You better run, you better take cover

Brett Gillespie

Global Macro

September 27th, 1983. What comes to mind? What if I include the quote from Bob Hawke? “Any boss who sacks a worker for not turning up today is a bum”. If you are over 45, you will know straight away. It was the day the yacht Australia II won the 7th race of the America’s Cup challenge, and in doing so ended the longest winning streak in sporting history, some 132 years!

It was a nail biting series. In a best of 7 races, Australia lost the first two races due to “equipment failure”. Race 3 was abandoned as neither boat could complete the course in the time limit (no wind), but when the race restarted the following day Australia won by three minutes and 14 seconds. Hopes were high, then quickly deflated two days later when the US won race 4 and took a 3:1 lead. Australia would have to win the remaining 3 races to take the title. The Americans started race 5 in the lead, but then they suffered equipment failure. Australia took race 6, and the whole nation was up watching race 7 live in the early hours of the morning.

Australia II was subsequently overtaken by Conner who built up what seemed to be an unassailable margin. At the start of the penultimate leg (a square run) the America's Cup looked like it would stay in Newport. Conner failed to cover Australia II which allowed them to run deeper and faster assisted by breeze and windshifts allowing Australia II to overtake the Americans by the leeward mark. Conner then engaged Australia II in a spectacular tacking duel with nearly 50 tacks including a number of faked "dummy" tacks trying to break the Australians' cover. Australia II held on until both boats reached the starboard layline in amongst the spectator fleet and tacked several boat lengths ahead of Liberty and sailed to the finish to take the race. Australia II crossed the finish line with a winning margin of 41 seconds, becoming the first successful challenger in the 132 years "since the schooner America won it in a race around England's Isle of Wight in 1851”.

I’ve always loved sailing, having grown up with a Hobie cat, and a father owning (small) yachts and racing each week. And from time to time I still do a season or two of twilight racing. One of my favourite seasons was on John Balderstone’s “Jem”, a Sydney 47, racing out of Rushcutters bay on Monday night – the spinnaker race. The most exciting races were when a big afternoon southerly hit mid-race. With 25-35 knot gusting winds, and a 70 square metre spinnaker needing to go up and down 3 times in a race, some very handy work was required. Indeed, I was up front, with 3 others dragging the spinnaker in as we rounded a mark when a gust reflated the sail. I held on, as you do when trying to pull a sail down on a smaller boat, only to find myself been taken over the rail. Holding on to the sail for dear life, I was bobbed in and out of the water as it flapped in the gust, before two crew dragged me back in. “You’ve been tea bagged” , they said.

In many ways investing is like sailing. The weather changes, often without notice, and you need to be prepared – ready to reef the sails and batten down the hatches.

And so the weather changed in March. Indeed, we might say our portfolio was tea bagged. By tariffs. And Facebook. Having navigated February with tactical precision – let’s say we won race 3, we applied the same tactics for March. And the wind direction changed. Instead of rising bonds yields being the Achilles heel for the equity market, bond yields stabilised and tariffs (and Facebook) took us over the side rail and tea bagged us.

So what now?

The Outlook

Our core view is unchanged. The US economy is going to grow well above trend this year, the Fed is determined to get back to a more neutral cash rate (3% plus) in an orderly fashion, and there is a very real risk that a wage/inflation acceleration undermines confidence in the Fed and causes the market to fear a hard landing (recession) .

It just may not play out this quarter.

March was always going to be a pivotal month for bonds, given the alarmingly high wage and inflation prints the prior month. Would data confirm the start of a trend, or just a bit of noise? If there was another high print in wages or inflation, the market was ready to declare a trend and march 10 year yields through 3%, in turn panicking the equity market. In addition, a hawkish Fed could be expected to add to momentum. Although forecasting any one month is perilous, we were willing to spend premium on short dated options for that scenario. As it transpired, both the wages and inflation print were benign. The chart below shows the expectation for the US wage print each month v the actual. And below that the gap. The market got very nervous in February when wages came in 0.3 higher than expected. Another upside surprise in March would have suggested the wages trend was accelerating. Albeit, we had a sharp downside surprise. It will now likely take several high readings on wages/inflation to confirm a trend and panic the bond market through 3%.

The other catalyst for higher yields we were focussed on also faded a little in March. If you recall, we have written about the cessation of global central bank purchases of bonds seeing the risk premium restored to global 10 year yields. But recent European data has being slowing, and the ECB is sounding more dovish again.

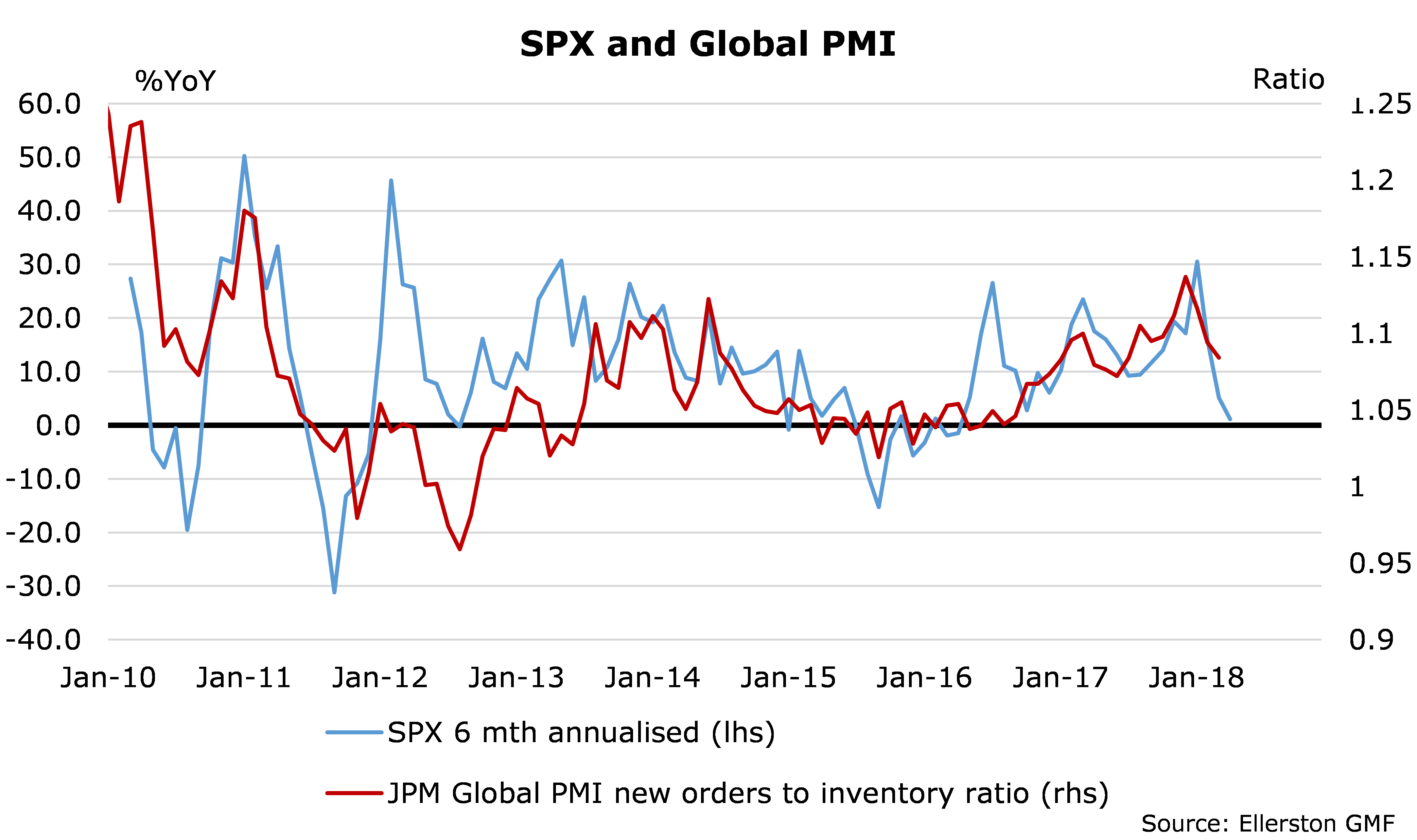

Indeed, the roll-over in global PMI’s suggests a near term peak in US yields.

And flat returns for the US stock market over the next 6 months.

In fact, a lot of the lead indicators our economist Tim Toohey constructs show a slowing of growth, particularly outside the US.

And our financial conditions indices (FCI) suggest this trend is going to continue. Only US conditions have eased over the last year. Everyone else, although “easy”, have remained the same or become less easy.

Why the divergence between the US and other countries? Well, the FCI’s measure how supportive “conditions” are that support the economy. The calculation includes interest rates, long term interest rates, interest rates for corporates, the effect of equity prices (wealth), and the currency. (And for some countries, commodity prices.) The key difference between countries at the moment is the US equity market over the last year is still up some 15% v flat to down for most other countries, and the USD has weakened v all the major currencies, meaning all the other countries are losing competitiveness to the US.

So that is the big picture macro backdrop. US growth will stay firm, thanks to supportive financial conditions (and tax cuts). But growth elsewhere is set to moderate slightly. Still solidly above trend, but slightly softer. That changes the global image from one of synchronised growth acceleration, to one of moderately strong growth but with the US clearly out-performing.

That in turn suggests US equities will out-perform the rest of the world, and that the USD will do the same. If it should find a bottom here.

Interestingly, an increase in tariffs (protectionism) should also lead to a stronger USD, supporting the theme in the chart above.

All reasonably straight forward. Until the southerly hit. The one/two of Facebook and tariffs.

So what about Facebook and the like? Is their business model mortally wounded? Won’t that crash US equities? There are a lot of people with a much better handle on this than myself, but listening to Hamish Douglas of Magellan last week, his view seemed reasonable –

expect volatility and adjustments, but long term Facebook will continue to do extremely well.

And won’t everyone lose with tariffs? Won’t common sense prevail? Where will the tit for tat end? As I write it is escalating, not moderating.

Indeed, Trump will not relent until he gets real concessions here. China (and India) have been dragging the chain on tariff reductions

Source: Morgan Stanley

But the deficit is with China

Source: Morgan Stanley

Source: Morgan Stanley

Are the tariffs so far material? No. If the 50b of US tariffs initially announced are fully imposed, the estimated hit to Chinese growth circa 0.15%. But now Trump is threatening another 100b. That is clearly alarming.

How bad can it get? Theoretically, if the US banned all imports from China, the hit to Chinese growth would be 1.3%. If China banned all direct and indirect imports from the US, US growth would slow by 0.9%. With reverberations, enough to possibly tip the world into recession.

But of course it won’t continue to escalate. Will it? Well, for sure we are going to have more brinkmanship. It is Trump’s modus operandi, as we have seen with NAFTA. But for Trump it is a negotiation, and he starts aggressive. So the market expects him to settle for realistic goals – in time.

And the Chinese? They initially made soothing sounds;

- China’s Vice Premier Liu warns Mnuchin in a call that China will defend its own trade interests, but hopes both sides will remain ‘rational’ and work together to keep relations stable (Xinhua/Reuters);

- China’s Vice Commerce Minister says China is considering ending some restrictions on foreign stakes (Reuters) and China’s new Central Bank Governor Yi Gang pledges steady opening of the finance sector (Reuters).

- Finally, an FT piece on how Chinese officials are confident that carefully calibrated responses to US tariffs can help avoid a bigger crisis in Sino-US relations as it eyes more important long-term strategic aims, also confident they can reduce the $375bn surplus in manufactured goods, and announce market opening measures, within 6 months to allow President Trump to claim victory before November’s mid-terms.

But make no mistake. China will also do their share of brinkmanship. Indeed, in response to Trump’s latest announcement of an extra 100b, they don’t sound so soothing;

· "We will not start a war -- however, if someone starts a war, we will definitely fight back," Gao Feng, the commerce ministry spokesman, said at a news conference in Beijing on Friday. "No options will be ruled out."

Mmm, what will those options look like? A couple of weeks ago Mei Xinyu, from China’s equivalent of Treasury, gave a speech identifying what options China has. They could

- target tariffs at the US states that helped Trump to victory (done);

- they could sell their US treasuries, forcing yields higher and undermining the US stock market (they have already stopped buying);

- Or they could stop co-operating with the US (with regard to say North Korea).

So what is going to happen? It is obviously hard to say. But I do know this. China’s $1.17 trillion holding of US treasuries in the 800 ton gorilla in the room. Last year they purchased $126.5 billion in Treasuries. This year they appear to have purchased none. What if they sell? What if they suggest selling? What if Trump thinks he can come up with some way to stop them selling? How would the Japanese feel about their $1.06 trillion holding? Tariffs are a problem. But if the fight turns to treasuries, we are just starting the volatility ride.

So what does one do?

First we focus on what we can forecast. We still believe the US economy will be strong. Indeed, the risk is that we get an outbreak in wages and/or inflation. The Fed needs to hike consistently back to 3.5%, they know it, and they are more determined than most realise. We are similarly determined to weather the storm and monetise that outlook.

And we take precautions. We are starting April with a reefed main and no genoa. Tariff concern will escalate and release, upsetting the markets for some months. In addition, some of the tech stocks will be rocky for a time, but again likely settle. We cannot predict the week to week tariff fear, or the bottom in some tech stocks. But we can forecast the growth outlook, and adjust for the actual consequences of tariffs and equity market weakness. As of now that is not material. What would make it material? A sharp fall in the equity market. So that is what we need to hedge.

So we have reduced risk and simplified our portfolio. Our main exposure to the Fed hiking is in the option market, where we will benefit if there is an increased expectation of rate hikes in the US in 2019. In March the market moved towards pricing 2 rate hikes after the employment numbers, before shaving expectations to just over one hike with the late month equity swoon. We expect US expectations for hikes in 2019 will move towards 3 to 4 as we move through the year. We have this trade in both futures and 6 month options, the latter to sustain the view.

But if tariffs escalate significantly, or there was a much larger fall in tech stocks, that will significantly dent US growth and likely derail the Fed. Indeed, we think the strong US growth is so locked in now that the only thing that will derail it is an equity market crash. And what is the best way to hedge against an equity crash? Puts on the US stock market? In this volatility, that is very expensive. We look for cheaper protection. AUD/YEN is highly correlated to equities in risk off episodes. And the option market there provides very “cheap” insurance. So we like short AUD/YEN in options to provide returns for the portfolio if the southerly turns into a cyclone.

We have exotic options targeting AUDJPY to trade into the 74-79 range over the next two months. Expiry at say 76 would reward 16x the premium at risk. Our correlation analysis suggests that would equate to US equities being about 8% weaker. A similar option trade on the SP would return at best 7:1. We have a little of that too (in case the correlation is not ideal), but less given the risk reward.

And Australia?

At the moment it is cruising along quite nicely. Our indicators still suggest a move back to 3% growth, a fall in the unemployment rate and hence a rate hike this year, most likely November. If anything, a minor tariff spat between China and the US will benefit Australian exporters. As long as it doesn’t get so big as to slow Chinese/US growth…We are still positioned for a November rate hike in the portfolio. But at this stage the exposure is modest. We have time to see our forecast of falling unemployment commence before building this exposure.

About the Ellerston Global Macro Fund

The Ellerston Global Macro Fund is an absolute, unconstrained strategy investing in a number of fundamentally derived core themes, optimised via trade expression and portfolio construction across Fixed Income, Foreign Exchange, Equity & Commodities. It focuses on capital preservation while providing low to negative correlation to traditional asset classes. Find out more

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Brett has worked in the financial services industry for over 28 years. Most recently he was Head of Global Macro at Ellerston Capital. Prior to that he spent over 10 years as Senior Portfolio Manager at Tudor Investment Corporation.

6 topics

Brett Gillespie

Investor

Global Macro

Brett has worked in the financial services industry for over 28 years. Most recently he was Head of Global Macro at Ellerston Capital. Prior to that he spent over 10 years as Senior Portfolio Manager at Tudor Investment Corporation.

Expertise

Brett Gillespie

Investor

Global Macro

Brett has worked in the financial services industry for over 28 years. Most recently he was Head of Global Macro at Ellerston Capital. Prior to that he spent over 10 years as Senior Portfolio Manager at Tudor Investment Corporation.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets