5 reasons housing prices to keep falling

Tim Hannon

Conrad Capital Group

The current 25-year credit cycle has seen Australian household leverage rates move to record levels versus all other developed markets. This degree of leverage is unprecedented in Australian history and is often a precursor to a major housing correction.

We have had significant concerns about the sustainability of the credit-driven boom of the Australian residential market, which we set out in a report published on Livewire in 2016.

High leverage is not enough to cause a housing correction. It also requires credit growth to flatten out and turn negative, and we think we are seeing the early signs of this.

Our negative view is coming from our current observations of tightening credit conditions in Australia, coupled with a moderation in buyer demand as house prices have started to soften.

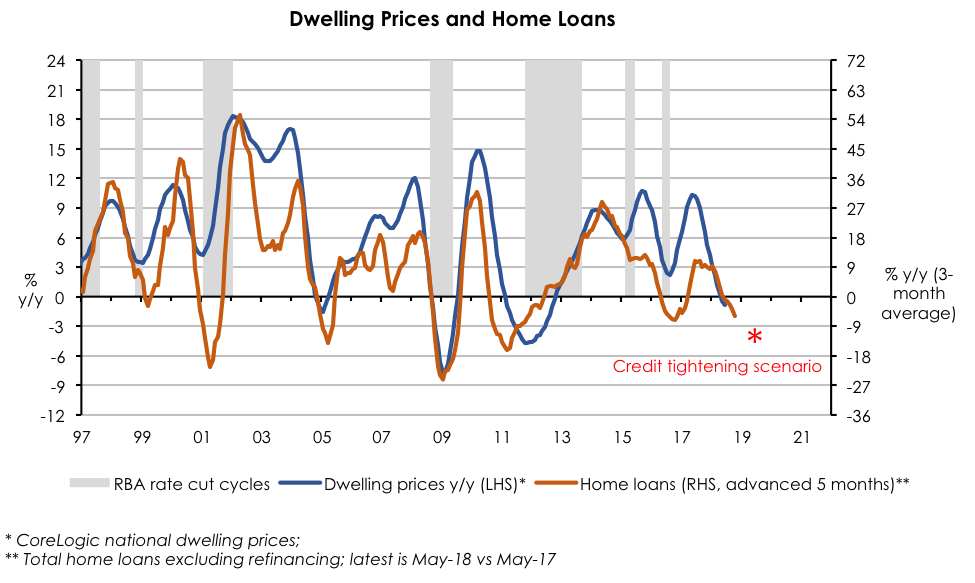

The chart below shows the close correlation of credit growth and growth. Credit drives housing prices…

Five reasons we believe credit growth will continue to slow

Our view is future credit growth will continue to slow because banks have tightened lending standards in response to the recent Royal Commission. Very simply, it is more difficult for borrowers to get a loan. Here are five reasons we expect credit growth to keep slowing.

1. More rigorous assessment of borrower expenses

Banks will start to use more realistic expense standards in assessing new loans – they have not been doing this previously. The average household spends around $75k per annum, but banks have been using $32-35k for over 75% of borrowers. Once banks adjust to factor in higher living expenses, they will not be able to lend as much.

We estimate a drop in borrowing capacity of 10-20%, with a risk of larger declines if banks start to verify actual household expenses for a large portion of borrowers.

2. Setting maximum borrowing levels versus income

The bank regulator, APRA, has directed banks to implement limits on the proportion of new lending at “very high debt-to-income” (DTI) levels of greater than six times (>6x).

While APRA indicated it will allow the banks to set these limits based on their own risk assessment and judgement, APRA’s description of >6x DTI as “very high” suggests APRA is over time targeting a material reduction in the proportion of new lending at high debt-to-income levels.

The Household Income and Labour Dynamics in Australia (HILDA) survey suggests that a staggering 1/3 of loans (by $ value) have been made at a level that exceeds six times income.

If APRA’s debt-to-income directive was to reduce new loans with >6x DTI to 10-15% of new lending, this would represent a material reduction in credit availability.

This is particularly so when it is considered that the two largest housing markets trade at a median house price to income of nine times in Sydney and eight times in Melbourne.

This means theoretically there is little debt capacity to purchase the circa $1 million median house price in Sydney or Melbourne for households on the average income.

3. Including all household liabilities

Banks have not necessarily included all liabilities of households when determining their ability to service debt, as banks have been reliant on borrowers to disclose their pre‑existing debt levels.

Comprehensive credit reporting is now being introduced that will see banks gain access to loan applicants’ pre-existing debt profiles across all Australian banks, and thus will no longer need to rely on borrower disclosure. This means banks will soon be able to take into consideration applicants’ pre-existing debt levels for all new loan applications.

It is difficult to estimate the negative borrowing capacity impact.

4. Ability to service existing loans - interest-only cap

Interest-only loans reached close to 40% of banks’ total mortgage balances, which is now in decline after APRA’s 30% cap on interest-only loans (as a % of flow) since the September quarter 2017.

The 30% interest-only cap means a significant number of interest-only loans will be forced to convert to principal & interest (P&I) once interest-only periods mature (typically 5‑years). Interest-only loans converted to P&I see monthly loan repayments increase by 30‑50%.

5. Chinese demand is falling

Foreign, and mostly Chinese demand has represented at least 20% of new housing purchases, and it is not known what percentage of established housing.

It is becoming increasingly difficult to get capital out of China after recent authority crackdowns.

Australia has also made it harder, by increasing stamp duty on foreign buyers and bank lending restrictions for applicants residing outside of Australia.

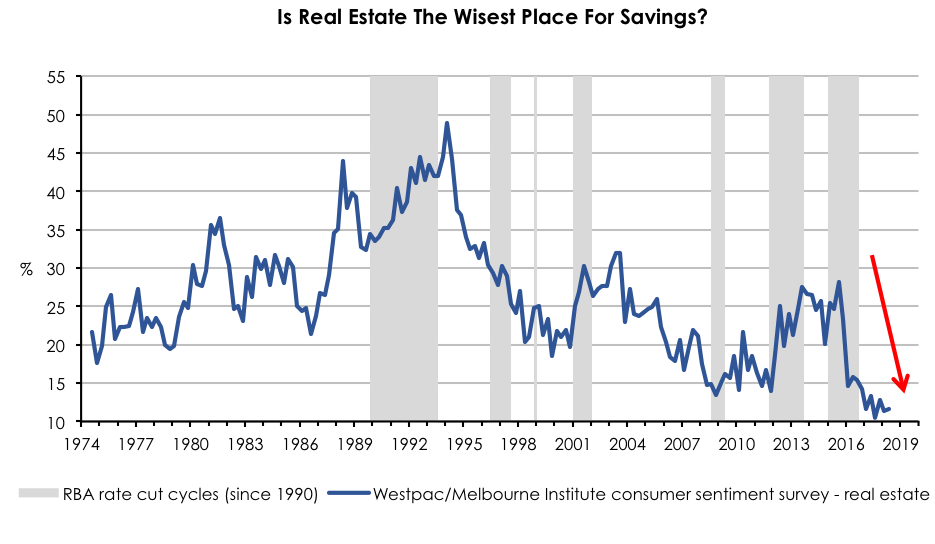

Willingness to borrow is at an all-time low

In addition to tightening credit standards, sentiment towards residential real estate indicates that borrowers are also less willing to enter the market.

How are we positioned?

It is most likely that borrowers will do anything to keep their property and will cut spending on most categories ahead of not meeting loan repayments.

We assess the impact from tighter credit conditions are yet to be felt. The first impacts will be felt amongst construction companies, residential developers and retailers.

In anticipation of a slowing credit cycle, we are short a select basket of exposed companies across these sectors.

The banks will likely feel the hit later as broader consumer and employment shocks kick-start the impairment cycle. That won't stop them from de-rating in the interim on slowing revenue growth, rising costs and increasing regulatory risk.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim has 25 years’ experience in the investment and securities markets. Tim was a partner of Goldman Sachs and during his 16-year tenure at the firm had senior experience across all areas of equities investing.

5 topics

Tim Hannon

Managing Director

Conrad Capital Group

Tim has 25 years’ experience in the investment and securities markets. Tim was a partner of Goldman Sachs and during his 16-year tenure at the firm had senior experience across all areas of equities investing.

Expertise

Tim Hannon

Managing Director

Conrad Capital Group

Tim has 25 years’ experience in the investment and securities markets. Tim was a partner of Goldman Sachs and during his 16-year tenure at the firm had senior experience across all areas of equities investing.

Expertise

Comments

Comments

Sign In or Join Free to comment