10 most tipped big caps: Fundies’ analysis

On 13 May, we published a quick update on the progress of the ‘Most tipped big caps’, the 10 stocks that got the most votes in our reader survey at the start of the year. At the time the stocks had an impressive 13.6% lead on the market.

With August reporting season done and dusted, and the market having had more time to digest everything COVID, surely that gap would narrow given the ASX 200 is meant to be a highly efficient universe?

But that’s not how things are panning out. Livewire readers’ 10 most tipped big caps are putting the pedal to the metal, with this iron ore and technology-laden beast now trucking ahead by a whopping 29% of the benchmark. What’s interesting is that not only is this portfolio delivering blockbuster capital gains, but with a yield of nearly 5% it’s been a surprising haven for dividend investors as well.

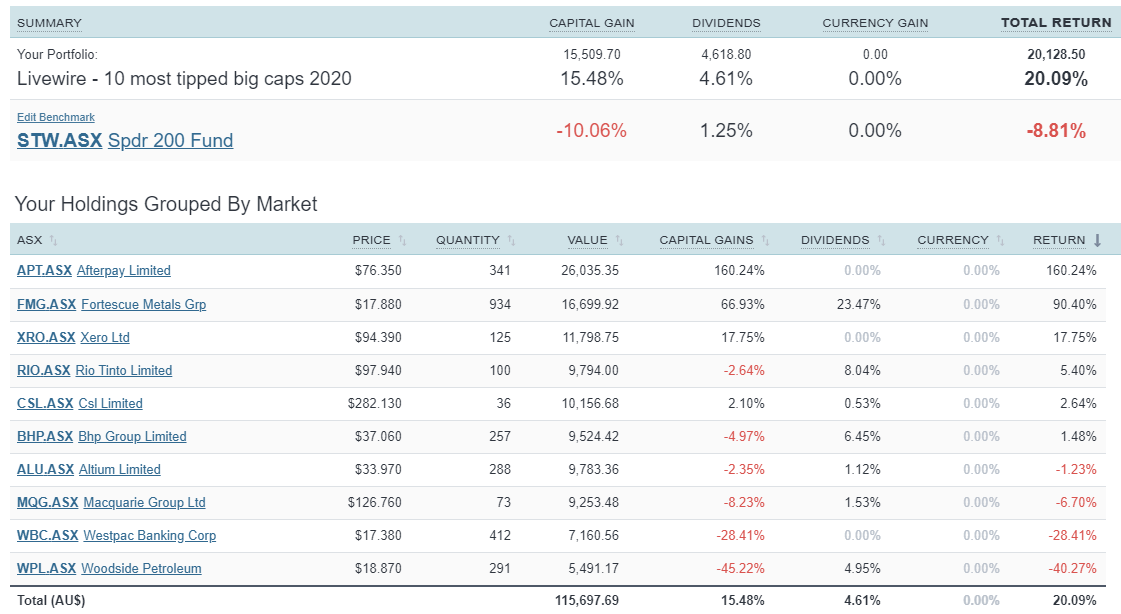

Our friends at Sharesight have kindly provided the performance of these stocks as at 7 September 2020. The portfolio is up 20.09% on an absolute basis, with six stocks in the black.

Click to enlarge the image.

source: sharesight

In this wire, I break down the performance of the 10 most tipped big caps and synthesise the excellent analysis from the fundies who have recently covered these stocks.

1. Afterpay (+160%)

Obviously, different views are what makes the market, but no stock is more divisive right now than the buy now-pay later juggernaut Afterpay. Even with the recent tech sell-off, the ASX darling has put on a sizzling 160% this year alone.

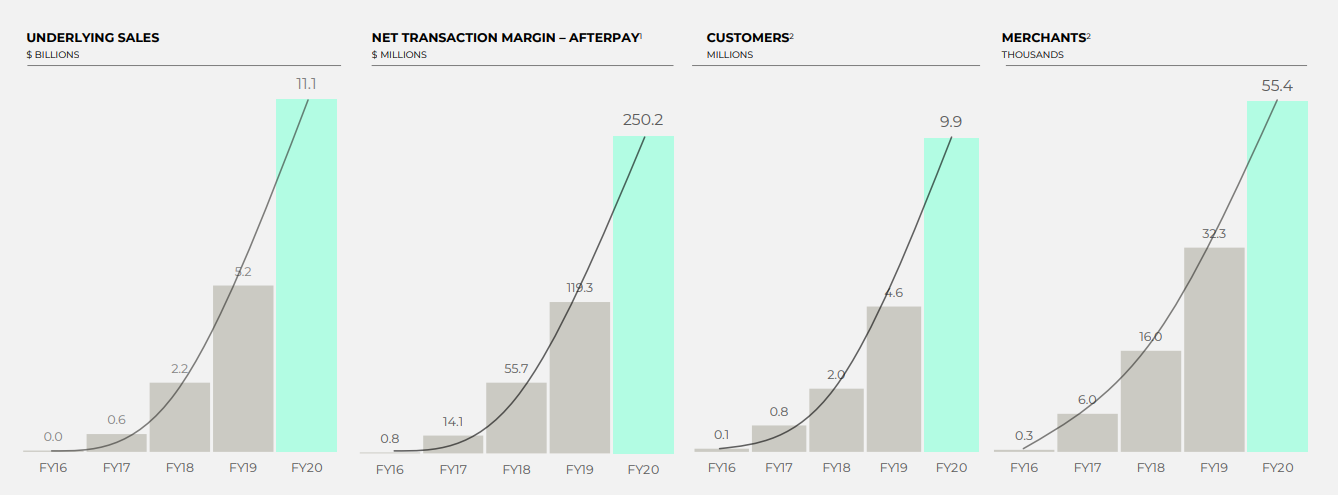

For Simon Shields at Monash Investors Limited, Afterpay’s full-year results validate the attractiveness and acceptance of its offering from both merchants and consumers, with key underlying business metrics firing on all cylinders (see chart below).

source: afterpay august 2020 results

Looking ahead, the key challenge for co-founders Nick Molnar and Anthony Eisen will be in replicating Afterpay’s success across more offshore markets. Simon has conviction that the company will be able to execute in the newly announced frontiers of Europe and Asia.

“That business in Europe has got to be worth $10s of dollars to the share price, even if they only do half as well as in the United States. Now we see them going to Asia ... you wouldn't say that the Asian opportunity in the near term is going to be anywhere near as big as the European or United States opportunity, but it's still a significant value add to the business.”

But Dean Fergie of Cyan Investment Partners, who invested in the IPO and sold out at $35 last year, reckons investors are in for a “perfect storm” if Afterpay doesn’t keep up the raging growth to justify its astronomical valuation, adding that the business model is still unproven.

“The business still hasn't been completely proven yet. The business is not making money at the bottom line. Sure, their profit numbers look great, but the EBITDA is still marginal at $35 million. A $25-$30 billion-dollar business, should be at the minimum at some stage, making $500 million after-tax. It's a long, long way from that at the moment. Lastly, there's a lot of merit to it but this business and its share price performance will live or die on how deeply and profitably they can penetrate the US market. That's all it's about.”

Both Simon and Dean expand on their views in Afterpay: Boom or Bust?

2. Fortescue Metals Group (+90%)

Fortescue Metals Group’s ore-some performance has continued, with the stock now up 90% this year. What’s almost mind-boggling to comprehend is that about 24% of that return is from dividends and franking credits.

Courtesy of elevated iron ore prices and impeccable execution, Fortescue has splashed US$3.7 billion in capital returns, and Stephane Andre from Alphinity Investment Management reckons the party isn’t over just yet in the wire While iron ore prices are high, Fortescue has more cards up its sleeve.

“… the demand in China keeps surprising on the upside, swallowing every tonne available and keeping the market tight. I believe it is likely to stay tight for a while, possibly for another 6 to 12 months, as there are no new sources of supply in the short to medium term. Demand will most likely stay robust in China and will also lift in COVID-affected countries like Japan, Korea and Taiwan. If that turns out to be the case, current market expectations of $75-80/t for 2021 versus the spot price of $125/t appears far too low, and FMG’s future earnings and cash flows will keep surprising significantly on the upside.”

3. Xero (+18%)

The Internet of Things thematic is gaining prominence and lifting data centre as well as software stocks. Xero has already advanced 18% this year. But amid general concern about tech valuations, James Gerrish of Market Matters last month rightly asked the question in the headline of his wire: Should we keep chasing cloud stocks? In that piece, James called out Megaport, NextDC, and Xero as ways Australian investors can access the cloud theme, though there could be a pullback in some of those names.

“New Zealand cloud-based accounting platform provider XRO is expanding rapidly into the likes of the US, UK and South East Asia. We like XRO over the medium-term seeing upside in their expansion while excellent client retention is both encouraging and vital. Competition remains in the form of MYOB but XRO appears to have the number on its rival.”

That being said, he reckons the stock is unlikely to move too far before it reports in November.

4. Rio Tinto (+5.40%)

As Michelle Lopez of Aberdeen Standard Investments concluded in her earnings season summary That's a wrap folks, the major miners have all shared the spoils from high iron ore prices.

"Strong results given resilient commodity prices, but broadly in-line with expectations. The bulks BHP, Rio Tinto and Fortescue all benefited from elevated iron ore prices. This is a sector of the market which is delivering attractive returns; dividend yields are well above market average and the expectations that elevated returns will remain in the near term given the high iron ore price."

5. CSL (+2.64%)

David Moberley from Paradice Investment Management pointed out in this excellent wire, Why CSL is cheaper than you think, that investors are far too fixated on the biotech giant’s current multiple whilst underappreciating the potential and mechanics of its nearly $1 billion in annual research & development expenditure.

“There's clearly a huge amount of value in that pipeline and I think the way we prefer to look at a business is to value each of the separate businesses individually and then we actually add on a component to that R&D pipeline. Given they are a dominant global leader with great scale advantages, strong growth outlook and an under-geared balance sheet, I can't see why the stock wouldn't continue to trade at a significant premium to the market.”

I'd strongly recommend reading the part of the wire where David mentions why he’s closely watching the CSL-112 to trial, which could lead to a “potentially company changing drug”.

6. BHP (+1.48%)

John Ayoub from Wilson Asset Management in the wire BHP: Continued demand to drive dividends and buybacks points out something every investor in the Big Australian should know. While in the short to medium-term, higher commodity prices will support ongoing capital returns, management are casting their eye towards “future metals” to propel long-term performance.

“The shape of the company is very much geared towards future metals – metals that will demonstrate above-system growth for the next three, five, 10 years. Additionally, you'll start seeing consolidation of the overall portfolios. You'll see a few more divestments, more organic growth. They'll be looking to do more exploration and finding new assets that way.”

7. Altium (-1.23%)

Long-time Altium holder Ben Clark of TMS Capital provided quality insights into how the tech stock is positioning itself for the next five years in Beneath the numbers, the Altium story just keeps getting better.

Ben points out that the company’s “game-changing” Altium 365 software package, launched at the tail end of FY 2020, has already seen strong take-up from customers.

“The other interesting part is that they are going to change their pricing approach – they are hoping over time to move 365 subscribers from a perpetual license fee to a SaaS-based model. That’s going to increase Altium’s quality of earnings and so their earnings base, which is 60% recurring, should increase. In turn, that should also make the software more attainable for smaller businesses.”

Ben goes on to discuss three other big things the market is overlooking when it comes to Altium.

8. Macquarie Group (-6.70%)

While Macquarie Group reports full-year results on 4 November, Matt Williams from Airlie Funds Management provided an update in late July to affirm his long-term thesis on the investment bank.

In his wire, Macquarie better braced for these difficult times than it was during the GFC, Matt says Macquarie has done a stellar job in shifting from a business model reliant on short-term funding to one with firmer capital and funding underpinnings. Today about two-thirds of Macquarie’s earnings is generated from its annuity-style businesses (funds management and banking and wealth products) that produce recurring revenue year in, year out.

“We are attracted to Macquarie’s superior capital allocation and its proven ability to adapt and shift its business mix according to market conditions. This is not an easy achievement and reflects the unique culture and operating system that has developed over the past 30 years. The result? Higher returns and higher earnings growth versus its financial sector peers – Macquarie delivered an average of 10% earnings growth over the past ten years, a superior return on equity, without excessive leverage.”

In the wire, Matt also shows some great graphs on Macquarie’s impressive profit growth since 2010, how the asset-management business is leveraged to two strong structural growth stories (namely, demand for infrastructure and renewable energy), and MQG’s attractive valuation relative to peers.

9. Westpac (-28.41%)

It’s no surprise to find Westpac among the laggards. COVID-19 has smashed banks’ share prices and their dividends; APRA itself demanded lenders take a conservative approach regarding capital management due to the high level of economic uncertainty. But Dr Don Hamson of Plato Investment Management in his wire Dividends hiding in plain sight highlights that Westpac has been the laggard among the Big Four, given the other lenders opted to at least pay an interim dividend.

"Westpac was a bit of a laggard amongst the big fours because ANZ did announce a dividend in the end, but Westpac decided to not even pay an interim dividend at all, remembering that it also has that AUSTRAC fine outstanding. Its earnings were actually probably the biggest disappointment, but I would say that Westpac seems to have conservatively provided large provisions against future debts. So I think it's a bit of a sandbagging by the new CEO there.”

10. Woodside Energy (-40.27%)

COVID-19 came just as hopes were building that Woodside’s share price would break out of stagnation. Unfortunately, Woodside is the biggest loser on the list, with its share price down more than 40% year-to-date.

But Romano Sala Tenna and Hendrik Bothma of Katana Asset Management see an opportunity. Given the prospect for oil demand to rise as economies reopen and Woodside’s growth optionality, Romano and Hendrik - in With Woodside down 40%, is it time to get greedy? – reckon the company makes a quality recovery play trading at a great discount.

“What attracts us to WPL in the large-cap energy basket is the strength of their balance sheet which management improved during 1H2020. Gearing has fallen below 20% and liquidity has been increased to US$7.5bn. They are the least levered to the oil price and have a clear focus on rewarding shareholders by maintaining an 80% payout ratio, which is well above their policy minimum of 50%. They also have an ambitious pipeline of growth opportunities which offer catalysts to the current price including acquiring Chevron’s 16.7% stake in the North West Shelf and Cairn’s 40% stake in the Sangomar project.”

Reporting season webinar

To round out reporting season, Livewire will be hosting an exclusive webinar for our subscribers. Join Bella Kidman, and two equity managers on September 15 as they discuss the highlights of reporting season for both the big caps and the small caps. You can register for the webinar here. Register now to ensure a spot as the webinar will be open to 500 Livewire readers only.

Again, a big thanks to our readers, fundies and Sharesight for their input in bringing to life our most-tipped updates. Please give this wire a like if you'd like to see more updates and commentary on the most tipped stocks from our fundies.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

3 topics

10 stocks mentioned

13 contributors mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment