Valuations creating once-in-a-lifetime opportunities

Looking back on the start to 2020, it's hard to know where to begin. In Australia, the widespread and devastating bushfires had barely been extinguished by damaging rains when the severity of the global COVID-19 (coronavirus) pandemic became apparent. We wish all our readers the very best during these tumultuous times.

Uncertainty and the anxiety it breeds doesn’t bring out the best in us. Supermarket shelves have been scooped into our trollies, oftentimes without reasonable prospects of future consumption. Similar irrational behaviour is plaguing sharemarkets around the world. Panic and short-termism has led to indiscriminate selling, the weight of which has either squashed buyer appetite or has been met with a buyers’ strike. Share prices have fallen precipitously.

As we write, the S&P/ASX 300 Index is below the levels when we first launched this strategy almost 15 years ago. Markets are rightly obsessed with the elevated levels of corporate debt and the impact that the current coronavirus will have on earnings and solvency. Very little has been spared from the carnage.

But despite being predisposed to pessimism ourselves, now is not the time to panic.

Through a slightly different (longer-term) lens, we see extraordinary value for the portfolios we manage and some once-in-a-lifetime buying opportunities.

Many of these companies have little or no financial leverage, provide a product or service that society needs (or soon will need again) and have superior competitive positions to their peers. Above all though, these companies are cheap.

We already own many of these companies, so it is disappointing to post performance numbers that are even poorer than the broader sharemarket’s. This is not uncommon though, with previous large market drawdowns being similarly indiscriminate. Nevertheless, we’d like to use the remainder of this wire to outline how the portfolios are positioned and our activity in recent weeks.

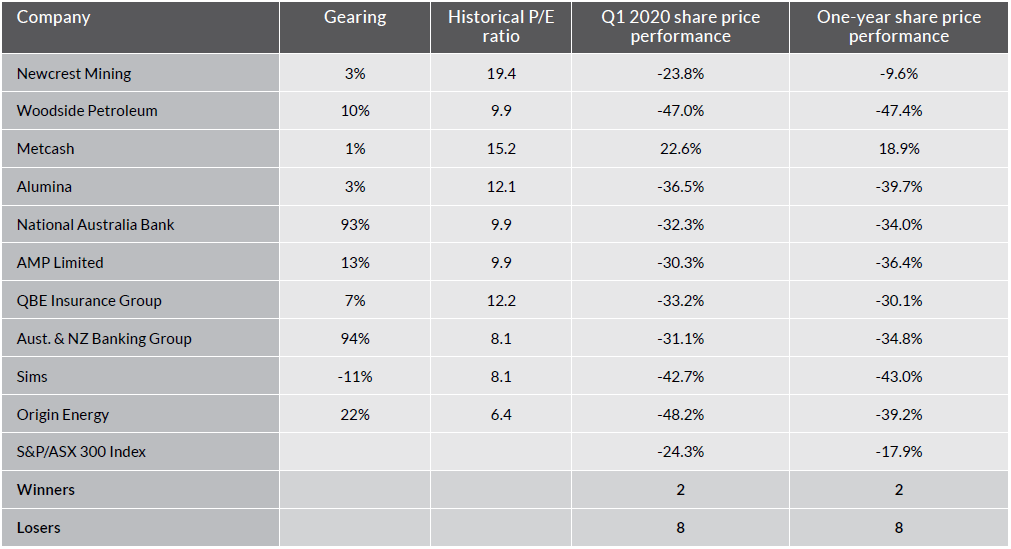

Table 1 shows the top 10 investments which combined represent over 60% of our Australian Equity Fund. Despite these not being the entire portfolio, they are representative of the rest of the Fund and focusing on them will hopefully give our readers insight into how we are navigating these times.

Table 1: Top 10 holdings in the Allan Gray Australia Equity Fund at 31 March 2020

Source: Factset, latest company financial statements.

Column A details each company’s gearing (the ratio of net debt to total assets), a widely used measure of indebtedness. Column B details each company’s price to earnings ratio for its most recently reported 12 months. Given that forecast earnings are so difficult to predict today, a pre-virus earnings level is most likely the best indication of medium-term future earnings prospects. Columns C and D show the performance of these companies over the past quarter and year.

There are a number of key takeaways about the companies in this table

#1: They are generally lowly geared. For most of these companies, the vast majority of their asset bases have been funded by equity, not debt. In Sims’ case, it has net cash, invaluable at times like these

Two exceptions are National Australia Bank and Australian and New Zealand Banking Group (ANZ). Their business models are a little different to most companies as they are in the business of borrowing money from savers and lending it to borrowers. Banks by their very nature are geared beasts and particularly prone to economic downdrafts given the loan impairments that often follow. At least some of this risk is already factored into the current share prices, with both banks trading well below their net tangible asset (NTA) levels.

The banks are better capitalised than they’ve ever been before, mostly better capitalised than overseas banks and as cheaply priced relative to NTA as they were in the early-1990s.

#2: They trade at very low multiples of recent earnings which, without exception, we believe are very low themselves. We have no competitive advantage in assessing the length of time the current virus disruptions will last, but little suggests it will be permanent. Earnings will recover.

It is worth clarifying two exposures in our top 10: gold (Newcrest) and energy (Woodside and Origin). In Newcrest’s case, the gold price is over A$2,500 per ounce today, 40% above last year’s levels with profits expected to increase materially on 2019’s levels. Newcrest is far more attractively priced than the 19 times historical P/E multiple suggests.

Our energy exposure is almost the complete opposite. In 2019, Woodside’s realised oil price was US$50 per barrel, well above today’s low- to mid-US$20s per barrel. We expect its profits to fall materially in 2020 but we believe this to be unsustainable. At current oil prices, we believe Woodside is well positioned to survive and then thrive. We’ve addressed its low gearing above but its exceptionally low cost of production (in the low US$20s per barrel) will insulate it from the spiralling losses and gearing increases which plague other oil and gas producers.

But even at US$50 per barrel, large swathes of world oil production was already in decline, capex budgets were being reduced and the financial sustainability of the massively indebted US oil producers was questionable. At today’s oil prices, well in excess of five million barrels of daily oil production would be loss making in the US alone. Low- to mid-US$20s per barrel is simply not sustainable and we expect supply to rapidly adjust to today’s reduced demand. We remain confident that oil prices will significantly exceed US$50 per barrel in the years to come but we acknowledge that the path there is likely to take longer than we had first anticipated.

Our energy exposures have been our largest detractors from a performance perspective, but also offer some of the greatest future returns potential for the Equity Fund.

#3: They have significantly underperformed. During the quarter all but two of these companies (Metcash and Newcrest) underperformed the broader sharemarket. Given how weak these company share prices had been leading into the quarter, the continued underperformance appears overdone and may be consistent with the indiscriminate selling which riddles markets today. None of these companies have sustained any significant impairment to their value and all appear to be attractively priced.

Our actions during the current market sell-off

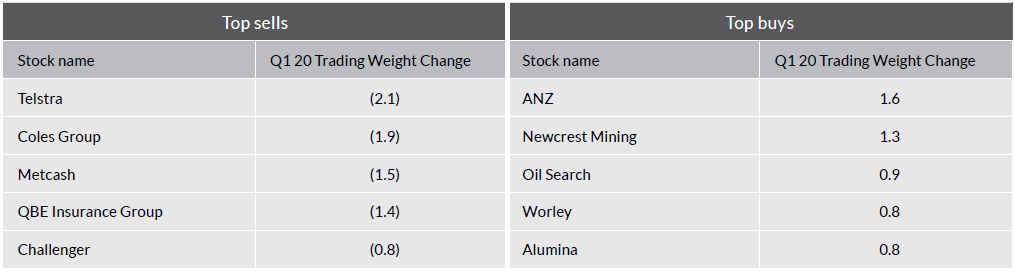

We haven’t changed the way we manage money or how we view companies. The value of a company remains the present value of its future dividend stream. We have maintained our dogged focus on company fundamentals, taking advantage of mispricings as we believe they’ve presented. Table 2 shows our trading activity during the quarter (other than for new positions less than 1% of the portfolio which we don’t disclose).

Table 2: Top five buys and sells in the Allan Gray Australia Equity Fund during the quarter

Source: Allan Gray.

During the quarter we’ve exited our Coles holding and significantly trimmed our Telstra and Metcash holdings. Sales of QBE and Challenger were done in February after they reported stronger than expected results and their share prices significantly outperformed. In both these cases, this strength has completely reversed, in Challenger’s case, materially so (a fortuitous sell on our part!).

Other than our significant additions to ANZ and Newcrest, our buying has been more widespread and measured in anticipation of companies raising equity to bolster their balance sheets. Our buying in Oil Search has been partly offset by some selling in Woodside although on balance, we have modestly added to our energy exposure.

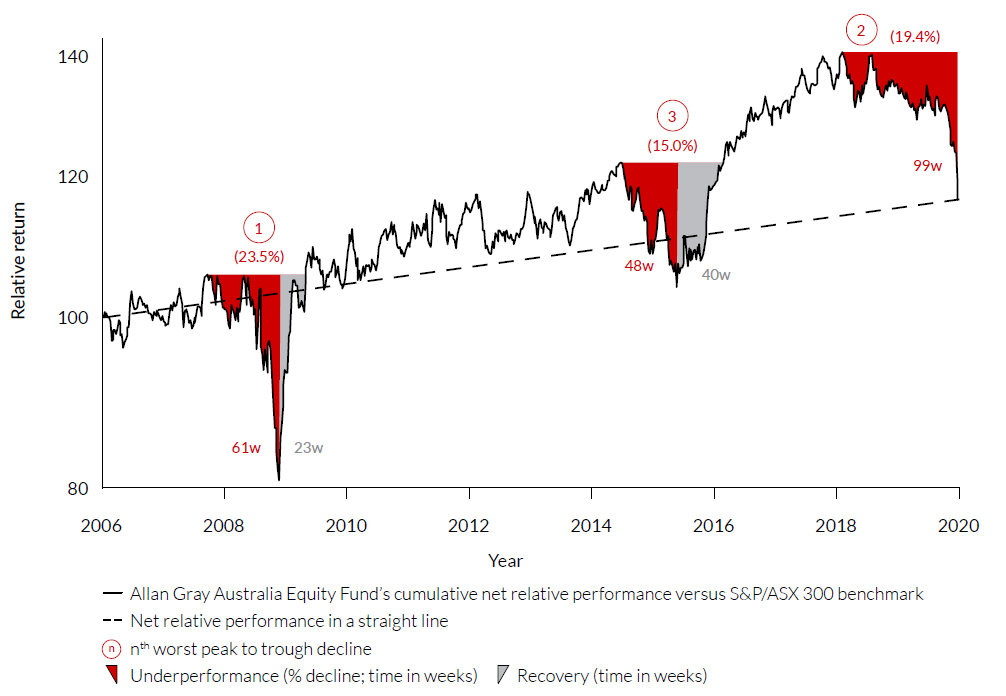

Before ending, it is worthwhile reflecting on what has happened during our previous drawdowns. We’ve been here before in 2008 and 2015. As Graph 1 shows, in both instances the recovery was significant and patient investors were rewarded handsomely. While past performance can never be relied upon to predict future performance, we nevertheless feel the opportunities presented to our investors today are strong.

Graph 1: Relative return of the Allan Gray Australia Equity Fund versus the S&P/ASX 300 Accumulation Index

Source: Allan Gray. Past performance is not indicative of future performance. Net relative performance is shown for Class A of the Allan Gray. Australia Equity Fund and is calculated on a geometric basis.

We appreciate that these are difficult times and as much as we would have liked to have generated far better returns than we have this quarter, we are excited about the future prospects for the portfolio.

Find out more

Contrarian investing is not for everyone, however there can be rewards for the patient investor who embraces Allan Gray’s approach. To stay up to date with our latest thinking, hit the follow button below or contact us for further information.

The above wire is an extract from Allan Gray Australia’s March 2020 Quarterly Commentary, which you can read in full here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan Gray in 2006 as an analyst, bringing with him a strong background in finance from previous roles at Alliance Bernstein, Macquarie Bank, and Deloitte & Touche. Simon holds a Bachelor of Business Science (First Class Honours) in Finance and Business Strategy, along with a Postgraduate Diploma in Accounting, from the University of Cape Town. He was a Chartered Accountant and is a CFA Charterholder. Known for his contrarian, long-term, value-driven investment philosophy, Simon speaks frequently at industry events and appears in media interviews, offering perspectives on specific securities, as well as portfolio positioning and the Allan Gray contrarian investment strategy.

3 topics

12 stocks mentioned

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan...

Expertise

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan...

Expertise

Comments

Comments

Sign In or Join Free to comment