May Market Commentary

Another month of small gains in equities and credit, whilst commodities continued to fall back. Equities were up in Japan (2.4%), China (1.5%) and the US (1.2%) with Europe pretty much flat (-0.1%). Australian equities (-3.4%) were the standout loser. High yield and investment grade credit in the US and Europe also posted small gains. In commodities, iron ore (-17.2%) led the falls for a third month in a row. US natural gas (-6.1%) also took damage, with smaller falls for US oil (-1.7%) and copper (-1.2%) as gold (0.0%) remained unchanged.

Economic data tended to be weak in May, with macro indicators from Morgan Stanley and Citibank both showing notable drop offs. In recent months, soft data had been strong whilst hard data was subpar, but the gap has closed with soft data falling off. Even though lending standards are weak US corporate and consumer demand for debt has also dropped. Investor sentiment surveys are mostly optimistic though investors could be suffering from fear of missing out. The big positive data point was US federal tax collections, which have jumped this year.

Several big names have weighed in on valuations and sentiment. Nassim Taleb sees tail risk worse than 2007. Ray Dalio thinks the short term looks good, but the long term looks scary. Bill Gross says investors should short US high yield debt. Howard Marks is a little more sanguine calling credit rich but not in a bubble. Jim Rickards called China the biggest Ponzi scheme in history but Jim O’Neill says fears of a China crisis are completely overblown.

The bitcoin price has powered past $2,000 after being below $1,000 as recently as March. This has led to plenty of articles suggesting that Bitcoin looks like a bubble. Jefferey Gundlach asked whether it is a coincidence that Bitcoin is doing so well when Chinese equities and the currency are down. Others think a surge of Japanese buyers could be the reason. Other alternative currencies have also been on a tear, Bitcoin is just the largest of over 800.

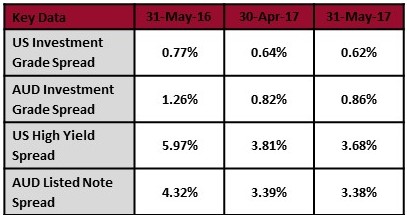

Various types of debt are showing bubble like signs, particularly European long duration and high yield debt. With negative overnight rates European investors are forced to go long or go below investment grade or end up going backwards after inflation. High yield bonds are now yielding less than 3%, leaving less than 1% of yield to cover defaults after accounting for inflation. The yield is even less than equities. Very long duration sovereign debt is back in favour now that the French election has passed, the recent French 30 year issue priced at 2% and was four times oversubscribed. Fitch has noted low spreads, high leverage and loose covenants are great for debt issuers but looks like 2007 all over again.

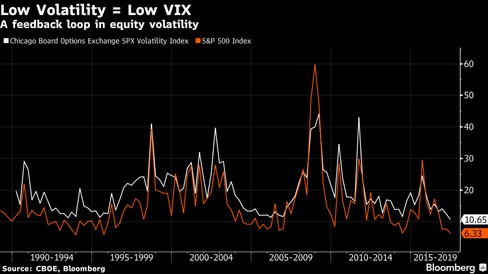

The lack of volatility has attracted a lot of interest and articles. The key focus is on the volatility index, often referred to as the VIX or fear index. The VIX is based on the cost of purchasing short dated options on the S&P 500, with a low reading meaning the cost of buying options is cheap. But low volatility wasn’t just limited to the VIX, bond volatility and most other asset classes are low too.

There’s a host of reasons why the VIX has been low. The short answer is that expected volatility (the cost of purchasing options) is low because realised (actual) volatility has been lower. Think of this in basic economic terms, if the cost of the inputs goes down then the cost the finished product in an open market will also go down. The graph below shows that the gap between the realised and expected volatility tends to move together quite well so the market has responded quite normally. Lurking behind the low realised volatility is a more interesting story that no one can definitively confirm.

Probably the best explanation for the recent low volatility came from Deutsche; they’ve posited that hedging by banks is reducing volatility in individual stocks and indices. However, they warned that the complexity of this hedging means that when VIX pops higher it can quickly snowball. There’s shades of the LTCM meltdown in this, once one person becomes a forced seller, others sell, either to race for the exit ahead of others or due to their leveraged positions. Others think that retail option sellers might be impacting the market, but they are more likely to impact expected volatility rather than realised volatility. Exchange traded products have also been put forward as subduing volatility.

Regardless of why volatility has been low the implications are worth considering. Selling volatility (selling options) has been a hugely profitable strategy over the long term. But it’s not for the faint hearted as there’s long periods of great returns and short periods of awful returns. Buying options, without a near term catalyst, is a ticket to the poorhouse. This makes sense when you consider that options are a form of insurance, and those who sell insurance expect to earn a decent margin for taking on the risk.

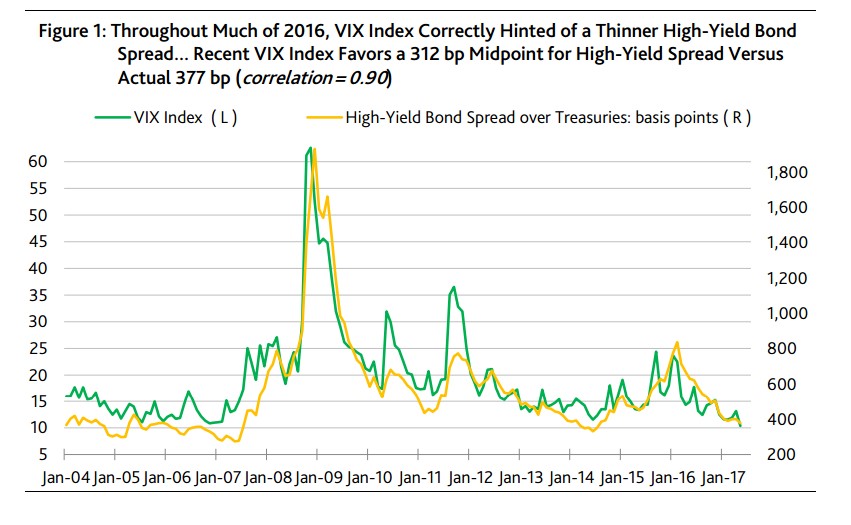

There’s a tendency to think that because the VIX is low the market is overly optimistic and equities are due for a fall. History doesn’t agree with this theory. However, for high yield the story is very different. The graph below shows a very strong correlation between the VIX and high yield spreads. If you consider that debt securities are also like insurance in that you get paid a premium for the credit risk then it is not surprising that these two types of insurance move together. I wouldn’t take the low VIX as a definitive indicator for high yield debt; the chart below indicates investors should be buying high yield debt. Many other indicators point to US and European high yield debt currently being an unattractive investment.

Source: (VIEW LINK)

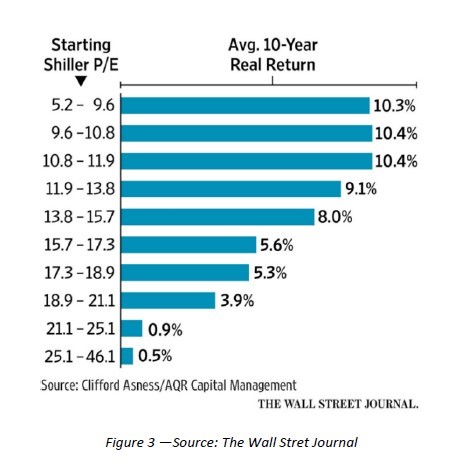

Unlike VIX, paying high prices for equities is a very strong lead indicator for future returns. I’m repeating this point pretty much every month now, but it is the point most often missing from the discussion of current high asset prices. The graph below is another great way of visualising the impact of paying too much now on your future returns. The higher the P/E ratio at the time of purchase, the lower the long term return.

If you want to disagree with that sort of data you need a pretty good “this time is different” argument. This Bloomberg article puts forward six reasons why investors should ignore these elevated ratios. I do give some credit to the argument that very low interest rates and quantitative easing could be here for a long time yet. The Japanisation of the US and European economies was something that many laughed at in 2009 but have more recently come around to. There’s also the risk that excessive money printing creates hyperinflation and investors therefore need to be in assets that have the ability to float higher with that.

Whilst almost everyone is talking about asset prices being high, only a few are taking meaningful action to protect against a potential correction. The most common actions are to increase cash positions a little or switch to lower risk assets. However, the decision by Altair Asset Management to temporarily close its equity funds and give back capital to investors is an all in bet that Australian equities will go lower. Altair’s CIO cited highly leveraged property, Chinese debt issues, overvalued Australian equities and geopolitical risks as reasons to hand back cash to investors. It’s attracted a lot of publicity and if the timing is roughly right it could pay off many times over for Altair and its clients.

Contrast this with the prevailing attitude in US high yield debt, where managers acknowledge high prices but are more worried about being unable to reinvest capital in a seller’s market than the possibility of material capital losses. Australian credit remains something of an island, where good value still remains. With a view that asset prices could be much cheaper in the medium term, my portfolios are now full of credits that shadow rate to investment grade with credit duration of around two years. Despite these conservative risk metrics, I’m continuing to deliver a net yield above that of US high yield for clients.

Australian Budget

The general opinion of the 2017/18 budget is that it is a politically savvy but economically boring budget. It’s easy to agree with this on a superficial level, but dig a little deeper and there’s a lot more colour to it.

Firstly, on the political side it has been called a Labor light budget in that it adopts some of the higher spending and higher taxing ways of the opposition Labor party. The ruling Liberal/National coalition has given up the fight for its core values of lower taxation, less waste and getting people to be less reliant upon government services. In shifting to the left to neutralise Labor, the coalition is leaving the right of politics wide open to the newly created Australian Conservatives, the Liberal Democrats and One Nation. If these parties can get their act together they will steal a stack of senate seats at the next election.

On the economic side the little noticed measures to stop healthy, working age people who can’t be bothered to work claiming welfare is great policy. It brings to mind the old Benjamin Franklin quote “I am for doing good for the poor, but I differ in opinion about the means. I think the best way of doing good to the poor is not making them easy in poverty, but leading or driving them out of it.”

When we are importing people to work in our fields, our tourist operations, our offices and food service outlets whilst over a million Australians are unemployed or underemployed there is clearly a willingness to work issue, not just a lack of jobs. The proposed measures draw from the successful New Zealand policies of the last decade, which are also finding favour with the Trump administration. I’m also strongly supportive of the efforts to crackdown on the black economy, which the taskforce head has estimated to be at least $35 billion per annum.

The biggest shortfall of the budget is that completely fails to take meaningful action to get back to a surplus. The plan for a balanced budget in four years (note this is well after another federal election and therefore a problem for another government) relies on ridiculous assumptions for inflation and employment growth. The old Keynesian principle of surpluses in the good times and deficits in the bad times has been discarded for deficits all the time. The major parties have given up on living within their means, unwilling to tell the population that we cannot have everything we want. At a federal level, we have given up on following the prudent examples of John Key (New Zealand) and Mike Baird (NSW), and have chosen the road to poverty that the US, Europe and Japan are taking.

The slow strangulation of higher taxes is ignored by many economists and politicians but it remains true. I’m not an advocate of Australia competing with Singapore and Ireland for the lowest corporate taxes in the world as that is a game we cannot win. However, Australia could compete in having lower tax rates for workers by shifting the tax burden to GST and land tax. Our migration should be focussed on very high skill workers and wealthy people, who will pay disproportionately high levels of taxation. By having a strong base of skilled workers, we can attract more of the new economy companies that will be driving future growth. The prize is not so much gaining corporate taxation from these companies, though targeted measures can capture more of their revenues. It is increasing the employment rates and income of Australians, thus increasing total taxes collected and lowering welfare spending.

China

The biggest news of the month for China was the downgrade by Moody’s of the country credit rating from Aa1 to A3. Whilst the first downgrade since 1989 came as a surprise to many, the massive growth in debt, lack of transparency in financial matters and the potential for bank bailouts means China should be rated much lower than A3. However, in saying this I’ve firmly of the view that almost all country ratings are inflated so I’m not singling out China on this. The aggressive Chinese response to the downgrade also isn’t unusual, countries and companies have long bad mouthed rating agencies after downgrades occurred. Rating agencies are transparent in their methodologies, typically outlining what needs to be done well in advance of downgrades. When borrowers fail to take corrective action they only have themselves to blame.

All of the above hasn’t stopped Bloomberg and Citigroup from taking steps to add Chinese bonds to their bond indices. I see four issues with this:

The quality of financial information is poor with fraud commonplace

Limited rating agency coverage, with the Chinese rating agencies notoriously optimistic in their assessments

Resolution of defaults is a very grey area. The legal system isn’t transparent or independent with corruption considered endemic, particularly against foreigners. Bailouts from local, state and the national governments are common when locals are the investors, but foreigners can be left with losses.

Trading rarely or never occurs on the majority of bonds, making valuations questionable and trading difficult.

These issues are common for emerging market countries, just part of the risk taken for the higher yield. Relative to other emerging markets though China’s debt offers very low returns. This is in large part due to the massive amount of capital trapped in the country by the exchange rate regime. As China’s bond market offers international investors relatively lower returns for high risk, there’s little reason for active investors to take the gamble. For passive investors, they look set to be stuck with poor value bonds being pushed into their portfolios. This is just another reason that passive investing for bonds is suboptimal.

After many false starts, reform of the financial system could be the real deal this time around as President Xi has given the orders. Credit growth in April was still strong, but wealth management products and entrusted loans saw a substantial drop in issuance. A life insurer banned from issuing new products has claimed there will be mass defaults and social unrest if it can’t start selling investment products again.

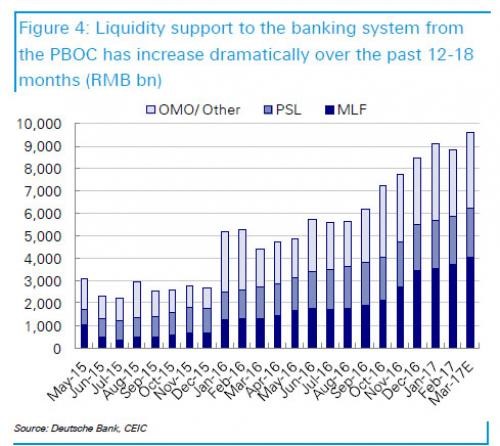

Regulators have cut off access to offshore bond markets for property developers and are insisting that collateral must exist and be saleable otherwise banks cannot lend. Research from the central bank called out moral hazard noting that no banks have collapsed even though some should have. The markets are pricing in this risk as interbank funding is now more expensive than corporate borrowing. This has occurred even with the huge expansion in central bank provided liquidity shown in the graph below.

The war on debt (as small as it has been) has led to higher bond yields, lower stock prices, more defaults and bond issues being cancelled. If fully implemented, this could have spill over impacts for global growth, particularly Canada and Australia. China has also seen a drop-off in its productivity growth which is another headwind for its GDP. The one belt, one road initiatives are supposed to provide new sources of growth for China. The risks are high when there is lots of debt, questionable viability and unstable countries involved.

Emerging Markets

Greece finally cut deal with its creditors that involves €4.9 billion of pension cuts and tax increases. This kicked off a huge rally in Greek debt and equities which makes them amongst the best performing assets this year. Sovereign debt yields have dropped low enough that some think another public issuance could be done. The 2014 issue traded as low as 40% of face value, but there just might be a few fools who get suckered in by the potential yield.

The IMF continues to argue the obvious that Greece needs a debt haircut, but some European institutions think Greece could deliver 20 years of big surpluses that will reduce debt levels. The constant debt maturities mean that Greece will have its feet to the fire for a long time yet. Greece has denied rumours that it could default in July this year, but that denial was based on a debt relief being granted in June which seems unlikely.

Puerto Rico is now in bankruptcy with the judge appointed cautioning that this will take years to fix. It’s very early stages for estimating recoveries but applying Detroit’s metrics to Puerto Rico implies an average recovery rate of 31%. Those expecting higher recovery rates are being optimistic on what a judge and the territory’s government can deliver when ordinary Puerto Ricans are already making sacrifices. Those looking to assign blame may focus on the tax exemption on municipal debt that made debt issuance much cheaper and allowed wasteful government spending to continue for years. Puerto Rico is being considered a precedent for future state bankruptcies. The financial troubles of the US Virgin Islands mean it may soon be following in footsteps of Puerto Rico.

Azerbaijan’s largest bank has halted payments on foreign debts, proposing haircuts of 20% on senior debt and 50% on subordinated debt. Brazil looked to be getting better, then another political crisis struck. Stocks were heavily sold off, serving as a reminder why emerging markets trade at a discount to developed markets. The underperformance of emerging markets relative to US markets in the last few years has Jeffrey Gundlach recommending a short position in the S&P 500 and long position in emerging market equities.

The end looks close for Venezuela. It’s primary export earner is oil, but oil production is dropping due to lack of maintenance on production and refining facilities. Security is getting ever worse with members of the army defecting. Goldman Sachs bought debt at 31% of face value from the government, half the level where similar bonds are trading.

Banking Bad

Monte Dei Paschi has fallen off the radar, but its problems remain unresolved. The proposal to take a government bailout has stalled as the ECB isn’t convinced the bank will be solvent after the proposed recapitalisation. The bailout cheque may need to be a lot bigger. The ECB is planning to introduce a total debt limit on leveraged loans of six times debt to adjusted EBITDA for European banks, similar to what the US has already done. Santander has been outed for verifying income on only 8% of its subprime auto loans. Deutsche Bank is looking to clawback compensation paid to board members who presided over its awful performance in the last decade.

Media Worth Consuming

Obama calls Trump a “bull****er”; he should know as he told his fair share of lies too. Trump’s budget is full of accounting gimmicks, spending cuts that are unlikely to pass and optimistic growth assumptions. Only Fox News and the Wall Street Journal are giving something like a balanced view of the Trump administration. American journalists were found to be dumber than average with excessive alcohol and coffee consumption blamed.

For those who love a good conspiracy theory, a murdered democrat has been named as the leaker of the Hillary files. Maybe Trump was right to propose the travel ban for troublesome countries; refugees are disproportionately involved in terrorism. Democrats can’t criticise Trump for sacking Comey; they had been calling for him to resign for months. In a classic example of the need to drain the swamp, a US politician bought shares in a company he is responsible for regulating, he gets named and shamed, then other politicians buy shares in the same company days later.

The US tax deduction for mortgage interest is hugely regressive. The US food voucher program, SNAP, could be too generous and making poor people fat. There are good arguments for a flat tax, particularly when combined with targeted welfare and low income tax rebates.

Being more efficient with what we have (productivity) is how people become wealthier. One commentator argues we would be better off if robots destroyed more jobs. Austria is looking to tax Google searches and Facebook interactions.

Colorado is struggling to fill transport jobs as many applicants test positive for drugs, particularly marijuana. Synthetic heroin use is skyrocketing in the US with manufacturers and dealers cashing in. Women are finding few good men left in the rustbelt as drugs and unemployment take a toll. American employers steal $15 billion a year from their employees. Non-compete clauses for workers discourage competition and growth. Amazon’s success is blamed for bringing Seattle problems. Baltimore has high per student funding but awful test results, proving more money for schools isn’t a magic solution.

Adding batteries to natural gas generators can yield extra revenue for generators for the quick start capability. A machine is in production that recycles plastics with a 2.5 year payback period. A hedge fund manager that earnt $11 million a year won $160 million in damages from a casino that beat him up. Las Vegas buffet waste goes to feed pigs, which then end up back on the buffet. China was amongst the worst impacted by the Wannacry computer virus due its widespread use of black market copies of Windows software which don’t get updated. China is mocking western liberals for ignoring real world problems. Chinese click farms are the easy way to get lots of likes and followers on social media.

If you want the version with all of the links you can find it here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

5 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management