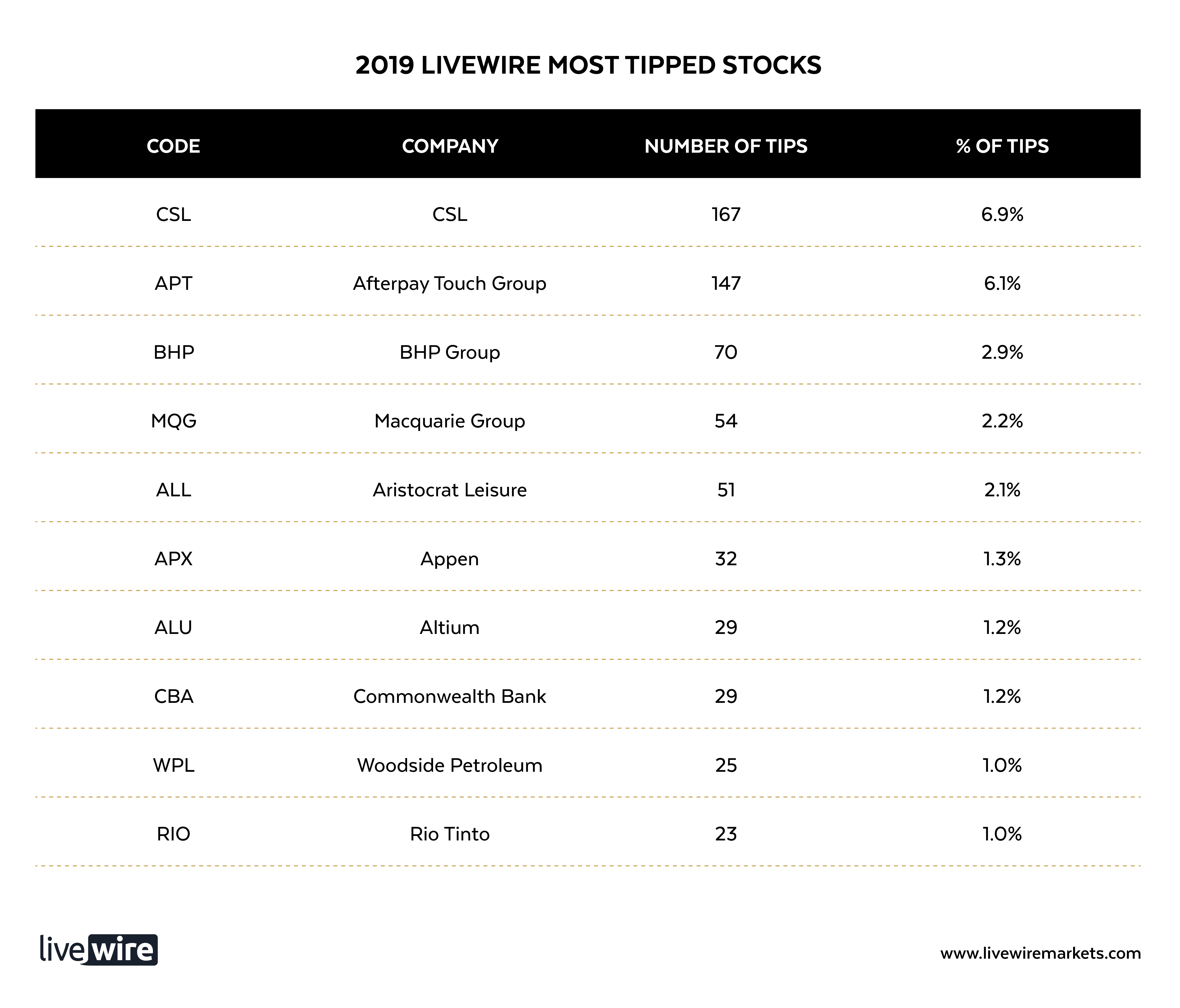

The 10 most tipped stocks for 2019

Alex Cowie

Equity indices everywhere were in the red last year, yet the three most tipped stocks from the 2018 Livewire reader survey, Afterpay Touch, CSL and BHP, all finished well in the black. They gained (excluding dividends) 107.7%, 31.0%, and 15.8% respectively, or 52% on average. While the order has changed, the top 3 this year comprises the same stocks as last year. In addition, the conviction across this group has increased, with the aggregate share of votes increasing from 10% to 16% (from 2,500 participants). Can lightning really strike twice? Let’s see what the fundies have been saying about these three stocks, as well as the new entrants to this year’s most tipped stocks list.

#1 Most tipped: CSL Limited

The fund managers are less sanguine, with Roger Montgomery and Ben Rundle both calling it a 'hold' on valuation concerns in a recent Buy Hold Sell. Roger told Matt Kidman:

“The market is willing to pay for three CSLs for the growth of one, effectively, and we value the business as a sort of ... If it never grew again, it's probably worth 30 or 40 billion dollars. Market was willing to pay over $100 billion for it. You say you often joke, Matthew, that I don't like mining businesses. I think this is the highest-quality mining business in Australia. It mines and refines blood and it does a brilliant job and it's got great product development. It's got low exploration costs. It is extremely high quality. Just too expensive.”

Back in late 2017, Bell Potter included CSL in a shortlist of their ten ‘most favoured stocks for 2018’. They have also backed it up again for this year in this wire saying that: ‘the global growth in plasma volumes is expected to be around a solid 8% per annum for the foreseeable future and, in addition, the group is planning to launch new products from its very extensive Research and Development portfolio”.

#2 most tipped: Afterpay Touch

This time last year, Richard Coppleson nailed it with his nomination of Afterpay as his top pick for Livewire’s 2018 outlook videos, saying: “I think it is an absolute screamer. It’s got a billion dollar market cap, they’ve got 40% EPS growth this year, 50% EPS growth next year, and multiples going beyond that”.

The stock price had quite the journey since then, tripling between April and August, then halving as the market stumbled in Q4, yet still finishing the year up 108% to be the top performer on the ASX200. The price has consolidated more recently, and readers are clearly confident that Afterpay will resume the meteoric rise that has taken it from microcap to midcap in under 3 years.

A number of managers on Livewire are positive on the stock, including Andrew Mitchell from Ophir who focused on the rapid inroads being made into the US market, and recently reminded of the scale of the opportunity in this wire saying:

“With the US market well over 20x the size of the Australian opportunity, the potential for the business to grow significantly from here is obviously apparent. In a short period of time, Afterpay has scaled to 10% of all online transactions in Australia, representing an addressable market of ~US$18bn per annum. In the US, online transactions represent some ~US$450bn per annum, with online fashion alone accounting for US$60bn in purchases each year.”

#3 most tipped: BHP

After five years of declines, the miners turned back up at the start of 2016. The contrarians were followed by the growth managers, and more recently the income specialists are making the case for the sector.

At a recent Livewire / IRESS event, which you can watch in this wire, Peter Gardner from Plato Investment Management focused on BHP (and Rio) as overlooked dividend opportunities, saying:

“In terms of the gems that we see now in the market, it is in a place that people haven't really seen income from in the past, and it's resources. If you look at BHP and Rio, they're both sitting on fully franked yields of over 7% now. Rio has just done its second off-market buyback. BHP is doing a major off-market buyback now, as well as the big special dividend in January. The resource stocks are now on fairly healthy margins from where commodity prices are. Iron ore prices really haven't fallen in the last six months, and given the Australian dollar has, that's just only improved their margins”.

#4 most tipped: Macquarie Group

Like the three stocks above, Macquarie was also on the list last year and bucked the market trend to finish up for the year. Readers are backing it again for 2019, and the stock has had several managers write positively on it on Livewire in recent months.

In October, Andrew Martin from Alphinity wrote about the silver lining in the silver doughnut, in a special piece to revisit a correct call he had made on Livewire in 2017, saying that:

"We continue to have a positive view of Macquarie over the next year, especially relative to other financials. Recent company updates suggest they continue to perform ahead of expectations and we believe their guidance for the full year remains quite conservative".

In ‘what Benjamin Graham would say about this market’, Hugh Dive from Atlas Funds Management focused on Macquarie as a stock that would appeal to the father of value investing himself. Marcus Bogdan at Blackmore also landed on Macquarie as one of “4 stocks to consider after Red October”.

#5 most tipped: Aristocrat Leisure

While the first four stocks on this list were also on last year’s list, the rest of this list, including Aristocrat, are new entrants. And also unlike the first four, Aristocrat went backwards last year so doesn't have momentum on its side.

Several contributing managers are positive on the stock. A few months back, Charlie Aitken singled out Aristocrat as an opportunity in his wire “When rotation goes too far” listing several fundamental drivers and catalysts as to why he believes Aristocrat “at the current share price levels offers a compelling opportunity”. Stuart Jackson at Montgomery ran the ruler over the stock in ‘Aristocrat diversifying beyond machines’, and Steve Johnson included the stock in a theoretical portfolio designed to be recession-proof as well as property-proof in this recent wire.

#6 most tipped: Appen Limited

Machine learning company, Appen, is another ‘microcap to midcap’ story, with its share price up from $0.56 to $14.88 in just over four years. Last year alone, it gained over 50%, despite huge volatility. In a recent piece, 7 questions with Roger Montgomery, Roger cited a basket of stocks, which included Appen, to be cautious of on valuation grounds. He also used this group as a bellwether for a market to be very wary of. He wrote:

"I was frustrated back in September when profitless companies were surging. I wrote for Livewire that a portfolio made up of high-flying stocks like Wisetech, Xero, Appen, Altium and Afterpay was trading at more than 15 times revenue and more than 480 times earnings.

The performance of some stocks – knowing their underlying business model and prospects – was inconceivable so I called a peer in funds management whom I know had purchased some of these stocks. I couldn’t understand how he was holding them even after they had doubled or tripled for him. I couldn’t get a valuation even at the price he’d bought them for.

He confirmed what I suspected; He had suspended any requirement to invest in quality, or at value, and was quite deliberately chasing growth and momentum. So, I pressed him by asking; “if you didn’t buy with any reference to value, and the stocks have more than doubled now, how do you know when to exit?” His reply: “You will see them rolling over.”

At that point I knew we wouldn’t have to wait very long for some sort of correction. When reputable and smart people collectively start doing dumb things, the party is almost always close to over."

#7 most tipped: Altium Limited

Altium is another market darling tech stock with a ‘bottom-left to top-right’ chart, increasing from $2 to $24 in less than 4 years. Like its NASDAQ counterparts, it has also hit volatility in the last year. While Roger Montgomery warned on Altium (see above), Uday Cheruvu at PM Capital was fairly positive on it in ‘Reading the tarot cards of tech’ saying that,

"We also like Altium (ASX: ALU), an Australian-domiciled owned public software company that provides PC-based electronics design software for engineers who design printed circuit boards. Unusually for tech companies, it actually has a PE (around 40 times)! Its underlying business is PCB software - basically green boards that all the chips are put on when you buy tech goods. Altium makes the software that people use to design these boards.

Historically they've had a huge piracy problem; they have not been able to get their users to pay them, particularly in China. However, that problem is turning around as piracy is falling the world over. That means they have re a huge growth potential not because their software is penetrating any further, but that people are starting to pay. That sort of a structural change is a positive for their business which I think warrants their valuation."

#8 most tipped: Commonwealth Bank

I've never thought of the biggest stock on the market as a contender for the top performer in percentage gain terms, but the market can be an unpredictable place!

One key area of concern for income investors is the sustainability of banks' dividends, given the multiple headwinds banks now face. Dr Don Hamson at Plato wrote in Healthy outlook for dividend yields in 2019 that:

“Banks have maintained their dividends in 2018 despite one-off expenses associated with the Royal Commission. While $1.5 billion in pre-tax legal and remediation costs seems large, after tax it is relatively small in the context of approximately $30 billion in annual post-tax profits for the big four banks. When averaged across the 10 years of the Royal Commission review period, it represents less than 1 per cent of annual bank profits over that time. Although we do not predict near-term dividend increases from the banks, at current prices they are all trading on strong dividend yields and below average price-earnings (PE) ratios. The fact that none of the banks cut dividends in 2018, when they could easily have used the Royal Commission excuse, suggests they are reasonably confident they can maintain current levels”.

In November, Michael Wayne at Medallion threw the cat among the pigeons in a wire that argued ‘The Golden age of Banking is over’:

"When looking back over recent decades we would argue that the economic conditions created a ‘Golden age of banking'. Many economic elements moved in a favourable direction over the same timeframe. However, as we argue here, this Golden age of banking is over. Let's break it down by contrasting how 6 key drivers have played out over the golden age, versus how they look today...

He looked at how rates, real wages, de/regulation, household debt, bank credit, and housing prices have turned mostly from tailwinds into headwinds. He was also careful to point out that he thought prices were more likely to oscillate in a range than collapse, and that total returns would be driven by dividends. This wire triggered some passionate debate, in response to which Michael penned a second wire to clarify his view, which was another good read.

#9 most tipped: Woodside Petroleum

There have been some notable bullish calls on the big energy stocks recently, and Adam Alexander at Evans & Partners nominated Woodside in a special series we ran in October seeking top stock ideas, arguing that:

“China’s demand for LNG is booming…. driven by a relentless quest by the Chinese Government for cleaner air and blue skies. Woodside Petroleum is well positioned with infrastructure and resources to supply this insatiable demand.”

#10 most tipped: Rio Tinto

Trent Crawley from Vertium wrote a great wire recently on ‘The next stock to release franking credits’, which explains his screening process for shortlisting the top candidates for off-market buybacks. He landed on 2 stocks, including Rio Tinto, saying that:

“Despite buying back ~10% of its ASX listed register for ~A$2.9bn via an off-market buy-back last month, we think RIO will return in the new year with another, potentially even larger off-market buy-back. RIO has recently announced three asset sales totaling ~US4.5bn, the proceeds of which we expect will be returned to shareholders. The largest of these is its interest in the Grasberg mine in Indonesia worth US$3.5bn. While this is subject to a number of regulatory approvals it is expected to close in 1H19. The one caveat for RIO is there is talk that they may bid for a minority interest in Teck Resources’ copper assets in Chile. This could cost ~US$2bn which would reduce the value of the potential buy-back”.

More of the most tipped stocks?

There are some very interesting, lesser-known small-to-midcaps further down the spreadsheet. If you are interested in being the first to see the follow-up wire covering them, please hit the follow button below. And if you've found this piece useful, please like, comment or share it with investing friends. Thanks for your support, and all the best for a prosperous 2019.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Alex Cowie,

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

10 stocks mentioned

11 contributors mentioned

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Comments

Comments

Sign In or Join Free to comment