Bulls, Bears, and ‘I don’t cares’

Following the falls in equity markets globally across October and November, there’s been a marked increase in bearish commentary from fund manager, analysts, and various other commentators. But as the saying goes, there’s two sides to every trade, and this is no exception. To balance out the panicked shouts, there’ve been plenty of high performing fund managers calling for calm. Some because they’re not interested in the macro picture, and others because they don’t think the current environment is concerning. I don’t intend on telling you who’s right or who’s wrong; I’m no arbiter of truth, nor can I predict the future. Instead, I’ve collected and summarized the views of some of the best in the business to help you decide for yourself.

The bull case

The bulls are generally a bit quieter at the moment, but there are still plenty of them around if you’re looking for them.

Mary Manning, Portfolio Manager for Ellerston Asia, thinks we’re unlikely to see a major bear market like the GFC or the Tech Wreck.

“My view is that this is not one of the big corrections. This is not GFC 2.0, this is definitely not an Asian crisis. We have checklists, we go through the bear market checklist and if you look at some of these big corrections like the Asian crisis or Tech Wreck, there are a lot of things that characterise the markets prior to these big corrections.

For example, there were extreme valuations, there was certain corporate behaviour, like IPOs and lots of M&A, the sentiment was euphoric – it was all ‘love’ and nobody thought about risk. Cash levels were very low, balance sheets or corporates were stretched. We have a checklist of 10 things, when you go through them, the market right now is not checking a lot of those things. To me, this seems more like a taper tantrum plus a trade war sort of correction. Which means, in my view, we’re closer to the floor than we are to the ceiling in this correction.”

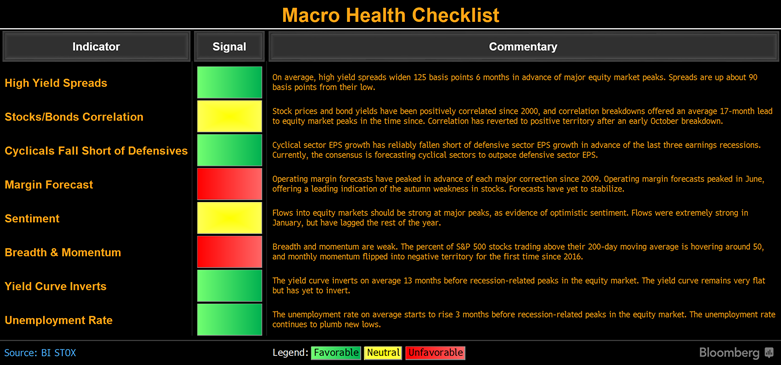

Gina Martin Adams, formerly Managing Director and Equity Strategist at Wells Fargo, and now Chief Equity Strategist at Bloomberg LP, is not quite so quick to say we’re near the bottom, but still only sees two “unfavourable” items on her checklist of eight. Currently the unemployment rate, yield curve, cyclicals vs defensives, and high yield spreads all remain positives for the equity markets.

Source: Bloomberg

Paul Taylor, Head of Australian Equities at Fidelity International, is pretty sanguine about the Australian market and economy. Despite fears of a housing-led recession, he says “there doesn’t appear to be any short-term catalysts that would cause a major market downturn.” While he acknowledges the trade war is a concern, he says that “it’s unlikely however this would cause a major downturn in its own right.”

Importantly, he sees good relative and absolute value in the Australian share market:

“While the Australian equity market appears good absolute value, it’s a stand-out in terms of relative value against other asset classes such as cash and bonds due to earnings and dividend yield.”

The bear case

The bears have been loud, grizzly, and numerous since October. Whether or not they’re right remains to be seen. It’s only with the benefit of hindsight that we’ll know for certain.

Geoff Wilson AO, Chairman and Chief Investment Officer at Wilson Asset Management, is one of the most recognisable people in Australian funds management. His reasoning is fairly straight forward:

Quantitative Easing and record-low interest rates have driven valuations to high levels. This tailwind is now over. Quantitative Tightening (the reduction of central banks’ balance sheets) began in October.

Charlie Jamieson, Chief Investment Officer at Jamieson Coote Bonds, doesn’t pull his punches. If you’ve read or watched any of his commentary on Livewire recently, you’d see that he’s firmly of the belief that things are getting very rough in credit markets.

Though Charlie doesn’t comment on equities, in my view, it’s hard imagine a situation where a major dislocation in credit markets coincides with rallying equity markets.

“Credit is smouldering right now. When that smoke becomes fire, the door becomes a key hole and only the first few get through. The rest get burnt. Holding credit risks with your equity holdings into 2019 and 2020 seems mighty dangerous.”

Rudi Filapek-Vandyck from FNArena is firmly focused on the equities markets, and appears to be similarly bearish.

“Today's equity markets are increasingly showcasing the main characteristics of a bear market.”

Rudi is adept at reading market sentiment, and what he’s reading doesn’t instil confidence.

“Trading activity inside the Australian share market very much resembles that of a genuine bear market. Bad news is being punished without recourse. Good news might trigger a share price rally, but that subsequently becomes a source for taking profits and raising more cash. No news can mean anything, but most likely the stock is being sold off on flimsy correlations and spurious projections.

On some days, nothing really matters. If your stock is listed, and widely owned, it will be sold, simply because other shares are too. No room for exceptions.”

Dr Jerome Lander from Procapital is an asset allocation specialist. This essentially means that he advises institutions, financial planning firms, and wealth management firms on which asset classes and fund managers to invest in. His current views seem to suggest that being overweight equity risk is a dangerous place to be, and advocates for cash and alternative investments.

“There is (arguably of course) a bubble in nearly every mainstream asset class. A bubble in debt markets, a bubble in property, a bubble in equity, a bubble in private assets, and a bubble in the way portfolios are managed. This is an artificially created result of easy monetary and fiscal policies that have been employed by global governments for many years now in an effort to boost asset prices (successfully). These policies appear unsustainable in the long term.

…

Unfortunately, we are probably already in a long overdue equity and credit bear market in the US – and if not - there is a large probability of it not being that far away (within a year or two). We are almost certainly in a bear market in Sydney and Melbourne residential real estate! We define a bear market simply as one which is more likely to lose you money (in real terms) than make it.”

The “I don’t care” case

Humans, both individually and collectively, are pretty bad at predicting the future.

“It’s Difficult to Make Predictions, Especially About the Future”

Versions of this quote have been attributed to Yogi Berra, Neils Bohr, Mark Twain, and many others. Regardless of its source, it emphasises a fundamental truth about the world we live in: it’s more complex than our minds could ever hope to fully grasp. With this in mind, there have been plenty of people calling for calm, not necessarily because they think the markets will be fine, but instead because they accept that they can’t predict them and therefore shouldn’t try.

John Garrett, Managing Director at Moelis Australia and author of MastersInvest.com says that long-term investors probably shouldn’t be too concerned about the current noise.

“It’s more than likely the world will continue to move ahead, and October’s sell-off will be a blip in a long-term chart that moves from the bottom left to the top right. That’s been the trend over the long term and it is likely to be the trend in the future too.

You needn’t worry about short-term blips if you maintain a long-term view, provided you buy high-quality companies and don’t pay lofty multiples for them. These are companies with strong balance sheets, widening moats, high returns on equity and track records of profitability.”

Aaron Binsted, Portfolio Manager at Lazard Asset Management, says that timing the markets is “almost impossible”, and reminds investors that some of the biggest up-days occur in the midst of market turbulence.

"When market and economic environments are less certain, investor return expectations can become difficult to manage. Individuals in such periods can make quick, impulsive decisions based largely on emotions and leave the equity market at the wrong time.

Equities can still play a key role in volatile markets. Successfully timing the equity markets is almost impossible. Many studies have shown that just missing the five best days in equity markets over a year will have a dramatic impact on your overall return. In addition, history shows that many of the biggest one-day upswings occur in the midst of turbulence.

We argue investors need a long-term equity allocation for inflation protection and growth opportunities. Traditional options, like term deposits, bonds, and residential property do not offer enough income to keep pace with cost of living pressures. Equities can over the long-run make a much more attractive source of income.”

Warren Buffett is a man that needs no introduction, but it would be remiss of me to talk about ignoring the macro noise without including a Buffett quote.

"We look at opportunities, as they come along, we try to figure whether we can understand the long term economic prospects of the business. A lot of times the answer is no, then we forget it. We are not making any judgment about where the market is going or we are not looking at any macro factors.

My partner Charlie Munger and I have been working together now 55 years. We've talked about every business you can imagine and stocks. We have never had one decision that involved a macro factor. It just doesn't come up."

In conclusion

There’s no real right or wrong answer here, or at least not one that can be seen without hindsight. As always, it’s important to understand your own strategy and approach to investing and stick with what you know. A clear, well defined strategy (ideally, in writing) can be a valuable tool when the going gets tough.

Let us know in the comments what your views are; do you fall into one of these three camps, or is there another point of view that we haven’t covered?

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium,.

4 topics

9 contributors mentioned

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment