Can the housing rally continue?

12 months ago, Australia’s housing market appeared to be spiralling towards a very messy crash. A combination of factors had led to some of the worst falls in housing in decades; tighter credit conditions, negative sentiment from the Royal Commission, and fears about changes that a Labor government would make if it were to gain power. Today, the story couldn’t be more different. Credit conditions have loosened, the Liberals were unexpectedly re-elected, and the Royal Commission is already just a distant memory. The second half of last year saw a staggering turnaround in the market. Double-digit annualised price gains are once again a reality as several rate cuts from the RBA have supercharged the buying demand.

But not everyone is convinced. Due to low wage growth and a sluggish economy, some commentators don’t think the current pace can be maintained. Others think there are further price falls to come.

To get a better understanding of the landscape, I reached out to three experts to get their take on the outlook for the housing market. Responses come from Shane Oliver, AMP Capital; Damien Klassen, Nucleus Wealth; and Jonathan Rochford, Narrow Road Capital.

Spectacular rebound can’t continue

Shane Oliver, AMP Capital

The rebound in home prices since mid-last year has been spectacular. In fact, it’s been so spectacular that some of those who were previously looking for 40% or so falls in prices don’t believe it and think it’s been made up by property spruikers. But there is too much supportive evidence to buy the line it’s been made up! Rising housing finance, rising prices, strong clearance rates and numerous anecdotes of people who have missed out because a property went for $200,000 or so over reserve.

The main drivers of the rebound appear to have been the removal of uncertainty around negative gearing and the capital gains tax discount thanks to the Federal election outcome, earlier and faster RBA rate cuts and regulatory easing. The impact of these unleashed pent up demand from the 2017-19 period of falling prices that has now largely run its course. Prices are likely to continue to increase this year as rates remain low, underlying demand remains high relative to supply and an element of FOMO (or fear of missing out) continues to impact. But the gains are likely to be much slower than the 19% or so annualised pace seen in Sydney and Melbourne through the second half of last year, particularly as the soft economy makes an impact, as affordability is now rapidly deteriorating again and if housing credit growth starts to pick up APRA is likely to step in again to try and cool the property market down. In any case we are unlikely to see a re-run of the easing in lending standards again that saw a big chunk of loans going to interest-only borrowers like we did through the last property boom. As a result, this upswing in prices is likely to ultimately prove to be a lot milder than what was seen over the 2012-17 period.

Housing lacks a solid foundation

Damien Klassen, Nucleus Wealth

The Australian household is the second most indebted in the world. This is a risk. Part of the house price rise has been falling interest rates. Another part has been the loosening of credit standards. A third element has been quality problems in new apartments, resulting in increasing demand for free-standing houses. The final part is pent-up demand from 2018/early 2019 when transactions stopped in anticipation of a Labor government. None of those are a solid foundation upon which to build a sustainable housing boom.

There may well be a further short-term leg up in housing as a buying frenzy seems to have taken hold. If (and it is a big if) COVID-19 doesn't derail the growth.

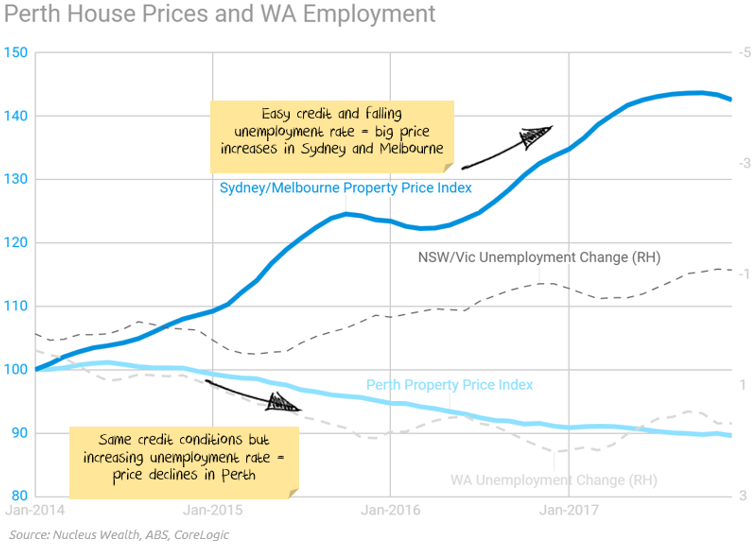

During 2012 to 2017, while interest rates were cut and Sydney/Melbourne house prices boomed, Perth prices fell 10%. This was due to rising unemployment:

In Australia, there are likely to be job losses from:

- a dramatic fall in construction approvals

- tourism losses from bushfires

- tourism losses from China travel bans

- fewer students from China travel bans

- less discretionary expenditure due to lack of consumer confidence from all the above

- a government determined to run only a small deficit

There is a distinct possibility the rest of Australia faces the same effect as Perth.

I assume house prices are limited by:

- the cost of a mortgage relative to the cost of renting

- the cost of a mortgage relative to wages

Rental growth and wage growth are both close to generational lows.

This means the investment outcome is:

- Even in the boom conditions, you are unlikely to make a profit if you borrow most of the money

- In negative scenarios, you are likely to make significant losses.

Can I engineer a case where investors do make money? Sure. But it involves unlikely scenarios where wages and rents increase rapidly while somehow interest rates stay low. Or it involves suggesting that the median home buyer will pay all their post-tax income in interest and prepared to pay interest costs more than double the cost of renting an equivalent house.

The story is not as bad in markets outside of Melbourne and Sydney, but the theme is the same.

Finally, remember that property is not a short-term trade. If you buy today and sell in a year up 10%, you would be lucky to make anything after paying entry and exit costs. Property needs a 5-10-year bullish case for prices to justify the huge upfront and sale costs and the very low rental yields. I find it difficult to come up with one.

Slower growth in house prices ahead

Jonathan Rochford, Narrow Road Capital

The rebound in house prices has been driven by three key factors:

- Positive sentiment after Labor’s proposed tax changes were rejected,

- Lower interest rates, and

- The continued above normal population growth.

The sentiment change and interest rate cuts are unlikely to be repeated and their impact should reduce soon. The extraordinary population growth is set to continue with neither major party willing to consider the negative impacts of this policy. This points to a much slower appreciation in house prices ahead.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for Mining.com.au.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium.

3 topics

3 contributors mentioned

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for Mining.com.au. Patrick was a Market Analyst, Editor, Senior...

Expertise

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for Mining.com.au. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment