14 big-caps most likely to slash dividends

Income investors should brace for an overall 30% reduction in dividends across the Australian share market, according to Plato Investment Management.

The economic fallout from COVID-19 will present those relying on yield the twin-challenge of receiving reduced payments from shares and navigating dividend traps, the income investing specialist’s Peter Gardner and Dr Don Hamson told investors at a webcast yesterday.

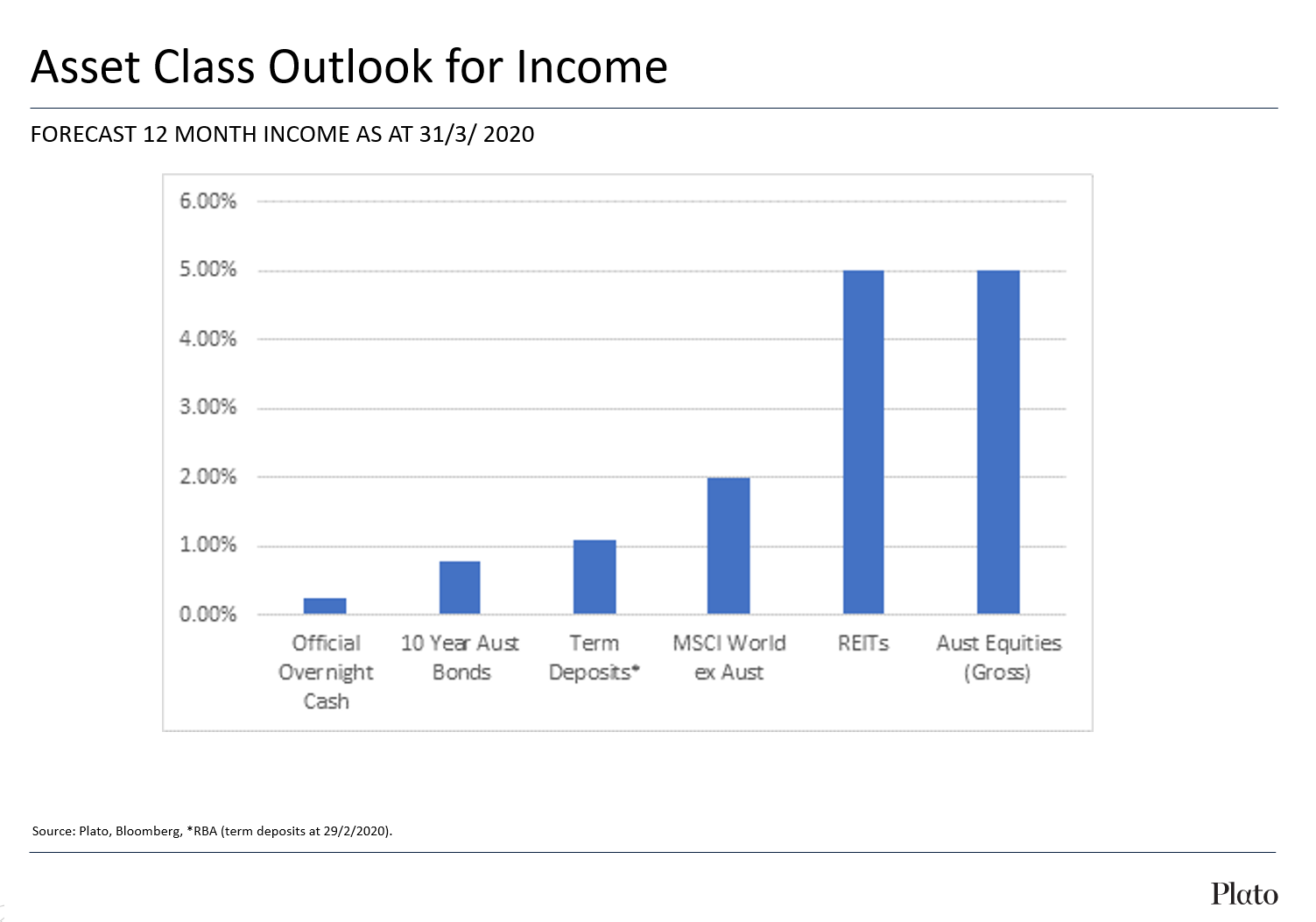

The forecast was based on the experience of previous downturns; the 2008 global financial crisis and the early 1990s Australian recession. This means investors would need to recalibrate their yield expectations on Australian equities to 5%, down from 7%.

“We're looking at numbers around the 30% type based on falls in dividends in the two previous downturns that we've seen, even though the GFC wasn't a technical recession. But that, to me, gives you an idea that at the broader index level, you can see dividends being cut. The impact is very stock specific and sector specific. Some industries are actually doing better out of this but clearly some are in significant trouble.”

Which stocks are most at risk?

Gardner went on to apply Plato’s modelling across the biggest dividend payers, being the top 20 ASX companies, to call out who’s most at risk. This list aligns to the prediction made by Livewire readers at the start of the year that the major mining stocks would be a better place for income than the Big Four banks in 2020. The 14 stocks at medium-to-high risk of slashing payouts are dominated by financials, while BHP, Rio, Fortescue and the usual defensive names have a low chance of reducing dividends.

Gardner laid out his thesis across sectors and stocks as follows:

- Resources/energy: BHP, Rio and Fortescue are benefitting from iron ore prices staying high as China has continued to produce lots of steel being used in infrastructure-related stimulus. There have also been supply issues around the world, with India and South Africa lowering output. South32 on the other hand doesn’t have exposure to iron ore, so its earnings will come under pressure. Energy stocks are being dragged by low oil prices.

- Defensive stocks: Telstra and the supermarkets are benefiting from a surge in demand for data usage and essential buying. Meanwhile, Wesfarmers has a higher exposure to discretionary spend which will probably be weak in this environment. AGL and Transurban are expected to take a hit due to falling power demand and restrictions on non-essential travel.

- Diversified financials: ASX and Macquarie, as well as insurers, would see reduced investment earnings given falls in markets as well as rate cuts by central banks.

CBA stands out from the Big Four

Picking apart the banks, CBA is a ‘medium risk’ as it holds a higher amount of capital relative to other banks and is receiving proceeds from asset sales. Still, the biggest Australian lender would likely defer its mooted off-market buyback planned for later this year.

“However, Westpac, NAB and ANZ, we think there's a very high chance that they will cut their dividends and actually, yesterday, the Reserve Bank of New Zealand actually announced that New Zealand banks wouldn't be able to pay dividends, which effectively means that the Australian banks that make their earnings in New Zealand won't be able to distribute that part of their earnings.”

Gardner quantifies that dividend cuts across the lenders would likely be 30% and “potentially even higher”.

The silver lining

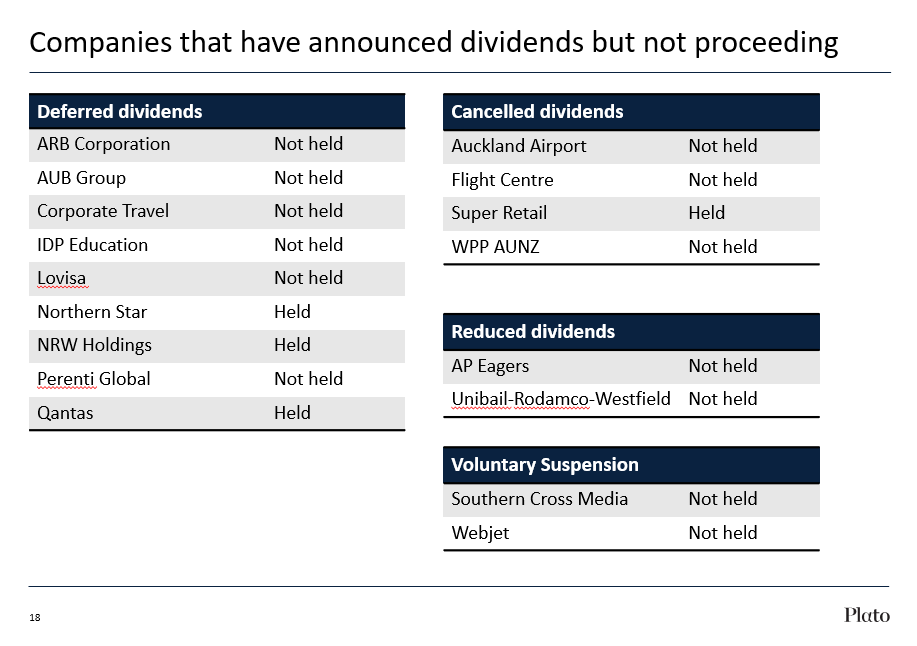

While the expectation of dividend cuts will surely be sombre news for investors in these companies, spare a thought for those at the mid/small-cap end of the spectrum, where more than a dozen well known stocks have decided to defer or cancel dividends that were due to be paid.

“This is the first time that we've actually seen this happen in the Australian market, where companies that have already gone ex dividend are actually deferring the payment in their dividends, or, in some cases, cancelling those dividends, or reducing those dividends. So it's a pretty unprecedented time at the moment.”

Win by not losing

Given many broking platforms and financial services data providers present dividend information on a historical basis, trailing yields can often look too good to be true, The Big Four banks ex-CBA, for example, are all yielding around 10% and even higher when franking credits are taken into account.

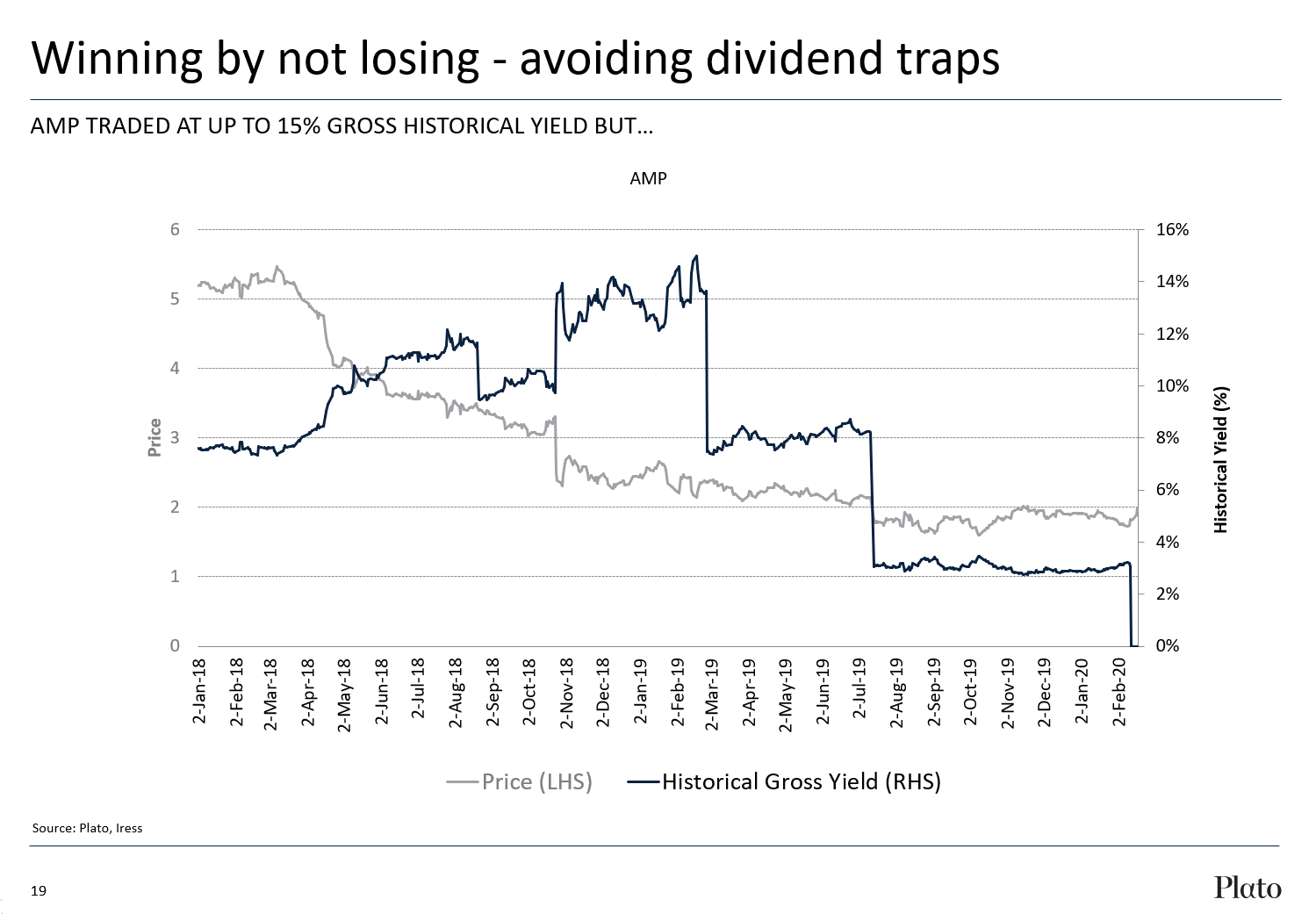

But Gardner warns investors to not be naïve, sharing the example of when investors were seduced by AMP over the last two years.

“If you were kind of a naïve investor that just looked at the historical dividend yield, you would have said, "Wow, AMP's got a yield of 15%. This is an amazing stock." Until it's cut its dividend by about 70% in February 2019, then didn't pay a dividend in August 2019, then again didn't pay a dividend this year this side of February, so you thought you were getting a high yield stock but it turned out the yield you actually received turned out to be zero now.”

Thus, avoiding dividend traps through careful stock selection or considering a specialist strategy might be something for investors to consider given uncertainty around dividends is expected to persist for the next 12-18 months.

Gardner said the way Plato plays income investing is to rotate through stocks to generate yield rather than put companies at risk of dividend cuts/suspensions in the bottom drawer.

“This actually enables us to move into the areas of the market we think are going to have a good relative stock return as well as the ones that are going to get good yield, and we think that's very important in the current market.”

Where to from here?

Hamson summed up the call by predicting that volatility would continue and recessions around the world are unavoidable. Government policies, though, will be very crucial to how long this downturn is and how quickly countries and stocks and industries rebound out of that downturn.

"I think one thing we can say pretty much for sure is that interest rates will remain even lower for longer, so there's no real, I think, likelihood of any interest rate rises around the world for some time."

The good news for income investors will be that dividends will rise again, as they did after the GFC, once COVID-19 passes and the economy is back on track.

Access the full Plato recording here.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under ASIC Regulatory Guide 36, section 66.

3 topics

22 stocks mentioned

1 contributor mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment