New era for central banks

Elizabeth Moran

Elizabeth Moran Consulting

FIIG Securities guest economist, Saul Eslake looks at the current global shift by central banks in ‘advanced’ economies to increase inflation, rather than keep it down as seen in the past decade. He also details why tax cuts and Trump tariffs are likely to put the US under inflationary pressure this year.

The number one concern for central banks

Over the past decade, the number one concern for central banks in ‘advanced’ economies has been low inflation. This has been both an intellectual and a practical challenge for central bankers whose pre-occupation for the three decades prior to the onset of the global financial crisis had been trying to keep inflation down, rather than the need to push it up. Hence the need to push interest rates down to previously unimaginable levels – below zero, in some cases – and keep them there for an extended period; and to develop a new suite of tools to expand the capacity of central banks to address hitherto unimagined obstacles.

But this phase in the history of central banking appears to be drawing to a close. As evidenced by:

- The US Federal Reserve has already raised its principal policy interest rate five times, and begun to unwind the expansion in its balance sheet that began during the initial stages of the GFC.

- Canada’s central bank has lifted interest rates three times since June last year

- The Bank of England implemented its first increase in interest rates since the GFC in November last year

- Almost certainly, the European Central Bank will soon foreshadow an end to its bond buying program, and begin its gradual return to more ‘normal’ interest rate levels, either later this year or early next year

- The Bank of Japan is likely to be the outlier amongst the central banks of large ‘advanced’ economies, maintaining the monetary policy settings instituted during the financial crisis and its aftermath.

This new phase is unfolding for three reasons.

First, there are some signs – albeit not, as yet, unambiguous or incontrovertible – that inflation is beginning to pick up from the historically very low levels of recent years.

Second, central banks are rightly concerned that the extended period of ultra-easy monetary policy has fostered inflated prices of a broad range of financial and real assets, increasing the risks of another financial crisis at some point in the future, if those policy settings were to stay for longer than required.

Third, central banks are acutely conscious that they currently have very little scope to respond to another financial crisis or economic downturn, were one to occur for any reason.

The signs that inflation is beginning to stir are perhaps clearest in the United States. That’s largely because the recovery has been in train longer in the US than in any other major ‘advanced’ economy.

Indeed, the current cycle, although unusually slow by historical standards, will next month become the second longest since at least the middle of the 19th century, surpassed only by the ten year expansion between March 1991 and March 2001.

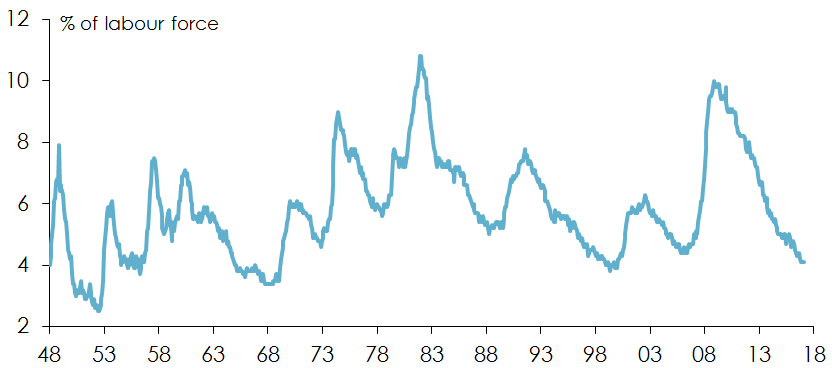

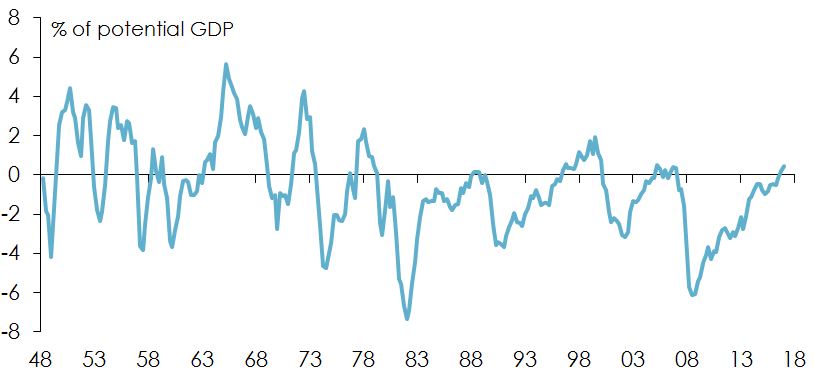

Since May 2016, the US unemployment rate has been below 5% - the level traditionally regarded as consistent with ‘full employment’; and for the past four months has been at 4.1%, lower than at any time since 1969, apart from the last year of the record expansion that ended in 2001, see Figure 1. Broader measures of ‘under-employment’ in the US have also been below their long term averages for more than two years. US GDP has been above its ‘potential’ level, as estimated by the Congressional Budget Office, since the second half of last year see Figure 2.

Figure 1 - US unemployment since 1948

Source: US Bureau of Labor Statistics

Figure 2 - US ‘output gap’ since 1948

Note: The 'output gap' is the difference between actual and 'potential' GDP, potential GDP being the level of GDP when the economy is operating at 'full employment'. Sources: US Congressional Budget Office; US Bureau of Economic Analysis

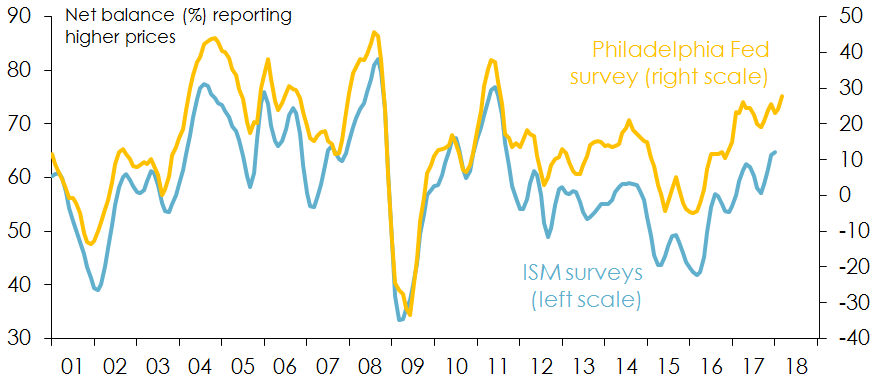

Not surprisingly, ‘upstream’ measures of price pressures, such as those contained in the monthly purchasing manager surveys, or the widely followed Philadelphia Fed Index, are now at their highest levels in eight years (see Figure 3, as is the official measure of ‘producer price’ inflation.

Figure 3 - Upstream’ measures of US price inflation

Note: ‘ISM surveys’ is the average of the ‘prices paid’ component of the manufacturing and services surveys. ‘Philadelphia Fed survey’ is the average of the ‘prices paid’ and ‘prices received’ components. Both expressed as three month moving averages. Sources: US Institute of Supply Management; Federal Reserve Bank of Philadelphia.

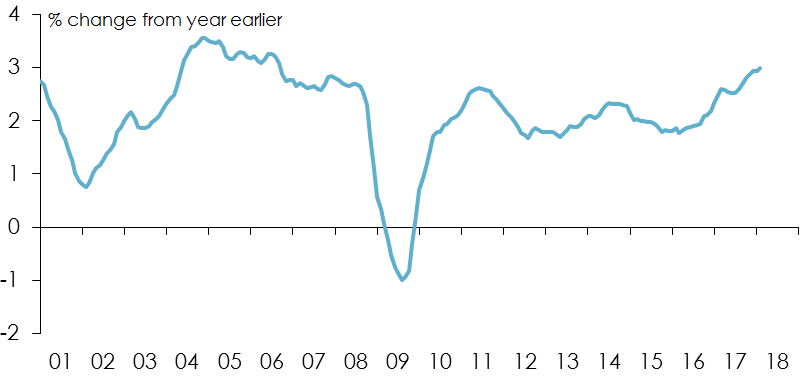

Figure 4 - New York Fed Underlying Inflation Gauge

Note: Series shown is the one from the 'full data set'. Source: Federal Reserve Bank of New York

Moreover, there are at least two developments which are likely to add to inflationary pressures in the US this year.

1. US tax cuts

The first of these is the combination of tax cuts and spending increases implemented over the past few months, which from a cyclical perspective, is perhaps the most spectacularly ill-timed fiscal stimulus in living memory. These measures will boost aggregate demand much more than they will add to aggregate supply at a time when (as noted earlier) the US economy is at or beyond ‘full employment’. They will therefore boost inflation or the US current account deficit, or both, more than they will stimulate growth in real GDP.

2. Trump tariffs

The second is the large tariffs which the Trump Administration is seeking to impose on steel and aluminium – key inputs into a wide range of US manufactured goods – on top of those already imposed on imported timber, washing machines and solar panels, among other items.

Contrary to President Trump’s inaugural address assertion, ‘protection’ will not ‘lead to greater prosperity and strength’. Tariffs are not something a country makes foreigners pay in order to get their goods into that country. They are something a country makes its own citizens pay in order to keep foreign goods out of the country. These (and possibly other) tariff hikes will add to inflationary pressures, while doing little if anything to boost employment.

All of this means that not only is the Federal Reserve highly likely to raise its funds rate target another three times this year – as it has been foreshadowing since the third quarter of last year – but that the risks are increasingly tilted towards the Fed doing more than that.

Until very recently, the bond market has been dubious about the Fed’s stated intentions. They may have some more adjusting to do.

None of this means that Australia’s Reserve Bank will be under any pressure to raise rates sooner than it thinks is warranted on purely domestic grounds. On the contrary, many Australian forecasters – me included – have recently pushed back their expectations as to when the RBA might make its first upward move, in my case from August to November this year, as a result of persistent softness in both price and wage inflation. If other central banks, in particular the US Federal Reserve, raise their interest rates sooner or more often than currently expected, the RBA would delighted if that were to result in a lower AUD.

But Australian bond yields will still likely move in the same direction as their global counterparts, albeit in smaller increments. The time to go ‘long bonds’ in Australia may well come before the RBA is well and truly into its own hiking cycle – as it usually does – but we’re not there yet.

Are you ready to find out how you can earn over 5% pa* with corporate bonds? Click here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

6 topics

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Comments

Comments

Sign In or Join Free to comment