What do low interest rates mean for equity markets?

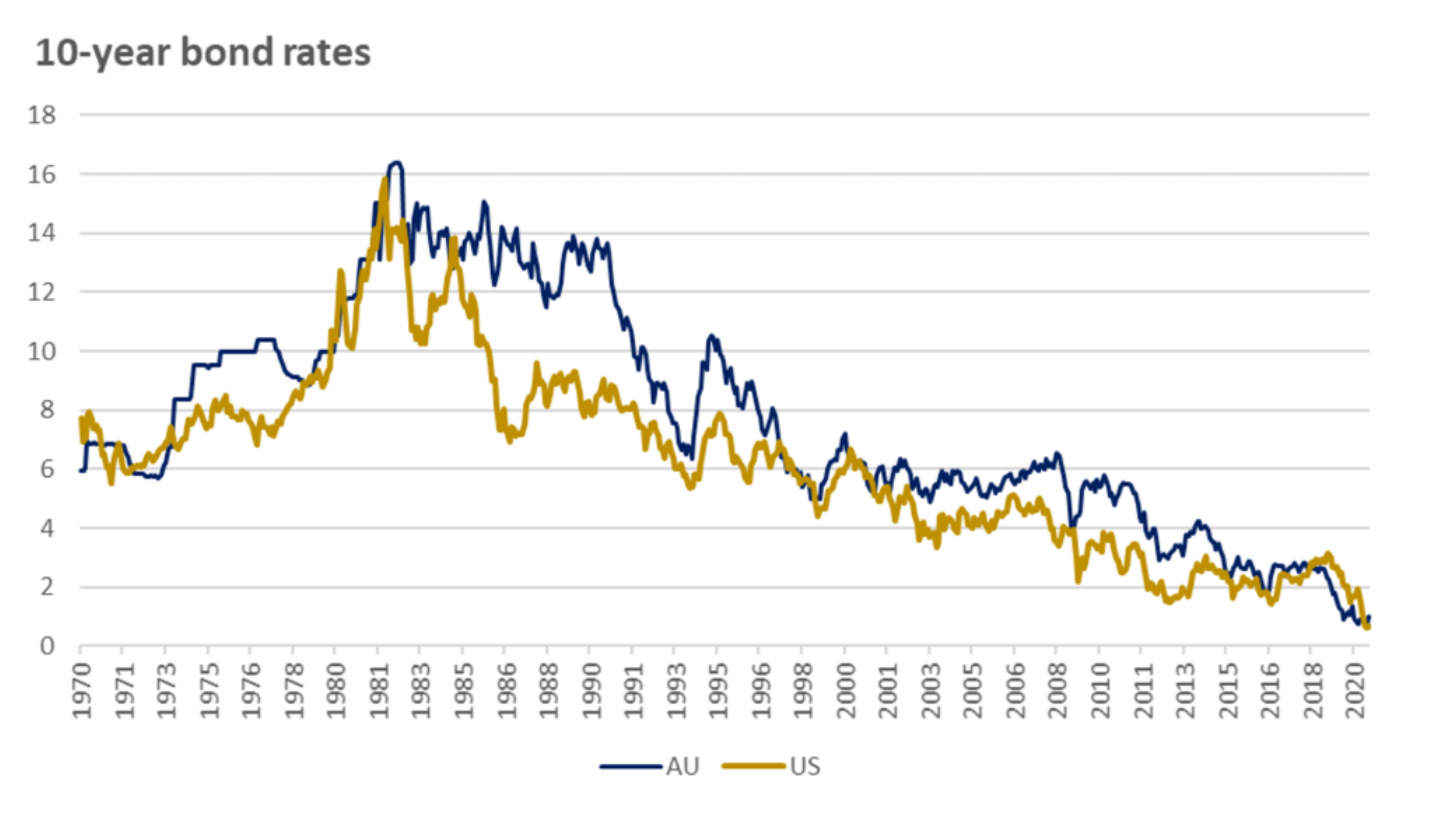

The last 30-40 years has seen a dramatic shift down in interest rates for much of the developed world. For example, the ten-year government bond yields in Australia and the US have declined from around 14 per cent in the early 80s to more recently lie somewhere not unadjacent to zero.

This relentless shift down in rates has naturally had profound implications for bond prices which are tied to rates by some straightforward math that requires the price of a bond to equal the coupon divided by the yield.

In the case of equities, it is tempting to think that a very similar dynamic should be at play. If you believe in capital asset pricing model (CAPM), for example, your starting point for calculating an equity discount rate is a long-term risk-free rate, and market practice has been to take the ten-year government bond rate as an estimate for the relevant risk-free rate. All else being equal, a lower ten-year government bond rate would flow directly into a lower equity discount rate and higher equity valuations.

But “all else being equal” is a big assumption, and something that warrants further thought.

One thing that needs to be considered is the role of inflation, which impacts bonds and equities differently. Due to the effects of inflation, we might expect each of the revenues, costs and (importantly), profits of a business to increase with it, such that inflation drives growth in (nominal) earnings for equities.

A typical ten-year government bond enjoys no such inflationary growth in its coupon, which tends to be fixed at the time of issue. This means that where interest rates change as a response to changing inflation, the valuation implications for equities and bonds can be different. This is an important point given that central banks typically use interest rates as a way of steering inflation – keeping rates low when inflation is low and pushing rates higher when inflation becomes uncomfortably high.

A consequence of this is that when interest rates are reduced in response to low levels of inflation, the nominal growth rate of equities will also tend to be lower. Compounding this, the economic environment that promotes low inflation tends to be one of weaker economic growth, so for equities, the expected valuation tailwind of low rates needs to be set against the potential valuation headwind of slower future growth.

Beyond inflation, there are other factors that might contribute to interest rates impacting equities differently to bonds. Some of these include:

- The idea behind the risk-free rate component of CAPM is that it is the return an investor would we willing to accept on a riskless investment. If long-term bond rates were to become divorced from investor preferences, for example by central banks pushing them to “artificially” low levels, this idea may no longer be valid.

- While a ten-year bond produces cashflows for exactly ten years, the timeframe for equity valuation is indefinite. If investors are concerned that long-term interest rates may change during that indefinite period, then long-term bond rates may not be such a good proxy for the risk-free rate. This would likely become more important as interest rates get lower and longer-dated cashflows become more important to valuation.

- In addition to the risk-free rate, an equity discount rate includes a risk premium to compensate investors for the risk of holding equities. The equity risk premium is a very difficult thing to measure directly, and it is not clear that it would remain constant when interest rates change. For example, if investor psychology was such that a minimum total return was required to invest in equities, declining interest rates would be offset by a larger risk premium.

Having said all that, it seems entirely reasonable to think that declining interest rates should put some upward pressure on equity valuations. For example, where the income that can be earned on “riskless” investments becomes unacceptable, there will be some impetus for investors to move towards riskier assets to find the necessary income, driving up their prices in the process.

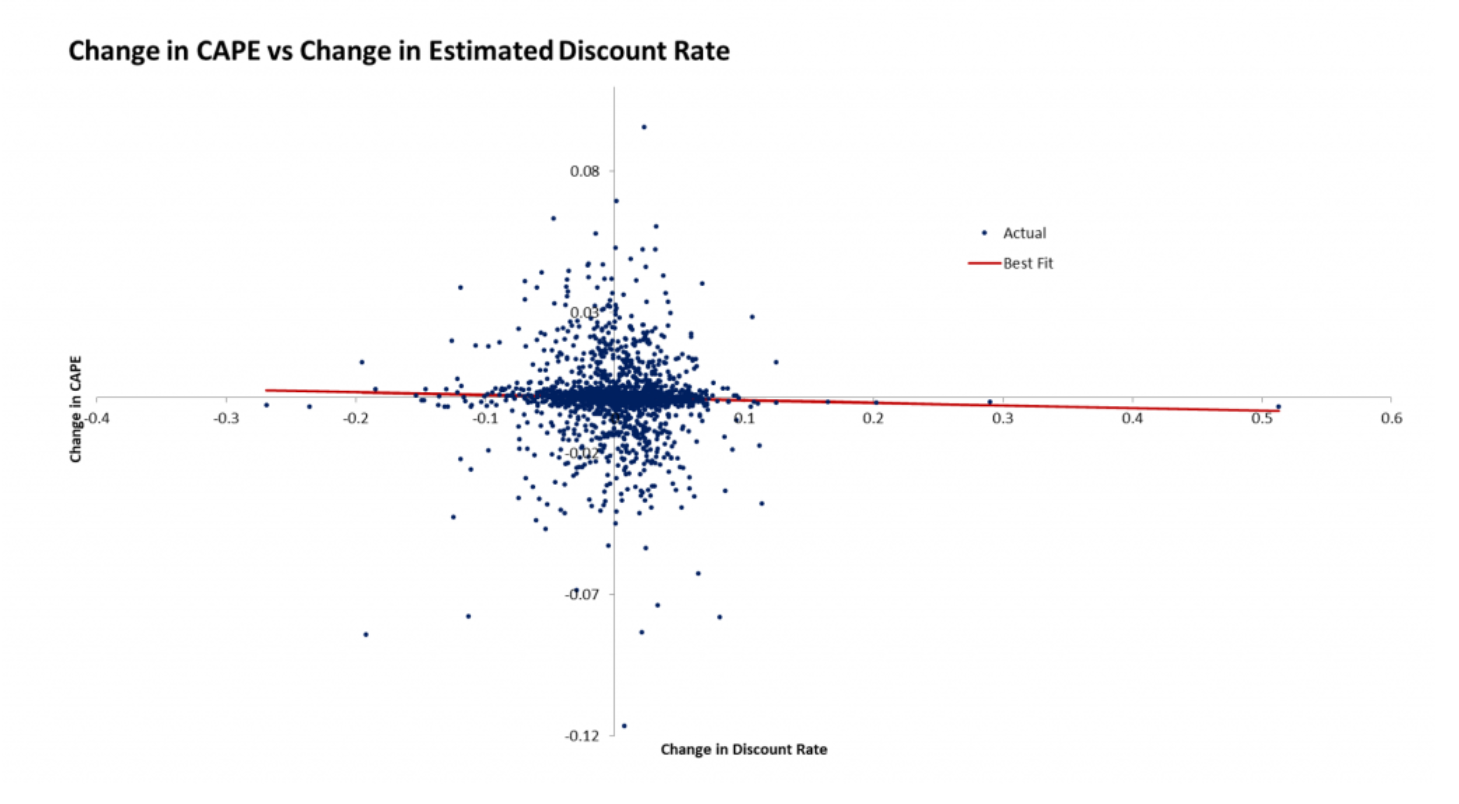

To better understand how these competing arguments might weigh up, we can look at the historical relationship between interest rates and equity valuations. One of the better sources of relevant data is Robert Shiller’s website, which includes among other things time series for 10-year US government bond rates and the Cyclically Adjusted Price Earnings Ratio (CAPE) stretching back as far as 1881.

To the extent that changes in interest rates justify changes to equity valuations, we should be able to see this by regressing monthly or yearly changes to CAPE against the corresponding monthly or yearly change to interest rates.

We make one slight adjustment to the data, which is to add a constant assumed equity risk premium of 6 per cent to the ten-year government bond rate to estimate the CAPM discount rate investors might apply in valuing the equity market. We then look at the relationship between proportionate changes to this estimated discount rate and proportionate changes to CAPE.

The results of this analysis are set out below using monthly data. As shown, we find virtually no relationship between changes to interest rates and changes to CAPE, suggesting that interest rates play a relatively minor role in setting the level of equity market valuations.

Source: Robert Shiller’s website; MIM analysis

We can try some variations on this analysis, including looking at annual rather than monthly intervals, looking at just the most recent 50 years rather than the full time series, and cleaning the data to reduce the effects of outliers. However, these variations all show a very similar picture to the one above – no clear relationship between interest rates and equity valuations.

This indicates, low interest rates do not provide a very sound basis for elevated equity prices, despite the apparent linkage through discount rates. This may reflect the inflation, growth and risk premium considerations outlined earlier, or possibly other explanations we have overlooked. In any event, history suggests that lower interest rates are not necessarily good news for equity investors.

An extension of this is that low interest rates may not provide a very sound basis for the stratospheric multiples currently attaching to some high growth companies in particular (in contrast to lower-growth, or “value” names).

At the end of the day, equity prices are driven by a wide range of factors related to growth prospects, risks and – importantly – investor sentiment. It is probably wise to consider all of these factors in thinking about your approach to the equity market, and while low interest rates might provide a strong incentive to move from safer investments into riskier ones like equities, this should be balanced against the very real risk of overpaying, especially for growth names trading at record multiples.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our investment process. Tim remains a shareholder of Montgomery Investment Management.

5 topics

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management