they are good at highlighting trend change, and picking the pivot points is what timing is all about.

What are 2 to 3 simple things investors can do to their investment process to dramatically improve their performance?

- No joke: subscribe to Marcus Today and get an education. (Details of our special offer for Livewire subscribers is provided below). We have been building a community of better investors for 22 years. We do that through daily podcasts and emails, all of which inform and explain as well as entertain. You are welcome to join us.

- Get a good chart set up. Everyone needs a go-to chart set up, one with a couple of technical indicators on it that you understand. We have an education course telling you how to do that being launched later this year. But look at any of our charts and you will see our chart set up. It's pretty simple, but you need your own go-to charts and you have to understand the technical signals and know when to believe them and when to ignore them. You'll only do that with experience. There are some great software packages. Metastock is the old favourite, but we use Omnitrader (CorporateDoctor in Australia) and some of our Members use Bullcharts.

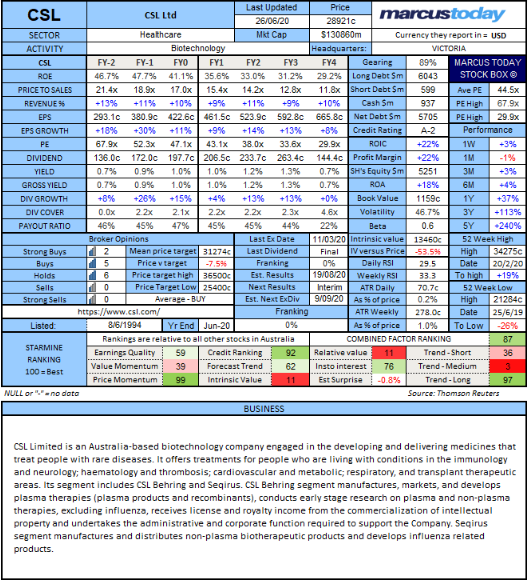

- Do the work. There is a baseline fundamental process you do on stocks, without which you are flying blind. You need to know what sort of animal you are dealing with. All stocks have different characters. We have a fabulous thing called a STOCK BOX that gives you a snapshot of a company and its fundamentals. Below is an example. You will notice that we have at least five years worth of historic and forecast numbers, that's so you can see the trend in things like company earnings and return on equity. It gives you so much more information than just quoting one PE or yield. You will also see in the STOCK BOX things like broker recommendations, target prices, intrinsic value and a host of other useful information that will give you a handle on value, on growth, on whether the price is thought to be too high or too low.

Click to enlarge image.

Where to from here for markets?

No one knows. We don't care. We are not in the game of making grand predictions. We are in the game of making money out of the market whenever the opportunity arises, and that could be any time. We just keep waking up in the morning and making decisions. It's working. We'll keep doing that. Telling you that we think the ASX 200 will be at 7000 by the end of the year is just an attention-grabbing joke. We laugh at that sort of prediction and despair for anyone that relies on these unmakeable predictions.

The problem with predictions is that some high profile finance commentators don't know they don't know, but still make the call. One broker called the bottom of the February Coronavirus correction after a week. I wanted to tell everybody not to listen but it's not allowed, and anyway, people making mistakes is good for those that haven’t. He must have taken a lot of retail investors back into the market. It wasn't just stupid, it was reckless. I saw the same thing in 2012 in December, one very high profile journalist writing for a stock market newsletter called the top of the market. He would have lost his followers a fortune. Forgotten now of course. That's the beauty of getting it wrong, no one remembers. Except me.

What are the key things you are watching that would make you cash up again become 100% invested?

We are in 100% cash at the moment and we did it because the US market dropped 6.9% in a night. That's not normal, that is the sort of move that marks a "Big Top" and starts a correction. Corrections start fast. At the same time 25% of the ASX 200 generated technical sell signals on their charts.

We had also made a 36% profit in less than three months. On that first day of the sell-off we were bleeding performance in the recovery stocks that had served us so well. It was time to lock in, which we did.

As far as getting 100% invested again, we'll take it day by day, stock by stock. We'll just keep waking up and making decisions. A sharp rise on the back of a vaccine (a real one this time) is about the only thing I can think of that would make us move very quickly at the moment. Otherwise, it is likely to be a gradual thing because it takes three times as long to build confidence as it does to destroy it. So you always have plenty of time to do your buying. It is the selling you've got to be quick with.

Lastly, I heard you have some amazing stories from your London broking days in the 80s. Can you tell a story about some lessons you learned which serve you well today?

Whilst in London my best man used to go fox-hunting (no emails) with the richest man in England. We had some hilarious nights out in London that included being chauffeured in and out of the West End, sitting at his private tables at London's top night clubs, and listening as he expounded his somewhat brutal assessment of life and business. I took notes. Here is the potted version. Do not try this at home.

- Think beyond the square. Set an unachievable goal. Shoot for the stars and hit the moon. Pictures of Porches on the fridge. All that sort of stuff.

- Starting with nothing is good. Who is the better competitor? Someone fat and comfortable or someone lean and hungry, someone driven, focused, bold and prepared to take risks?

- Debt is king. You'll never make big money without it. Do not be afraid of debt. Liabilities drive you to the most Herculean of efforts.

- Growing a business organically will only ever achieve incremental returns. Take the big steps and the little steps will look after themselves. There is more money made in a room in an hour than is made in a factory every day.

- Your business has to be scaleable. You cannot make exponential money without exponential growth. A pop star making an album is a scaleable business and why pop stars are rich. After 100 years in the game Morgan cars are still in the same factory and have a waiting list. They don't sell cars, they ration them. The business is not scaleable.

- Patience is not a virtue it's a waste of bloody time. Time is the most valuable of commodities and you will not succeed without it. No-one got rich working 9 to 5 and respecting weekends. You can't build a business 9 to 5. It takes total immersion. Every activity becomes a time versus money equation.

- There is no such thing as intelligence. What we mistake for smart or intelligent is actually just the expression of hard work and preparation. There is nothing you can do with brains that you can't achieve with application. What you don't know you learn. We all have the capacity to learn. Intelligence is impossible without hard work and possible with it. The difference is effort. Nothing comes without effort. From pop stars to the guy who invented the Rubik's cube, brilliance is 99% perspiration.

- There is no substitute for mistakes. Mistakes compress learning. A person not making mistakes is not learning.

- Education is paramount. The more you learn the more the lights come on and the more you realise how many other lights are off. You have to know, there is no substitute. Knowing opens doors. And knowing what you don't know is as important as knowing what you do.

- You cannot do everything yourself. Lucky then that the most valuable and available capital in the whole world is human capital, employees. The willingness of highly capable and educated people to work for a certain rather than variable sum is the most exploitable, available and cheap investment you will ever make. Invest in the markets and you concern yourself with returns of zero to 20% per annum and possibly even a loss. Invest in people and your return can be hundreds of percent. There is simply no better return on capital than capital "employed".

- There is education and there is qualification. Set out in pursuit of a qualification and you will deliver yourself to the corporate sector for exploitation. Set out for an education and you will develop beyond that. To take it to the extreme "why do exams". You already have everything you need. That piece of paper is of little use unless you want to impress someone else and build their assets instead of yours.

- We cannot employ the unchallenged. Twenty-five year olds are not supposed to be sitting in their parent's homes eating takeaway Pizza. The longer they stay on the financial umbilical cord the weaker they get. Feed the ducks and they will never learn to feed themselves. For their own sake, you have to release them to the wild. Kick them out. We cannot employ weaklings.

That's all I got. Things got a bit fuzzy and illegible sometimes. He always picked up the bill as well. Bargain. But is he happy…..you bet he is.

Special offer for Livewire subscribers

Take advantage of the EOFY Marcus Today membership offer as prices will increase from July. Click here to SUBSCRIBE using Promo Code EOFY20MT or sign up for a FREE TRIAL

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

5 topics

10 stocks mentioned

1 contributor mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment