The biggest winners and losers of reporting season

Alex Cowie

Reporting season is over and saw share prices of more than 40 stocks jump (or fall) by over 10% on the day of their results, with at least 10 moving by over 20%. The biggest gainer, Webjet, was up 30.6% on the day, a remarkable move for what was at the time a $1.5 billion stock.

However, despite these significant moves, many of the stocks have kept trending in the days since they announced, with Webjet now up more than 37% from its results.

Livewire published on-the-day fund manager commentary on results through reporting season, and in this wire, we look at what the fundies are saying about those stocks that moved the most, both up and down. Because as we discuss here, these moves could play out for several months yet...

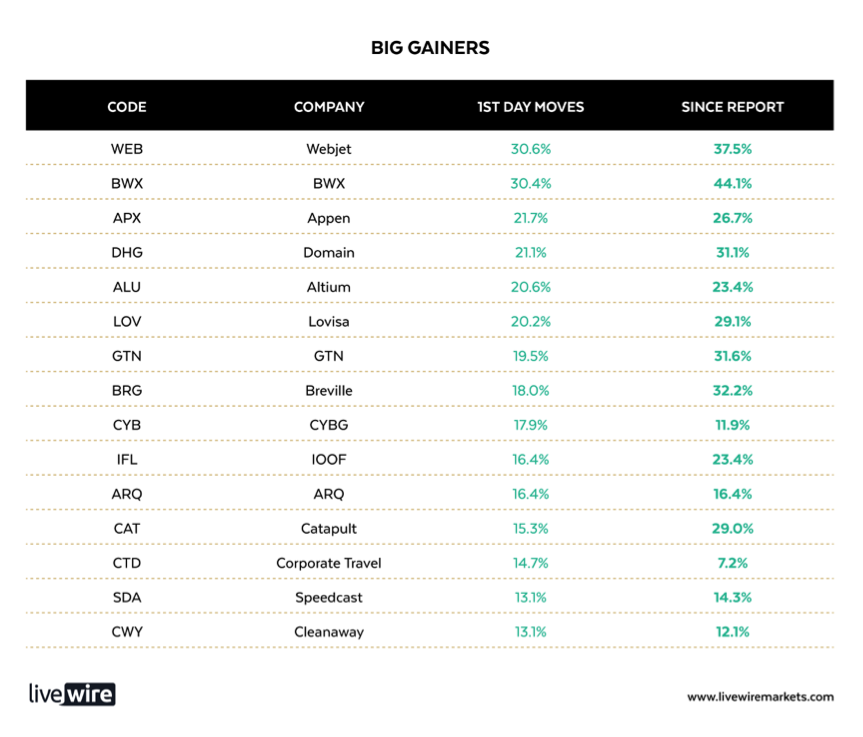

The biggest jumps of reporting season

This table shows the 15 biggest one-day share price jumps this February, next to their total current gain since reporting (as of 2pm 28th Feb).

Source: Data from Richard Coppleson / IRESS

A quick eyeball down the 1st day move’ column versus the ‘Since report’ column quickly shows that most of the stocks that jumped on day have kept trending since then.

In fact, at the time of writing, the additional gain (from end of day 1 to now) is an additional 4.4%. In comparison, the ASX200 has gained a little over 1% over the 2 weeks that most of this group reported.

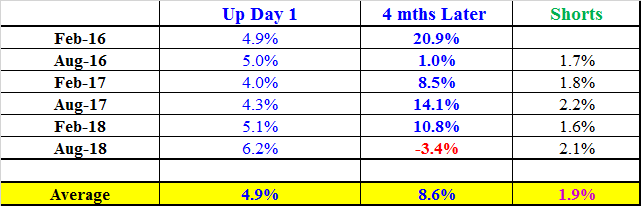

This phenomenon, ‘Post Earnings Announcement Drift’, is the topic of several academic papers, and is cited as one of the biggest counter-arguments to Efficient Markets Hypothesis. The sheer volume and concentration of company reports makes a farce of the idea that the information is transmitted efficiently around the market. There is simply too little time and too much data, and the professionals analysing the deluge of information have often had too little sleep and too much coffee.

Post Earnings Announcement Drift is certainly not contained to the first few weeks either. This goes on for months as the data is fully digested, the nuances in the fine print are spotted, and the post-results road shows are completed.

Richard Coppleson, Director of Institutional Sales and Trading at Bell Potter, who kindly provided the one-day move data above, has been reviewing this data for a few years, and recently published a wire summarizing his findings. By his calculations, the trend goes on for as much as four months after results.

This would suggest that there could still be money on the table in sifting through the big movers. We had around 30 responses in our series, and you can access the full list here.

However, in this wire, I have shortlisted the biggest movers from our list and pulled out key points for each, with links to the full wire.

to provide some sell-side perspective, I have added extracts from the reporting season monitor based on broker ratings, kindly made available by Rudi Filapek-Vandyck at FNArena, and you can access the full listing here.

The big gainers

I have reviewed the price data for this group, both on the day of the result, and then in the days following, Post Earnings Announcement Drift is apparent here too, particularly among the stocks with the largest moves, both up and down.

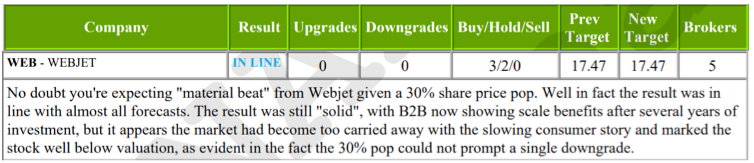

Webjet (WEB) was the standout gainer with a 30.6% move. Naheed Rahman from Flinders Investment Partners had previously flagged this stock on Livewire as one to watch, and wrote about it again for us right the latest result. He is very positive on the stock’s prospects, and even after the jump thought the stock was still cheap, writing:

“Despite the +30% move in the share price on the day, on our numbers, WEB is trading on a PE of 14x FY20. At the very minimum, putting the company on the average small cap industrial multiple (conservative given the quality and growth attributes of the company) yields a valuation close to $20/s, a +30% expected return from here”.

FNArena reporting season monitor summary:

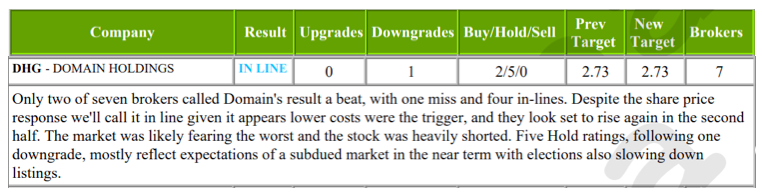

Domain (DHG) was another one of the >20% movers we had commentary on , jumping 21% on day one, and is now up by over 30%. Chris Prunty at QVG covered the stock’s result in ‘Pain in the domain’, however is not convinced the stock’s fundamentals support the price action, writing that:

"It’s not hard to dream the dream on Domain. Bulls cite strong cash flows, potential for margin improvement and geographic expansion and high barriers to entry. The bears say earnings estimates are too high, any geographic expansion will require investment and Domain is a long way behind their more geographically diverse major competitor; REA Group. Domain claims listing parity in many markets but needs to close the gap in audience and leads to get agents to pay up. Nine Entertainment’s almost 60% stake in Domain gives them every incentive to help them do this. On the audience front, Domain has already started to feature more prominently across Nine’s TV and Newspaper assets. Closing the revenue gap with REA will be harder. In our experience changing a sales culture is not easy. This, the cyclical downturn in listing volumes, and a lack of obvious valuation support keeps us on the sidelines."

FNArena reporting season monitor summary:

Ben Clark from TMS Capital discussed Altium (ALU), which gained 20% on day one, and has so far crept higher to be up 22%. This stock has now increased by more than 400 times from its low during what looks like some very unfortunate tax-loss selling in late June 2011. This stock just keeps on cranking and keeps defying its many critics. Ben made a compelling case for it in his wire, writing in Altium: Exceeding consensus forecasts again:

"Ever since we’ve owned Altium the one thing I’ve really noticed is how divisive the stock it is amongst institutional investors. This is a $3.5bn company yet less than 4% of the register are Australian active managers. Although it feels like many have admired its efforts from the sidelines few can bring themselves to pay the high earnings multiple the company has consistently traded on. This goes back to the ongoing debate we’ve all been reading about – what price do you pay for growth. My view from here is that if Altium hit their 2025 newly installed revenue target you will make very strong returns from this point. On the way however it will continue to see the volatility that’s surrounded it for the last five years. Look through the share price volatility and focus on the earnings trajectory is my advice; it's served us well to date.

Lovisa (LOV) has been something of a quiet achiever - how many other retailers have gained 400% in the last 3 years? The result certainly didn’t get as much airplay in comparison to some of these other big movers, yet the numbers looked good and the stock jumped 20% on day one, to be up by 30% now. Shane Fitzgerald at Monash Investors Limited covered this one in ‘Lovisa remains an attractive investment’ concluding to say that:

“With the stock trading on a PE in the 22-23x range given the strength of its earnings outlook, it remains an attractive investment.”

Corporate Travel (CTD) was a high profile gainer, jumping 14.7% on the day, however, this one has broken the trend somewhat by pulling back since then, and now sits at 6.7% up since the result.

It may not be surprising there was some volatility here given the 4% short position, and its recent history of the stock which plunged a few months ago after a short report surfaced. Naheed Rahman at Flinders also covered this one in ‘Corporate Travel lays down the runway for a rerating’ saying that

"The interim result today demonstrated a company firmly on a strong growth trajectory. It’s entirely reasonable for a quality company growing its earnings per share organically at 15-20% annually (with a realistic expectation that this will continue for many years given the large addressable market, and acquisitions to provide additional earnings growth), with strong returns and a highly capable management team, to be trading at above-market multiples. At today’s share price, the company is trading on a PE of ~25x, still towards the bottom end of its PE multiple trading range, and a level that we believe represents reasonable value."

Marcus Bogdan at Blackmore Capital wrote about $4.4 billion Cleanaway (CWY), which has been climbing strongly over the last 3 years and has jumped 35% year-to date. This includes a 12.8% on the result (now up 11.7%). Marcus wrote in Cleanaway: A defensive midcap on the rise that:

“We remain positively disposed towards CWY’s investment case given its high level of earnings visibility (>80% of earnings contracted) and growth optionality across each of its businesses. WY is trading on a FY20 EV/EBITDA of c. 8.8 times, which compares favourably to its international waste management peer group, particularly given its ability to continue to deliver double-digit earnings per share growth over the forecast period."

Dairy darling, A2 Milk (A2M), popped 10% on the day, and still sits around the same level now. Andrew Mitchell at Ophir has been a long-term supporter of this runaway success story, noting that A2’s current cash position is now greater than the company’s entire market capitalisation was in 2012. Regarding the latest set of results Andrew commented in A2 delivers again that

"Specialist dairy and infant milk formula producer The A2 Milk Company (A2M) has been one such notable performer, a business that only six years ago was a A$210m market cap NZ-based fresh milk producer generating $48.6m in revenues from the sale of bottled A2-only milk into supermarket chains in Australia and New Zealand. Today, the same humble Kiwi milk producer now commands a market capitalisation of over A$9.7bn, selling fresh milk and infant milk formula (IMF) products into Australia, New Zealand, China, the US and UK and will deliver an expected ~A$1.25bn in revenue for the 2019 financial year.

With a significant amount of runway left for the business in the two largest economies in the world, we continue to maintain confidence that the company will be a significantly larger one in years to come."

Nearmap (ASX:NEA) was one that didn’t disappoint either (up 7.5% on the day and 10.9% since). The stock has gained notable support among fund managers in recent months:

- Nearmap: Climbing through turbulence;

- Buy Hold Sell: 5 emerging growth stocks;

- Why we're bullish in 5 charts;

Mason Willoughby-Thomas from Global leader in the delivery of reality as a service”, summarising thus:

"After an extraordinary share price performance over the last year, and with a market capitalisation approaching $1 billion, some might question whether the shares have run beyond fundamentals. However, what we have witnessed over the past 12 months is a company with market-leading technology operating in a large, global and growing addressable marketplace that is effectively exploiting a first mover advantage. The size of the opportunity looks set to underpin Nearmap’s growth well into the future".

While QBE’s 4.2% initial jump on Monday’s results is the smallest on this list, this is a $16 billion stock, so it was a highly significant move. The stock has kept moving since and is now up over 7% from the result. Hugh Dive at Atlas wrote about it in QBE up 4% as housekeeping shows through, writing that:

“Today’s result from QBE was a clean result that reflects the moves management have made over the past few years to simplify QBE’s sprawling insurance empire. QBE trades on an undemanding PE multiple of 12x with a 5% dividend yield and will enjoy near term tailwinds from hardening premium rates globally and rising interest rates”.

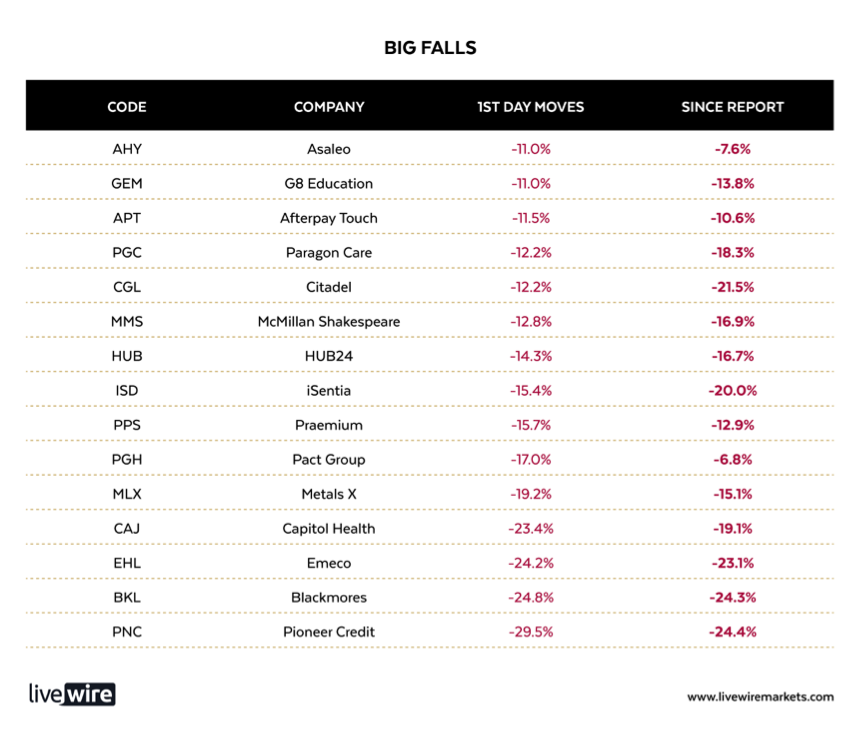

The biggest falls of reporting season

Just as there were some massive day-one jumps, there were some huge falls too, with Capitol Health, Emeco, Blackmores and Pioneer Credit all taking their turn under the blowtorch to lose more than 20% in a day. Even everyone’s favourite growth stock, Afterpay Touch, made it onto the naughty list...

Source: Data from Richard Coppleson and IRESS

Looking at the big fallers under our coverage, Joe Magyer from Lakehouse Capital wrote about Afterpay Touch (APT) which, to be fair followed a 20% jump the day before, fell 11.5% on day one of results, to now sit down by 10.6% since the result.

In the most widely distributed wire of this series, Afterpay’s opportunity much bigger than the market realises, Joe pulled out the key points from the result and summarised to say that:

"It’s hard to be indifferent about Afterpay Touch, which is one of the fastest-growing yet most divisive companies listed on the ASX. The market’s reaction this morning to the announcement of first-half results was no exception with the shares off by around 9% at lunchtime despite continued torrid growth. As usual, the market’s initial response was caught up on how results stacked up relative to consensus expectations, and some of the headline numbers were already in the market via a business update in January. Our view is that, while Afterpay Touch is a business and stock with a wide range of outcomes, the market is underestimating the scope of Afterpay’s opportunity here and abroad".

The worst intraday performer in our reporting season series was Isentia (ISD) which has burnt investors for three long years now to sit 91% under its high of late-2015.

It fell 12.2% on day one of results, and has slipped further to be down 17.2% now. Looking past the price chart, however, Graeme Carson from Cyan called it a classic turnaround story and wrote in ‘Turning bullish on Isentia” that:

"...The foundations of this business are solid, over 3000 subscription customers across 11 Asian Pacific market generating revenues of ~$120m in FY19 and underlying EBITDA around $20m. Debt at $40m is manageable, particularly given the strong operating cashflow, and well within banking covenants. We believe ISD is a textbook example of the “baby being throw out with the bathwater”. And really, who could blame investors who have been with the stock since listing? With a market cap well below the $100m line-in-the-sand for institutional investors but with a substantial existing market presence in its industry, ISD looks well poised to be a classic turnaround story".

Ben Rundle at NAOS Asset Management wrote about Smartgroup’s result (SIQ) which dropped 9.2% and is now down by 13.3%. While it has fallen, Ben has spotted an opportunity emerging:

SIQ is clearly operating in a difficult environment, however it is during these periods we can truly examine the underlying strength of the business. SIQ is a highly profitable business with an excellent management team and they appear to be taking market share whilst the trading environment is difficult and still generating organic growth. In our view, SIQ could trade lower post this result and fall out of favour with some investors. The consensus earnings estimate could likely be revised lower due to softer organic growth trends and the issue around warranties. SIQ will be one to watch closely for now as once the sellers have been shaken out we could see a meaningful buying opportunity

Tim Hannon from Newgate Capital Partners wrote about Whitehaven (WHC), which fell 6.7% day one and is now down 8.4%, making a convincing case on the company's metrics, and also the dynamics of the industry:

"On these very basic numbers, WHC is generating $850 million of free cashflow on a market capitalisation of $4.4 billion. This represents a free cashflow yield of 20%. We can debate how long thermal coal prices stay elevated for, but as we have highlighted there are some structural factors that are likely to support it at much higher levels than we have seen in history".

Full listing of Feb 2019 reporting season commentary

We had fund manager coverage of over 30 stocks through reporting season, and for more stock insights you can access the full listing here.

If you enjoyed this wire, please like, share, comment, forward to your investor community and subscribe (for free) if you haven't already! Happy investing.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Alex Cowie,

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

1 topic

12 stocks mentioned

10 contributors mentioned

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets