10 most tipped small caps: Fundies' deep dives

Alex Cowie

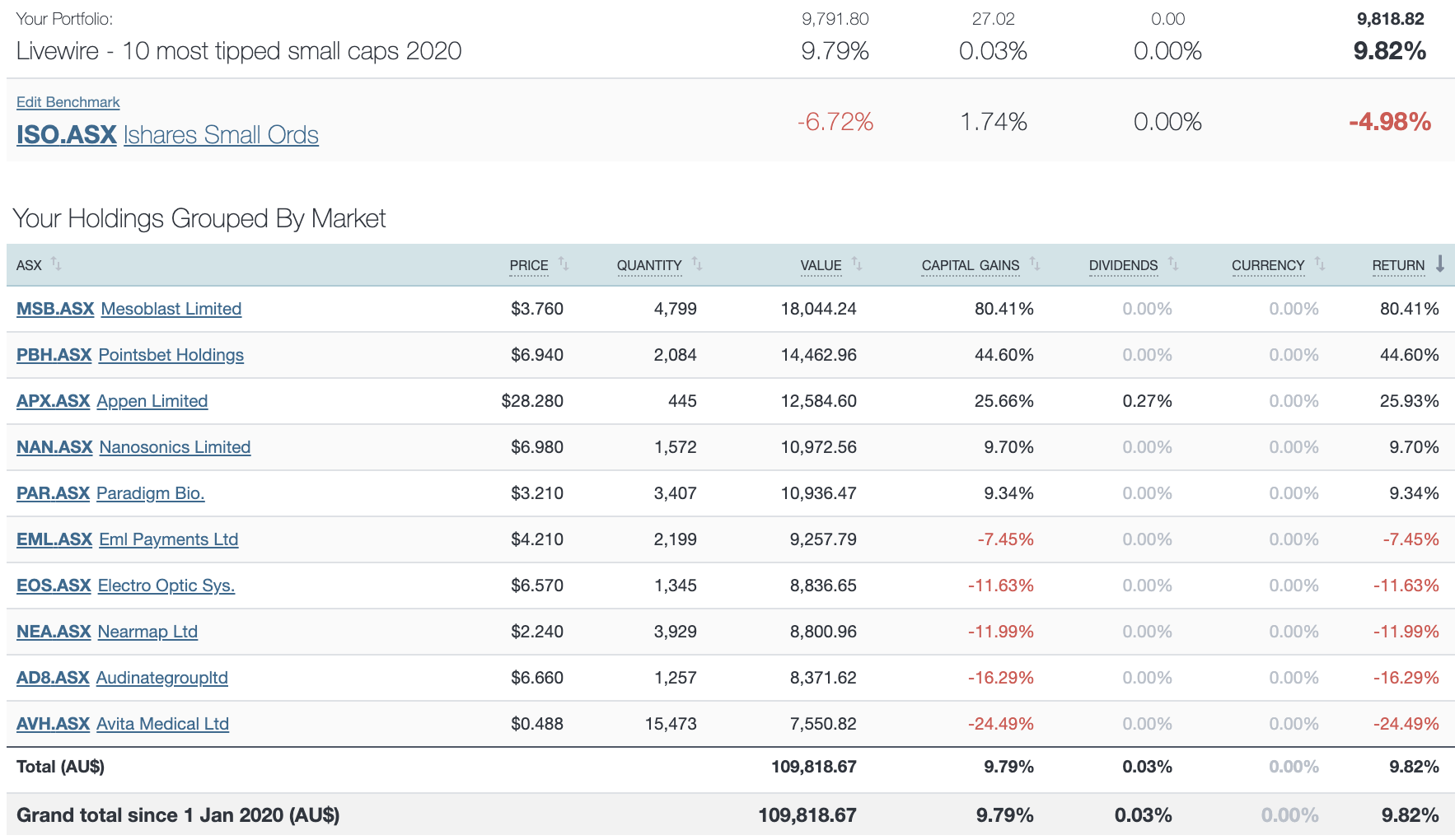

While the ASX200 has bounced by more than 33% from its March lows, the small caps index has now bounced by over 50%. A few weeks ago, I flagged that the ten most tipped small caps had already nudged into the black for the year and that we would be publishing a series of fund manager deep dives for these small caps.

These summaries from the fundies were all excellent and comprise a very useful research tool for anyone venturing down to the small end. In case you missed any of them, I wanted to round them up for you in this wire and highlight some of the points each fund manager made.

As we saw with the most tipped big caps, Livewire readers seem to have once again picked a group of stocks that is significantly ahead of the market. As the table above from our friends at Sharesight shows, the most tipped small caps are a full 15% ahead of the Small Ords so far. So let's see what the fundies think about these stocks...

The investment case for Appen continues to stack up

In his very popular report, James Dougherty from Lennox Capital Partners argued why The investment case for Appen continues to stack up.

Appen's price fell by around a third in the Feb/March COVID-crash, but the ensuing bounce has been impressive, with the stock doubling since then to recently set new all-time highs. James was very positive on the stock's potential, writing that:

Management has proven their execution skills and continues to execute their strategy at an exceptional level, establishing the company as a global leader in AI and machine learning datasets. It’s rare to find a company with a combination of strong management, attractive structural tailwinds and a proven history of growth and execution at a reasonable price, but when we do, we like to be on the long side of the bet. We believe Appen demonstrates these characteristics in spades.

As well as liking Appen, he also likes the industry it is in, saying that AI and machine learning is set to compound at an extraordinary rate over the coming decade, which should provide the company with a long-term tailwind. You can read James' view in full here.

Pointsbet: Betting big

Pointsbet investors have learned the meaning of volatility this year. First, the stock crashed from $6 to $1, which was half the price of last year's IPO, as investors responded to the notion that a sports-betting business requires sports games to bet on. After bottoming, the stock then bounced six-fold to re-test its previous highs.

Dean Fergie from Cyan Investment Management gave his verdict on Pointsbet in 'Pointsbet: Betting big'. He gave a balanced view of the stock, pointing to some of its attractive qualities, but flagging some of the risks as well, not least the capex required to break into the large, fragmented and competitive US market:

Overall, PBH can only be considered a horizon investment proposition. There is no doubt the pathway to profitability appears long, albeit incredibly well-funded with over $150m on the company’s balance sheet. Whilst the business is achieving EBITDA break-even in Australia, the cost of entering the US means the company might need their customer base in the US to increase 10 fold (to 200k) before achieving break-even in that region. With uncertainty around long-term, sustainable win margins, customer acquisition costs and legislative outcomes in new US states, notwithstanding the COVID related uncertainty with respect to the re-starting of global sporting events, PBH is all but impossible to value on fundamental metrics.

As the table above shows, the States of the US are a patchwork of different jurisdictions, all at different stages of legalisation.

Nanosonics: Global leader in infection protection

Is there a better time than a viral pandemic to focus on best practice for sterilisation of medical equipment? Nanosonics has 20% of this global market and has seen its price quickly recover in full from the lows. Katie Hudson at Yarra Capital Management wrote about Nanosonics in our series, saying

The company’s revenue model is compelling. While large inflows from the sale of its devices to hospitals are attractive, from our perspective the real value driver is the recurring consumables revenues which are linked to the daily use of their devices. Nanosonics has a highly scalable manufacturing process, requires little capital for growth, generates very strong free cash flow, and is investing in R&D for growth. With a net cash position, its balance sheet is in great shape at a time when many companies face a funding squeeze. There has probably never been a better time to be a global leader in infection prevention.

Nanosonics was once a nanocap on the ASX trading at $0.20 but has grown steadily to a $7.00 stock with a $2 billion market cap. The stock was one of last year's most tipped small caps as well, finishing up over 140% for the year. It has led the market so far in 2020, and in her wire, Katie argues that there is further upside potential here, and making comparisons to Cochlear, another Australian medical device story with success on the global stage.

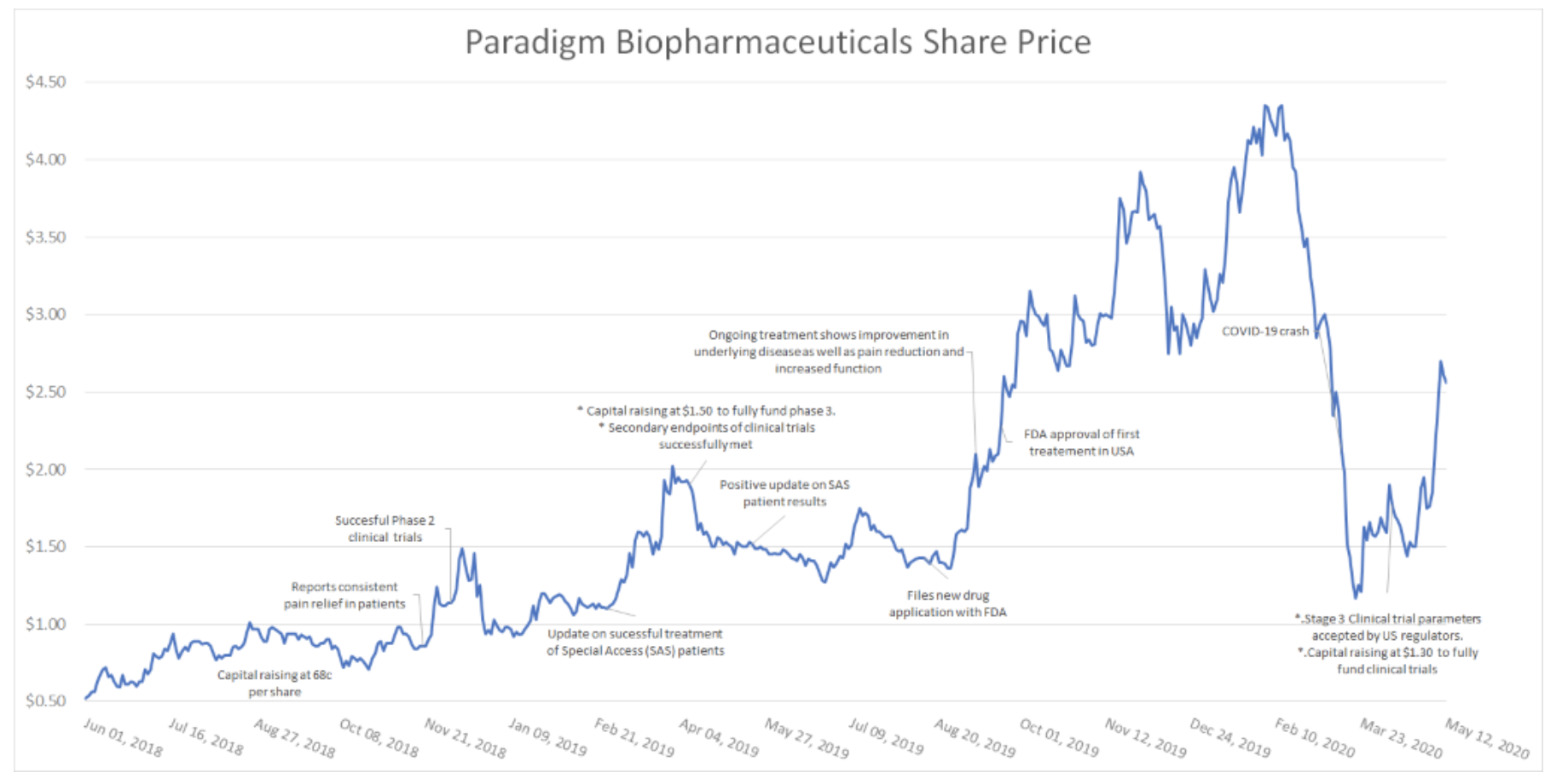

Progress and profile to power paradigm's share price

In his deep dive on $600 million market cap biotech, Paradigm, Michael Goldberg at Collins St Value Fund concludes to say that if the stock achieves even a small part of what they hope to, it may have a place in the ASX50 over the next couple of years. Given the smallest stock in the ASX50 has a market cap of around $6 billion, he clearly has high expectations. As he wrote in the wire:

Paradigm Biopharmaceuticals (PAR.ASX) have $108M in cash, no debt and are well advanced in the progression of clinical trials in addressable markets worth up to as much as $36B p.a. The next two years are particularly exciting for Paradigm Biopharmaceuticals as they are set to announce on five key developmental milestones. Each of those pieces of news could drive significantly more interest in the company, and result in a materially higher share price.

The headline of his wire, EPS of $20 by 2025, also suggests how bullish he is on the stock. His wire gives a good account of how well positioned it is, and the potential catalysts ahead.

Strong outlook for EML in a post-COVID world

The need for the digitisation of payment processes has been highlighted during the crisis, and this plays directly into EML’s hands as it is a payment processing company with a difference, in that it provides a payment gateway that can be highly customised to the needs of the client.

The stock was by far the most popular small-cap in our survey, taking 175 (2.5%) of all tips, and had a stellar 2019 with the price more than tripling. This year so far, it is only slightly ahead of the index.

Shane Fitzgerald at Monash Investors has provided a good overview of the stock in his wire, arguing that it has a strong outlook in a post-COVID-19 world, summarising to say that:

One of the big drivers of EML’s growth over time has been the desire for its corporates to move away from paper-based systems and towards more efficient card-based systems. Now there is a desire to move towards fully mobile-based systems where the gift card is loaded directly into an Apple Wallet or Samsung Pay or similar. The fully mobile payment solution that EML offers is now a must-have rather than a nice to have, and explains EML’s strong pipeline.

Nearmap: Focused on scaling up

After gaining a cheeky 100-fold between mid-2012 and mid-2019, Nearmap has struggled since then. The stock was one of the most tipped in 2019, but even with a 69% gain over the year, was at the back of the pack (Avita led the pack with a 690% gain). So far in 2020, it has lagged the market.

Focused on scaling up and gave a balanced view of the company's opportunities and risks, writing that:

Nearmap provides cloud-based aerial imagery as a service. We are optimistic that it will deliver strong returns over a three-year horizon as customers continue to seek best-in-breed imagery solutions. We are confident that industry growth, an increasing market share and modest customer churn will drive attractive revenue growth over a three-year time-frame. Moreover, we expect NEA to deliver strong operating leverage and margin expansion as it scales up, enabling it to achieve self-funded growth and giving it the opportunity to accelerate organic growth by reinvesting at high incremental rates of return.

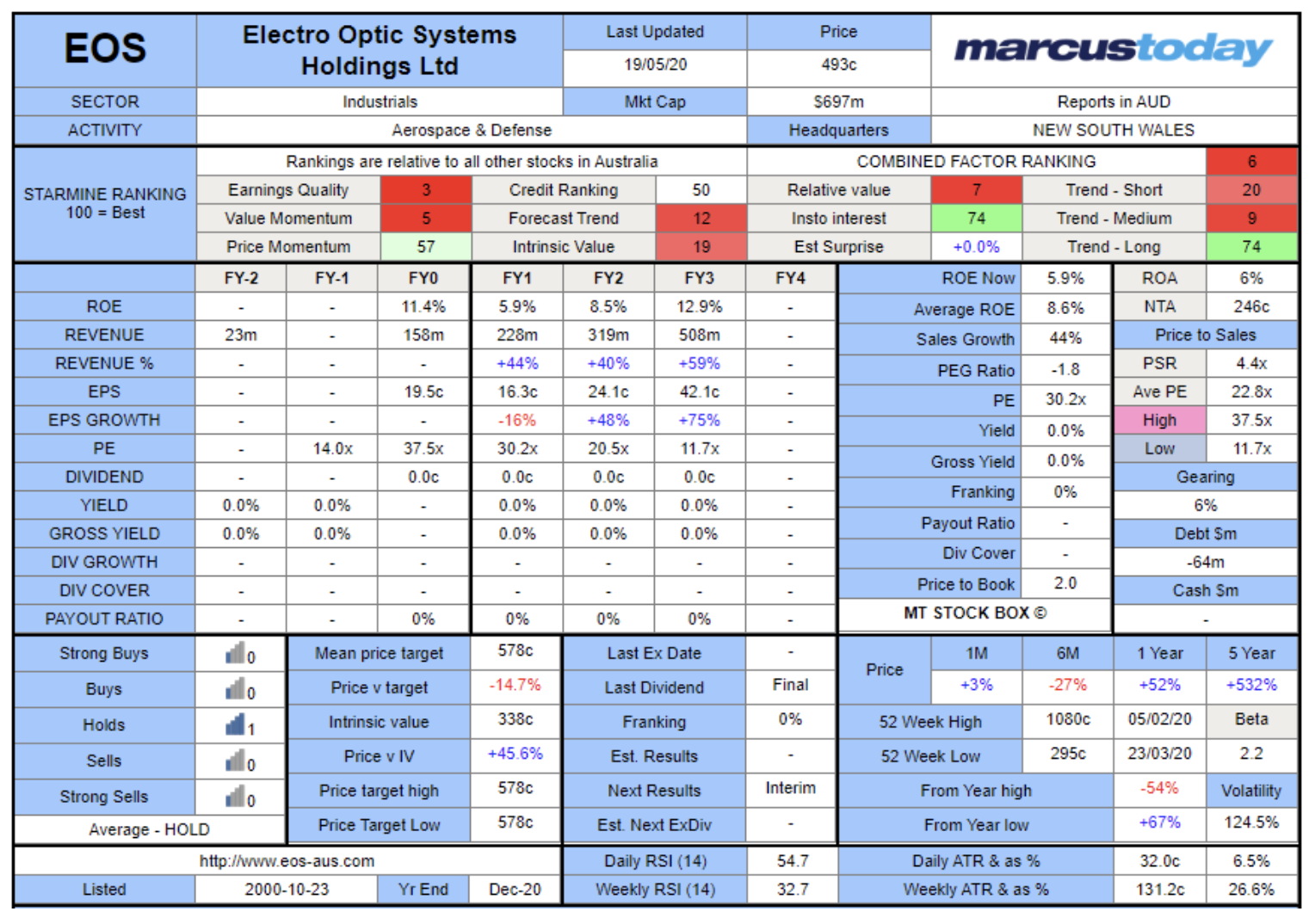

Electro Optic Systems – One to put in your sights

Electro Optic Systems is another stock that had a huge 2019, tripling in price, but is now trailing the market so far this year. Henry Jennings at Marcus Today covered this one, calling it is one to keep in your sights, suggesting a recent capital raise could be part of the reason the price has struggled. Longer-term he is positive on the stock, concluding to say:

It is not expensive looking out beyond the current disruptions. Good technology and US-based manufacturing coming on stream mid-year and exposed to a sector that is relatively immune from spending cuts although UAE and other Middle East contracts may see issues as oil prices remain at subdued levels. Speculative Buy for recovery with the defense sector delivery and payments. The US manufacturing operation could be a catalyst for a rerating. The balance sheet has been improved, now just a question of timing. Potentially some short-term indigestion from recent capital raise.

What COVID-19 means for Avita Medical

Avita produces a medical device called RECELL which produces a “suspension” of spray-on skin cells using a small sample of the patient’s own skin to help treat burn patients and skin defects.

Joseph Kim at Montgomery Investment Management first published his view the stock on Livewire a year ago, and kindly updated his view for this series in What COVID-19 means for Avita Medical.

The stock had an incredible run up in 2018 and 2019 but is at the back of the pack this year. Joseph has provided a balanced view of the stock in his wire.

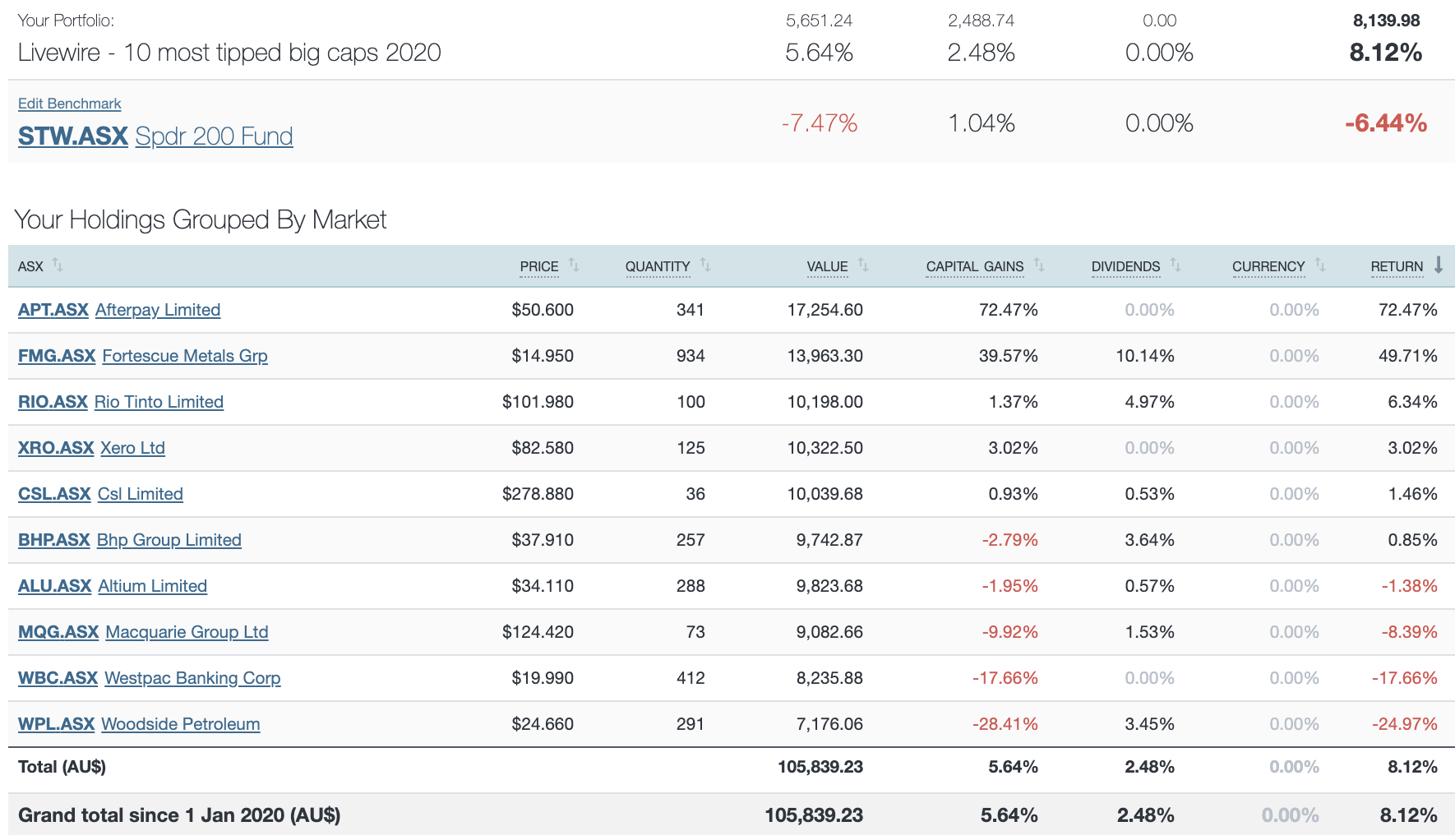

10 most tipped big caps

We recently provided a similar wrap of the ten most tipped big caps from our survey. If you missed it, you can access that by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Alex Cowie,

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

11 stocks mentioned

7 contributors mentioned

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Comments

Comments

Sign In or Join Free to comment