The 5 forgotten bigcaps

Alex Cowie

Livewire readers submitted ~2500 stock tips in a survey we ran at the start of the year. We published the ’10 most tipped stocks’ and ’10 more of the most tipped’ off the back of the results. However, in this wire, we put our contrarian heads on and ask: ‘Which big caps got no tips at all?’ ... and the results are astonishing. It turns out there is a cluster of quality big caps that were almost totally overlooked.

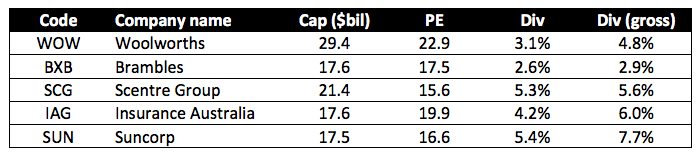

Woolworths, Brambles, Scentre Group, Suncorp and Insurance Australia have an aggregate market cap of $113 billion and outperformed the market by nearly 5% on average in 2018. And while ASX20 stocks received a mean of 25 tips each in our survey, this cluster of five received... just 3 tips between them.

To investigate if there is a hidden opportunity for you here, we have summarised some of the recent fund manager commentary for these stocks.

Just two tips for Woollies?

Woolworths (ASX:WOW) is perhaps the most surprising stock on this list. It is the largest with a market cap of $39.4 billion, it is a trusted household brand, the price has been gaining steadily for 2.5 years, and it returned +7.8% in CY18 (or +11.5% with dividends), compared to –6.9% for the ASX200 (or –2.8% for the accumulation index).

Yet from the ~2500 tips in the survey, Woolies got a grand sum of… 2 tips.

The team at Perpetual Investment have written positively on the stock a number of times in recent years. Vince Pezzullo published a wire called The bull thesis on Woolworths describing the stock as "long on assets and short on market cap," and being worth "$30+ stock at some point". It was $23.27 at the time, versus $28.87 today. More recently, Perpetual's Anthony Aboud looked at the tailwinds from their digital strategy in Old dogs, new tricks to say that:

"The Woolworths digital transformation is a work in progress, and early signs of the sales line and customer satisfaction have been extremely encouraging. Shareholders are already wearing the costs of these investments and have yet to get the full cost benefit. We think the risk-reward is good, with an unleveraged balance sheet following the potential petrol disposal, a strong market position and future profitability benefits from the current elevated capital and operating expenditure."

A few weeks ago, Trent Crawley at Vertium also singled Woolies out as a leading candidate for off-market buybacks, explaining the process he used to come to that conclusion, in his wire the next stock to release franking credits, writing that:

“We think the likely candidates to do an off-market buy-back (in order) are Woolworths followed by RIO. With the value of franking credits likely to fall for a significant cohort of investors mid next year, we would encourage all companies with excess franking and under-geared balance sheets to release franking credits as soon as practicable".

No love at all for Brambles!

Another surprise on this list was Brambles (ASX:BXB). A company with a market cap of $17.5 billion, that outperformed the market by nearly 8% last calendar year, and currently trading on an undemanding PE of 17… got ZERO tips at all in the survey.

Brambles is another one rated by Perpetual Investments. A few months ago, in ‘Brambles offers attractive value’, Vince Pezzullo wrote:

"With a new management team at the helm and a renewed focus on free cash flow and operating efficiencies, we believe the stock at the recent lows offered an attractive entry point”.

Marcus Bogdan at Blackmore Capital also nominated Brambles in a wire from November that provided a summary of ‘5 stocks to consider after the correction’.

Scentre Group: Zero tips

Scentre Group (ASX:SCG) was another ASX20 stock that was completely overlooked in the survey, despite beating the market last year (just) and having a long history as a reliable payer of an (unfranked) yield of 5.3%.

Scentre has been the topic of positive pieces from two different property specialist managers on Livewire. Michael Doble at Australia’s premium shopping centre portfolio’ that:

“The main thing the market is overlooking in SCG is the quality of the cash flows compared to lesser quality assets and portfolios in the AREIT sector.

Chris Bedingfield at Quay Global Investors also focused on the merits of Scentre Group in his entertaining presentation at Livewire Live 2018. ‘How to win Monopoly in 3 easy steps’.

Insurance: Not sexy

The two insurance giants, Suncorp (ASX:SUN) and Insurance Australia (ASX:IAG), with a market cap of $35 billion between them, were also overlooked almost completely, getting just one tip between them (for IAG).

Admittedly, insurance is not a ‘sexy’ investment theme. However, ask yourself: when was the last time you went to pay your insurance premium and thought ‘Well, that seems very reasonable doesn’t it’?

The fundies are unanimously positive on the sector at any rate. Blake Henricks at Firetrail Investments wrote a detailed wire on the topic called ‘Weathering the storm: An opportunity in Australian insurance’, summarising to say that:

The risk insurers face from large weather events will always be a key talking point for investors, but IAG and Suncorp have shown an ability to successfully mitigate a large portion of the P&L and capital volatility through reinsurance and re-pricing. With defensive characteristics in an increasingly difficult economic environment, we believe domestic insurance represents an attractive sector to be exposed to.

Andrew Martin at Alphinity Investment Management nominated Suncorp in A misunderstood gem at a material discount. Andrew had made a great call on Macquarie 12 months prior, and we asked him if he saw a similar looking opportunity ahead. He wrote that:

We think Suncorp continues to be misunderstood. While investors are often distracted by peripheral issues when it comes to Suncorp, ultimately earnings will be driven by improving insurance margins. These, in turn, will be driven by: An improving pricing environment in both commercial and personal lines insurance; and Taking costs out of the business; both operating and claims.

Five forgotten bigcaps

As for why these stocks had so little attention, my hunch is that it is simply because they are at the smaller end of the ASX20 so have smaller shareholder bases, and also that they are less 'exciting' stocks exposed to less 'exciting' themes.

However, uncertain markets make 'exciting' less appealing, and based on our contributors' investment perspectives, these stocks are clearly worth a closer look.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Alex Cowie,

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

1 topic

5 stocks mentioned

7 contributors mentioned

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Comments

Comments

Sign In or Join Free to comment