Spotlight on ASX sectors

The once-in-a-century pandemic that is COVID-19 has wrought havoc on global economies and markets. A number of sectors that are typically defensive during slowdowns were hit hard, while others saw massive gains. Will the rollout of the vaccine be the panacea that value stocks have been looking for to make their much-anticipated comeback in 2021?

The year that was

Bushfires; the worst pandemic since the 1918 Spanish Flu; people housebound due to lockdowns; nation-wide border closures, and the first recession in 30 years (that also happened to be the one of the shortest) were just some of the unprecedented events that occurred in Australia during 2020.

The stock market impact of the pandemic was unique compared to a typical correction and recession.

A number of sectors that are typically defensive during economic slowdowns and stock market corrections were adversely impacted. Toll roads, airports and casinos were all hit hard due to the lockdowns and border closures. Conversely, consumer staples massively outperformed early as sales grew substantially—partly due to panic buying—followed by discretionary retail related to electronics and the home as people renovated and fitted out home offices during the lockdown.

The recession was short lived within Australia as the state and international border closures, together with the lockdowns, mitigated the impact of COVID-19 spreading. The swift government intervention via fiscal and monetary stimulus materially reduced the impact of the lockdowns.

Morgan Stanley estimates that some $170b of crisis support was delivered to consumers during the crisis. Many consumers found they had fewer avenues to spend money (e.g. eating out, entertainment and holidays) and thus excess cash found its way into other non-discretionary retail spending.

The year ahead

We believe the 2021 year should bring a return to more normal conditions with the rollout of the many vaccines. There is no doubt the rollout of the vaccine is likely to be slower than many would want due to logistical constraints and the take-up of the vaccine by people. However, the market is always forward looking and given the end game is in sight, it should respond commensurately as the impact of the pandemic reduces.

The recovery in 2009/10 post the GFC also didn’t have all the answers initially. The recovery should see strong EPS growth across many sectors with a number of the forward-looking indicators such as Purchasing Manager’s Index (PMI) and Institute of Supply Management (ISM), and even consumer confidence pointing towards a typical response post a recession.

The combination of ongoing and increasing government stimulus will help drive the likely strong GDP growth globally from such low levels. This is likely to be inflationary resulting in commodities rising, USD falling and a steepening yield curve that will be positive for the more economically sensitive cyclicals, financials and reopening stocks.

The trade tensions with China remain real with little signs of it abating. The broader risks remain, whether the dispute moves from some isolated stock issues (e.g. wine, barley, lobsters, or thermal coal) to something broader that impacts the equity market and FX.

Currently, China’s share of Australia’s exports sits at around 40%. Iron ore is by far the largest export contributor with little ability for China to find alternate suppliers in the short to medium term. However, there is no doubt that China is looking to reduce its reliance on Australia for iron ore via new wholly owned mines in places such as Africa. Previous trade disputes between China, Japan and Korea have lasted around two years.

Interest rates will remain low for the foreseeable future as central banks globally try and buy time for economies to trade out of the pandemic mess. Bonds will partly reflect the short-term rates but also inflationary expectations and everything points towards inflation moving up. In this environment, we believe hard assets (e.g. commodities and real estate) and economically sensitive stocks such as cyclical and financial stocks will likely do well.

There are broader market headwinds (particularly in the US) due to the potential unwind in the concentration of the index heavyweights. A continuation of the value rotation will see ETF and pension fund rebalancing and thus making it difficult initially for the broader indices to outperform. This has become particularly acute given the incredible outperformance of these stocks over the past few years. However, the alpha opportunities will be immense, making fundamental stock picking a key driver for outperformance.

Spotlight on the sectors

Consumer staples

COVID-19 was a driver of strong sales during 2020. Online sales also increased. The high demand had the additional benefit of reducing promotions and competitive intensity. The level of competition in the supermarket sector was already weakening due to the announcement that Kaufland was quitting Australia. This means that Aldi remains entrenched as the dominant discount food retailer in Australia and does not need to aggressively price to gain market share.

While costs were elevated due to COVID-19 requirements, the outlook for supermarket profits improved due to the higher sales and the lower level of discounting.

In 2021, the sales benefit from COVID-19 is expected to ease, particularly as the strong sales from March 2020 are lapped.

However, the higher level of in-home consumption is expected to continue to contribute to sales, with expectations for supermarket sales now higher than they were pre-COVID-19. The lower level of promotions are also expected to continue to benefit industry profitability. Lastly, online sales are expected to reduce but to a higher level than pre-COVID-19, which will particularly benefit Coles and Woolworths.

Discretionary retail

The performance of discretionary retail varied substantially during 2020. Demand for home products increased substantially, so hardware, office equipment and furniture all experienced large increases. In contrast, those retail businesses exposed to travel or entertainment performed poorly. Spending was shifted from travel and out-of-home entertainment to products that enhanced home life. This situation is expected to continue in 2021 until the economy opens up and the companies start lapping the strong sales numbers.

The outlook for 2021 is less rosy. Assuming out-of-home entertainment and travel become available, we believe spending will shift back to these alternatives, and the very high level of demand for home products will revert back to normal levels.

COVID-19 has led to a large increase in online shopping. When access to shops returns to normal, the level of online spend will come down but the trend to online shopping will be accelerated. Incumbent Australian retailers have more to lose from this shift as Amazon and eBay continue to gain traction in this market.

Gaming

Despite traditionally being very resilient in economic downturns, 2020 proved to be extremely tough for the majority of stocks within the gaming sector. Unlike typical recessions where “sin stocks” historically have done well—gaming, wagering, and lotteries sales tend to hold up better than other consumer discretionary spend—COVID-19 proved to be anything but a typical recession. The closure of pubs, clubs, casinos, and wagering outlets meant revenue from bricks and mortar customers effectively went to zero.

Despite the setbacks from venue closures, the reopening of venues once lockdown eased proved how resilient gaming spend is.

Tribal casinos in the US opened to record gaming spend despite social distancing measures still in place. Australian and New Zealand casino gaming spend is tracking to pre-COVID-19 levels, despite more restrictive social distancing measures than those seen in the US. Clubs and pubs in Australia appear to be performing even better than their casino counterparts.

In addition to the resilience of gaming spend, another shift we are witnessing is the acceleration of traditional bricks and mortar gambling towards smart phone gambling; be it in wagering, lotteries or online casinos. It is hard to envisage this trend reversing, with Tabcorp’s wagering business the loser of this trend but a net beneficiary through its online lotteries, while SkyCity, through good management or good fortune, is well placed to take advantage of this dynamic.

Infrastructure & utilities

Infrastructure and utility stocks are generally perceived to be safe havens in economically turbulent times, as demand for toll roads, airports, gas pipelines, and electricity networks are generally resilient to economic cycles. That said, lockdowns and restricted travel measures saw toll roads and airports hit hard, with the share price of Transurban and Sydney Airport reflecting this dire outlook.

We took this opportunity to build a meaningful stake in Transurban. Our preference for toll roads over airports reflects our view that domestic land travel will recover faster than international air travel. For Transurban, the shift to more work from home and thus less intra-city toll usage will be offset by the desire to avoid congested public transport, and thus more driving.

Unfortunately for Sydney airports, there is no offset. While domestic travel should recover quickly, the recovery of international travel is more problematic. In addition to a recovery to demand, international travel requires multi-lateral international agreements on vaccine and quarantine rules. Historically, international flights have taken up 15% of apron slots, but have contributed to 40% of passengers and 70% of revenue.

Thus, the recovery in airports is still likely to be a multi-year story.

Banks

Banks were at the epicentre of the government mandated lockdown, falling precipitously in March 2020. The tail risks around large impairments due to businesses going bankrupt and mortgage defaults weighed on the stocks. The banks helped customers and the government by allowing customers to defer debt repayments for an extended period rather than place them into default.

Dividends were cut substantially due to a combination of both lower earnings and as a result of APRA placing constraints on the ability for banks to pay.

The outlook for the sector is substantially rosier than one would have thought six months ago.

The level of loan deferrals has reduced materially, and the banks look well provided for the increase in bad debts post government support reducing and finally removed. Unlike international banks, which are leveraged to the long end of the interest rate curve, net interest margins for Australian banks are unlikely to move higher in the short to medium term given the outlook for cash rates.

Housing lending growth looks to be robust given monetary policy, however at this stage business lending growth seems less so. Given the strong capital position, modest credit growth outlook and bad debts well provided, we expect banks to start increasing dividend payout ratios.

Given all that, the sector looks attractively priced within an environment where a number of the tail risks have reduced substantially. Over the next few years, we believe banks will return to the mantle as the highest paying dividend sector.

Diversified financials

Outside a narrow number of stocks, diversified financials have had an extremely difficult year, hit hard by the precipitous fall in markets in March. Leaving aside beta linked revenue, market linked stocks generally perform poorly in volatile markets, as net funds flow dries up when volatility is heightened. The volatility in 2020 heightened the pessimism to the sector from the Royal Commission in 2019.

That said, the sector now looks extremely cheap, with stocks like IOOF standout value.

Should market volatility subside in 2021, fund flows into the superannuation and investment system should return, given cash provides little protection to inflation or longevity risk. A return to organic growth should see the sector rerate materially from here.

Insurance

General insurance is normally considered to be somewhat defensive during economic downturns. While general insurance brokers showed this resilience, for the insurers themselves this was not the case as COVID-19 produced a major surprise.

While it is generally understood that there is a pandemic exclusion for business interruption insurance, COVID-19 resulted in increased claims and major uncertainty in this business line, as most insurers had poor wording in a meaningful proportion of their policies, which meant the pandemic exclusion did not hold in these policies. As a result, the share prices of general insurers underperformed significantly, as negative sentiment weighed them down and they de-rated meaningfully.

Looking forward, these unexpected COVID-19 claims are likely to result in a stronger than expected premium rate outlook, resulting in an improved profit outlook for the general insurers.

Healthcare

The nature of the COVID-19 pandemic resulted in divergent outcomes across the healthcare sector. The two primary factors that drove the variant outcomes between stocks was whether they directly benefited from increased demand due to COVID-19 or had any disruption in regard to access to services as a result of COVID-19.

In the first camp, Ansell and Sonic Healthcare both benefited from an increase in demand for their products (personal protective equipment in the case of Ansell) and services (COVID-19 testing in the case of Sonic). Other companies were impacted by restricted access to the services they provide, such as elective surgery in the case of Ramsay Healthcare and plasma donations (shortfalls in which undermine future supply) in the case of CSL.

For Resmed, there were elements of both: increased ventilator sales, which were thought to be crucial in the therapeutic response to COVID-19, as well as increased resupply of masks and accessories due to an easier access to patients who were working from home. This was offset by reduced CPAP sales, as sleep testing labs were shut down.

The outlook for the sector is again very stock specific. While Ansell and Sonic will see the elevated demand normalise over time, other companies may see a sustained benefit or structural improvement in their activities.

Ramsay Healthcare will benefit from the backlog of surgical patients who went untreated for much of 2020. Resmed may see a sustained increase in diagnosis rates as home sleep testing increased in acceptance due to the closure of sleep labs. For CSL, whilst the disruption in plasma supply may undermine availability of their products in FY22, the shortage of plasma has enabled meaningful price increases, which will likely be sustained even after supply normalises as and when the virus is brought under control.

Oil & gas

Oil & gas was one of the hardest hit sectors from the global COVID-19 response. The impact of containment measures across the globe brought mobility to a halt. In April, the worst of the near concurrent lockdowns saw almost one third of demand removed rapidly to levels not seen since 1995, sending oil prices plummeting.

OPEC+ scrambled to respond and, in reasonably short order, managed to cut about 10mb/d. Other producing nations, including the US and Canada, also contributed—whether by choice or the economic reality of sub $30 oil prices.

The supply response provided support for crude prices, further buoyed by China’s stimulus-fueled reopening and progressive uplift in most transportation demand from the trough levels, with the exception of international air travel, which continues to be restricted.

Oil and gas equities broadly followed the lead of crude, though decoupled to the downside in 2H2020, as the predominately LNG exposed sector saw earnings suffer on lagged oil-price sales.

The lead into 2021 has certainly been positive for oil. As oil suffered from COVID-19, it stands to reason it benefits from positive vaccine announcements. The market is looking forward to a return to normality with the final 5 – 10mb/d of demand occupied by international travel to return some time in 2021 or 2022.

We believe the oil and gas space is poised to do well in 2021 as economically driven supply curtailments will persist.

US shale is now mostly in the possession of more economically rational majors after a period of consolidation and juniors may find access to debt more restrictive.

Capex plans of oil and gas companies were deferred in 2020, and given the long cycle time for material oil developments, these delays could see a more rapid drawdown of the inventories built during 2020. Add to this the likelihood of a global economic recovery and the energy space appears well positioned. The risks are meaningful; the OPEC+ response to falling stocks could see a rapid resumption of production and China’s reaction to rest-of-world economic recovery could see it start to intentionally cool its growth outlook.

Mining

Industrial metals and steel making raw materials suffered in early 2020 due to the COVID-19 lockdowns, though the degree of price falls was highly varied. Iron ore was the most resilient while industrial metals (copper, nickel) fell sharply from more lofty levels.

From the late March lows, however, the experience has been that of significant recovery, buoyed by China’s loose fiscal and monetary policies aimed at lockdown recovery and offsetting weak external demand as the rest of the world (RoW) remained shut.

Supply issues also assisted the positive market sentiment, with COVID-19 impacting numerous mining jurisdictions, particularly in South America. Energy minerals were varied, with metallurgical coals reasonably supported by China’s steel growth, while thermal coal became (and is still) entangled in poor China-Australia relations.

Gold was a clear beneficiary of the chaos driven by COVID-19, with the sector reaching record levels and the highest levels relative to market since the post-GFC surge. Ex-gold, the mining equities fell in lockstep with the commodities over February/March, but rapidly recouped the losses by mid-year, strengthening further on vaccine news and a resolution in the US election.

ESG has been a major issue for the Australian mining sector following the destruction of 46,000-year-old rock shelters by RIO at Juukan Gorge in May, ultimately leading to the resignation of three executives including the CEO. The positive to come out of the incident was the attention Aboriginal relations received; old legislation is being updated and mining companies are under intense scrutiny from the investment community, which should hopefully drive good outcomes in indigenous engagement going forward.

Carbon has also been a key issue in recent weeks, with a number of resource companies detailing carbon reduction plans, including a few with ambitious targets of net zero by 2040 and beyond using a number of alternative energy options, like renewables and hydrogen and carbon capture and storage.

The outlook for 2021 looks positive for commodities and exposed equities with the caveat around the uncertainty of China’s response if the rest of the world emerges from recession after the roll out of vaccines.

Commodities should perform well in inflationary environments. Recovering unemployment and government stimulus should aid that outlook, combined with potential US dollar weakness on the expectation the Biden administration is less aggressive on foreign policy reducing geopolitical risk, which caused some to find safety in the greenback and gold.

The key issue we face is many commodities are trading well above their marginal cost of production, but there appears to be limited capacity for high cost production to enter to provide balance. Iron ore is a good example of this, given Vale’s continuing struggle to lift output. This can lead to higher prices for longer and a good period of over-earning from the miners, which can be returned to shareholders and provide additional stock support.

As mentioned, the caveat is China’s response to an RoW recovery, and if the country were to tighten fiscal and monetary policies to reduce future risks, the impact on commodity demand could be material.

This is likely a 2H2020 issue, with work funded by 2020 stimulus still in progress.

REITS

The property stocks massively diverged in performance depending on the impact of tenant occupancy and rent. Assets that were predominately retail, materially underperformed and fell to below half their stated book values. Office fared better since the tenant base was less exposed to the troubled SME sector and rent was more certain. Industrial outperformed through COVID-19 as the ecommerce thematic strengthened through all of this.

The outlook remains uncertain for most of the sector as leasing activity is still poor and tenants grapple with their structural needs for both office and retail physical space. However, the retail and office operators have had plenty of conservatism priced into their share price as their stocks now imply further material asset devaluations. Whilst accelerated work from home and online shopping will fundamentally lower demand, lower rates and a healthier than expected consumer/workforce would suggest the pessimism priced in may be overdone.

The value rotation is just starting

The ongoing signs of improving global macro conditions; monetary stimulus unlikely to end anytime soon; extreme valuation differentials, and incredibly stretched positioning is a compelling backdrop for the value rotation to endure.

The stark secular outperformance of growth vs value, and perhaps even defensives relative to value, since the GFC has been difficult for a fundamentally based bottom up value investor. This long-term trend has been driven by a combination of low interest rates and inflation expectations and economic growth, together with the incredible success of the technology sector.

As a value manager, our conviction lies in a process that is based on long-term sustainable earnings and cash flows, priced on appropriate multiples. So, when the market reverts to more normal conditions, a patient active value manager (and investor) can benefit enormously.

The global business cycle continues to surprise on the upside with strong PMI and ISM data helped by the unprecedented and quick government interventions. With vaccines rolling out globally, economies are starting the long road of recovery out of the pandemic-induced economic shock.

Interest rates have essentially been anchored by central bank intervention globally while inflation expectations are showing a recovery from low levels. This setup has historically been positive for value as bond yields trickle up, resulting in a steepening of the yield curve. We have started to see this play out with bond yields moving higher, which has helped the value/cyclical trade.

Despite the recent rotation and thus sharp rally in value, it has still materially underperformed growth over the past 12 months and has a long way to reverse the underperformance over the past few years. Value typically outperforms for at least 12 months after a major trough in earnings and we see no reason for this not to be repeated.

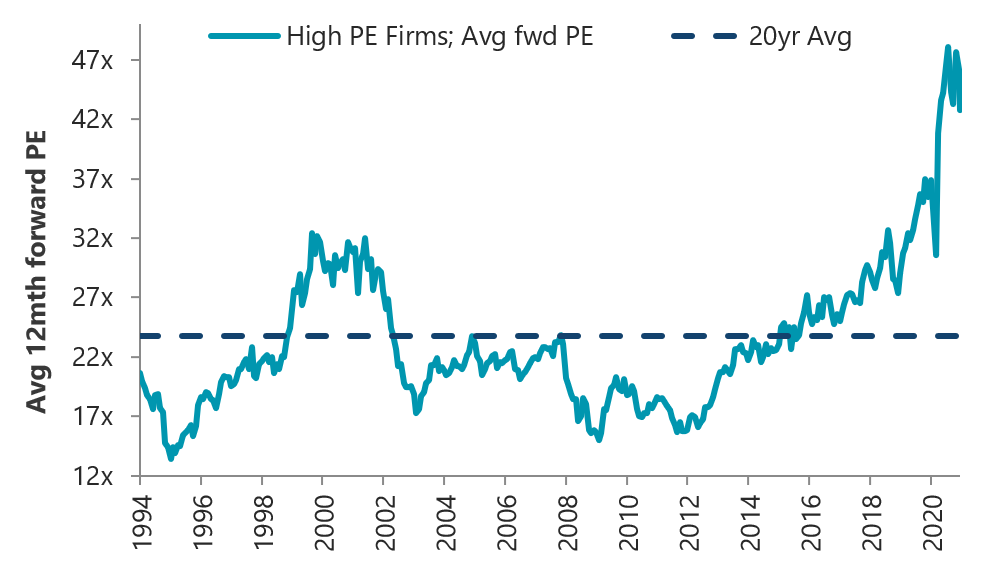

What makes this rotation even more fascinating is the combination of the enormous dispersion in value together with the huge skew in positioning. Performance will be generated not just via undervalued stocks re-rating higher but, just as importantly, expensive stocks will de-rate. Chart 1 illustrates how expensive versus history the high PE stocks are now trading.

Chart 1 – High PE stocks trade at an average PE of 42.8x, which is 80% above the 20-year average

Source: Goldman Sachs

The tough decade for value investors has created attractive investment opportunities that a well-disciplined value investor can harness.

Our process is well positioned to take advantage of the opportunity set that requires a long-term investment horizon that looks through the current uncertainty, and a detailed bottom-up focus that identifies attractively priced companies the market is ignoring that we believe are positioned to be rewarded in the economic recovery.

Learn more

Click the 'follow' button below to be the first to read our latest value investing insights, including where we are finding the most compelling opportunities on the ASX.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was Director, Corporate Finance with Westpac, a Senior Resource Analyst with Ord Minnett and in his early career, a geologist working with a number of resource companies. Brad has portfolio management responsibilities for the Tyndall Australian Share Wholesale Fund and Tyndall CVA Plus Strategy. He has analyst responsibilities for Banks.

........

Important information: This material was prepared and is issued by Nikko AM Limited ABN 99 003 376 252 AFSL No: 237563 (Nikko AM Australia). Nikko AM Australia is part of the Nikko AM Group. The information contained in this material is of a general nature only and does not constitute personal advice, nor does it constitute an offer of any financial product. It does not take into account the objectives, financial situation or needs of any individual. For this reason, you should, before acting on this material, consider the appropriateness of the material, having regard to your objectives, financial situation and needs. The information in this material has been prepared from what is considered to be reliable information, but the accuracy and integrity of the information is not guaranteed. Figures, charts, opinions and other data, including statistics, in this material are current as at the date of publication, unless stated otherwise. The graphs and figures contained in this material include either past or backdated data, and make no promise of future investment returns. Past performance is not an indicator of future performance. Any economic or market forecasts are not guaranteed. Any references to particular securities or sectors are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities or sectors and no warranty or guarantee is provided.

3 topics

22 stocks mentioned

Tyndall AM

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was...

Expertise

Tyndall AM

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was...

Expertise

Comments

Comments

Sign In or Join Free to comment